Get In-Demand Finance Certifications

FCFE = Net Income + Depreciation & Amortization – CapEx – ΔWorking Capital + Net Borrowing

Free Cash Flow to Equity (FCFE) can be calculated using net income as well as using the Free Cash Flow to the Firm (FCFF) formula. It is the amount of cash generated by a company that can be potentially distributed to the company’s shareholders. When using an intrinsic valuation method such as the Discounted Cash Flow (DCF) valuation model, an analyst can use FCFE as the business’ cash flow generating ability.

The FCFE is different from the free cash flow to the firm (FCFF), which indicates the amount of cash generated to all holders of the company’s securities (both investors and lenders).

Free cash flow to equity (FCFE) can be calculated in many ways. To calculate the FCFE from net income, we need to look at the formula and break it down. Here is the formula to calculate FCFE from net income:

However, FCFE is usually derived by using the free cash flow to the firm (FCFF) formula. To reconcile this, let’s look at how we get FCFE from FCFF. Here is the formula for FCFF:

Where:

Notice that FCFE and FCFF share very similar terms such as depreciation, capital expenditures, and changes in working capital. The main difference between the FCFF and FCFE is the impact of interest expenses and their tax shields. Therefore, the FCFE can be calculated using the FCFF formula:

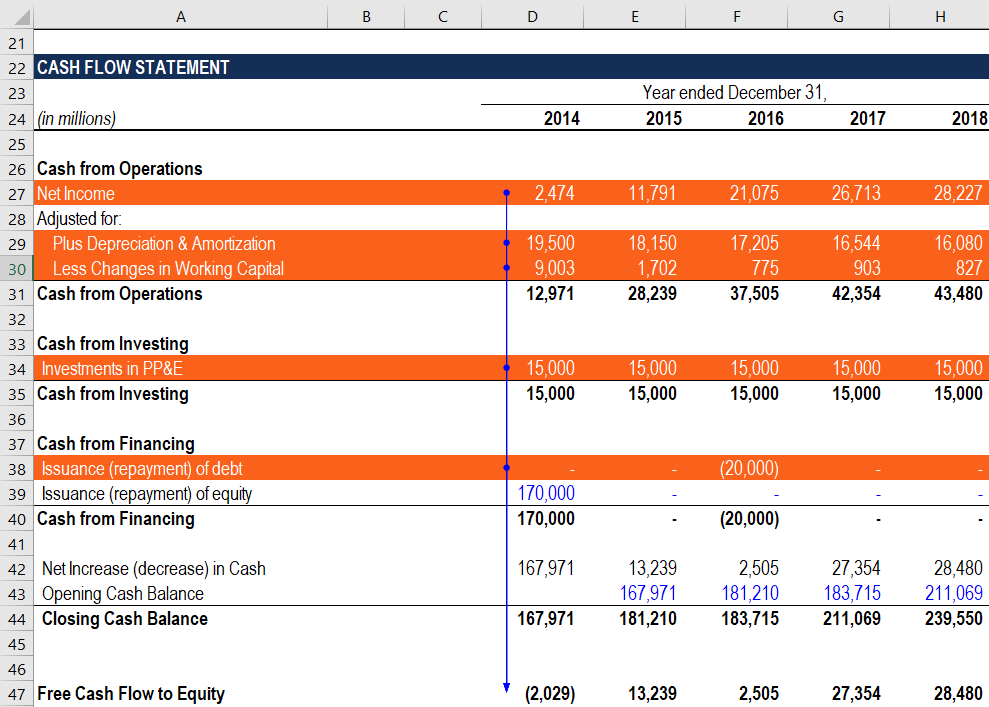

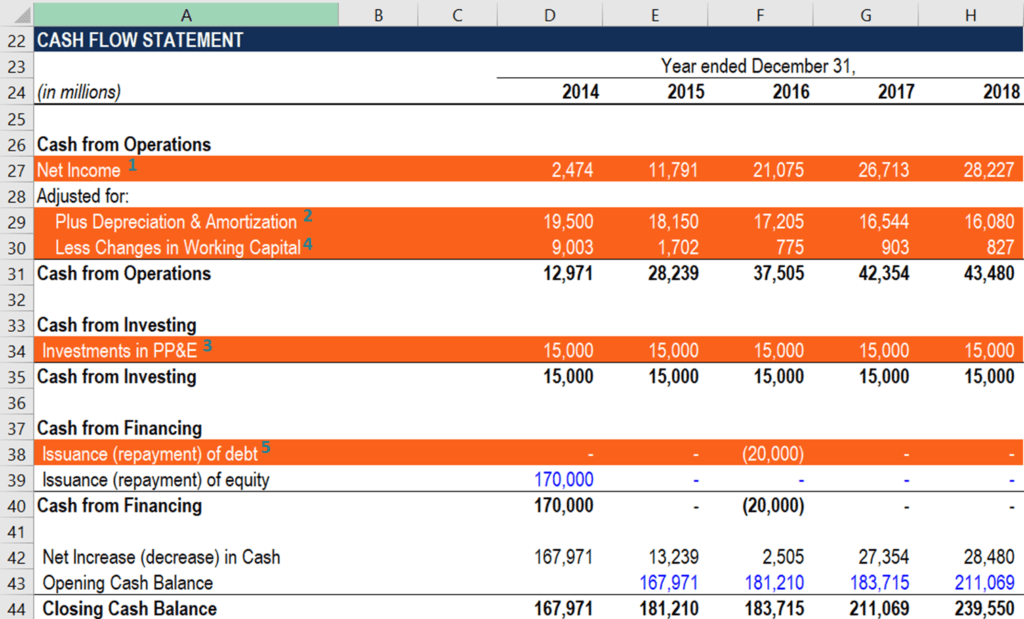

An analyst who calculates the free cash flows to equity in a financial model must be able to quickly navigate through a company’s financial statements. The primary reason is that all the inputs required for the calculation of the metric are taken from the financial statements. The guidance below will help you to quickly and correctly incorporate the FCFE from Net Income calculation into a financial model.

Thank you for reading CFI’s guide to Calculating FCFE from Net Income. To keep learning and developing your knowledge of financial analysis, we highly recommend the additional CFI resources below:

Below is a break down of subject weightings in the FMVA® financial analyst program. As you can see there is a heavy focus on financial modeling, finance, Excel, business valuation, budgeting/forecasting, PowerPoint presentations, accounting and business strategy.

A well rounded financial analyst possesses all of the above skills!

CFI is the global institution behind the financial modeling and valuation analyst FMVA® Designation. CFI is on a mission to enable anyone to be a great financial analyst and have a great career path. In order to help you advance your career, CFI has compiled many resources to assist you along the path.

In order to become a great financial analyst, here are some more questions and answers for you to discover: