Get In-Demand Finance Certifications

The formula to determine the contribution margin of a business

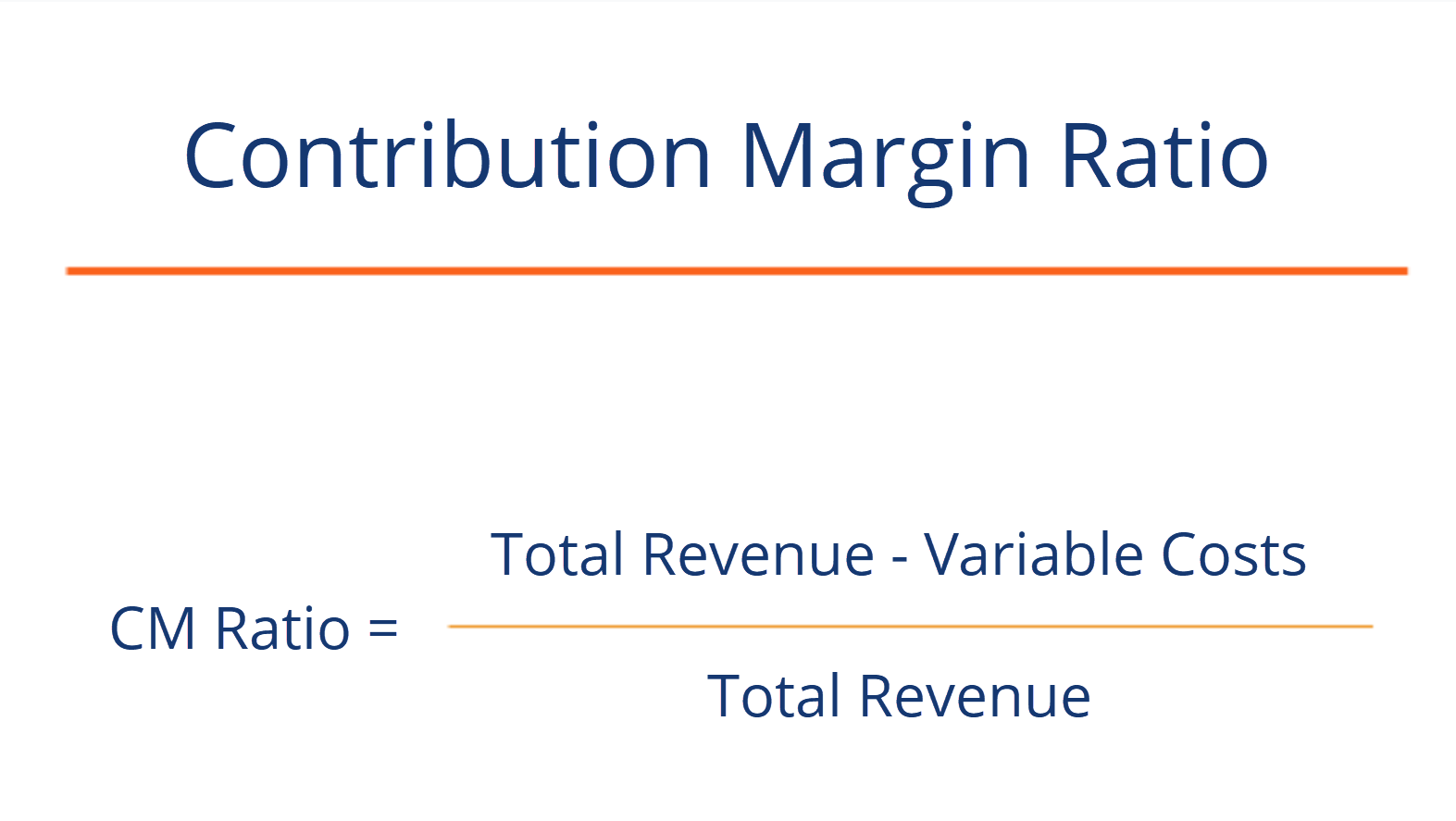

The contribution margin ratio (CM ratio) of a business is equal to its revenue less all variable costs, divided by its revenue. It represents the marginal benefit of producing one more unit. Here is the formula for contribution margin ratio (CM ratio):

See an example in Excel here.

CM ratio = (total revenue – cost of goods sold – any other variable expenses) / total revenue

A company has revenues of $50 million, the cost of goods sold is $20 million, marketing is $5 million, product delivery fees are $5 million, and fixed costs are $10 million.

Contribution margin dollars = $50M – $20M – $5M – $5M = $20 million

Contribution margin ratio = $20M / $50M = 40%

The fixed costs of $10 million are not included in the formula, however, it is important to make sure the CM dollars are greater than the fixed costs, otherwise, the company is not profitable.

The contribution margin is not necessarily a good indication of economic benefit. Companies may have significant fixed costs that need to be factored in.

It can be important to perform a breakeven analysis to determine how many units need to be sold, and at what price, in order for a company to break even. To learn more, check out our Financial Analysis course.

In order to perform this analysis, calculate the contribution margin per unit, then divide the fixed costs by this number and you will know how many units you have to sell to break even.

Building on the above example, suppose that the company sold 1 million units. That means the CM per unit is $20. Fixed costs are $10 million so the company has to sell 500,000 units to break even ($10 million / $20 per unit = 500,000).

Enter your name and email in the form below and download the free template now!

Download the free Excel template now to advance your finance knowledge!

Thank you for reading CFI’s guide to Contribution Margin Ratio. To learn more about other types of financial analysis you may want to check out these additional CFI resources:

To find out more about finance careers, try out our interactive Career Map.

CFI is a global provider of financial modeling courses and of the FMVA Certification. CFI’s mission is to help all professionals improve their technical skills. If you are a student or looking for a career change, the CFI website has many free resources to help you jumpstart your Career in Finance. If you are seeking to improve your technical skills, check out some of our most popular courses. Below are some additional resources for you to further explore:

CFI is a global provider of financial modeling courses and of the FMVA Certification. CFI’s mission is to help all professionals improve their technical skills. If you are a student or looking for a career change, the CFI website has many free resources to help you jumpstart your Career in Finance. If you are seeking to improve your technical skills, check out some of our most popular courses. Below are some additional resources for you to further explore:

Below is a break down of subject weightings in the FMVA® financial analyst program. As you can see there is a heavy focus on financial modeling, finance, Excel, business valuation, budgeting/forecasting, PowerPoint presentations, accounting and business strategy.

A well rounded financial analyst possesses all of the above skills!

CFI is the global institution behind the financial modeling and valuation analyst FMVA® Designation. CFI is on a mission to enable anyone to be a great financial analyst and have a great career path. In order to help you advance your career, CFI has compiled many resources to assist you along the path.

In order to become a great financial analyst, here are some more questions and answers for you to discover: