Get In-Demand Finance Certifications

Valuation and forecasting using multiples

The multiples analysis is a valuation technique that utilizes different financial metrics from comparable companies to value a target company. Thus, the assumption is that the relative value of certain financial ratios can be used to rank or value a company within a similar group.

Despite being the oldest technique in valuation, the multiples analysis is still used. However, it is now being incorporated with the discounted cash flow analysis and other market-based methods in valuation.

The first step in conducting a multiples analysis is to identify companies or assets that have similar business structures or operations. The next step is to determine the market value for each company. This is followed by utilizing standardized valuation multiples.

Under this process, each company’s market value is to be converted into a standardized value that is relative to a key statistic. Finally, a range of valuation multiples is applied to the target company’s key statistic in order to accommodate variation between the group of assets being compared.

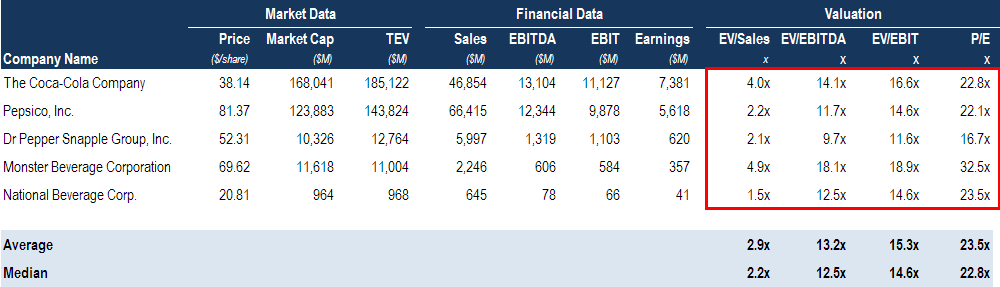

Multiples used in multiples analysis can be classified as enterprise value multiples or equity multiples. The most common equity multiple is the P/E ratio – or the price per earnings ratio – while the most common enterprise value multiple is the EV/Sales or the enterprise value per net sales ratio.

Equity multiples are often used in equity valuation. Investors are more familiar with these than the enterprise value multiples. On the other hand, enterprise value multiples are more comprehensive and have more available multiples to be used. These multiples allow analysts to focus on key statistics that minimize differences in accounting policies.

The simplicity of using multiples in valuation is both an advantage and a disadvantage. It is a disadvantage because it simplifies complex information into just a single value or a series of values. This effectively disregards other factors that affect a company’s intrinsic value, such as growth or decline. However, this simplicity allows a financial analyst to make quick computations to assess a company’s value.

Meanwhile, using multiple analysis can also lead to difficulty in comparing companies or assets. This is because companies, even when they seem to have identical business operations, may have different accounting policies. As such, multiples may be easily misinterpreted, and comparisons are not as conclusive. They need to be adjusted for different accounting policies.

Multiples analysis also disregards the future – it is static. It only considers the company’s position for a certain time period and fails to include the company’s growth in its business operations. However, there are ways to adjust for this using certain multiples that look at “leading” ratios.

Thank you for reading CFI’s guide to Multiples Analysis. To keep advancing your career, the additional resources below will be useful:

Below is a break down of subject weightings in the FMVA® financial analyst program. As you can see there is a heavy focus on financial modeling, finance, Excel, business valuation, budgeting/forecasting, PowerPoint presentations, accounting and business strategy.

A well rounded financial analyst possesses all of the above skills!

CFI is the global institution behind the financial modeling and valuation analyst FMVA® Designation. CFI is on a mission to enable anyone to be a great financial analyst and have a great career path. In order to help you advance your career, CFI has compiled many resources to assist you along the path.

In order to become a great financial analyst, here are some more questions and answers for you to discover: