Get Certified for Financial Modeling (FMVA)®

Gain in-demand industry knowledge and hands-on practice that will help you stand out from the competition and become a world-class financial analyst.

When analyzing a bank’s valuation, profitability alone doesn’t tell the full story. A bank may post billions in earnings yet remain constrained in dividend payouts or growth potential. The reason? Bank regulatory capital.

Regulatory capital requirements determine how much capital banks must hold before distributing profits to shareholders or expanding their loan book. These constraints shape valuation models, dictate dividend policies, and impact a bank’s ability to generate returns.

This guide breaks down:

Whether you are new to valuation or adding to your expertise, understanding bank regulatory capital is critical to assessing a bank’s financial health and investment potential.

Bank regulatory capital is the minimum amount of financial resources a bank must hold to absorb losses and ensure financial stability. It serves as a protective cushion, ensuring banks remain solvent during economic downturns.

Banks maintain three tiers of capital, ranked by their ability to absorb losses:

Common Equity Tier 1 (CET1) — The highest-quality capital, consisting of common stock and retained earnings.

Additional Tier 1 (AT1) — Hybrid securities like preferred shares and subordinated debt, which provide some loss absorption.

Tier 2 Capital — Includes subordinated debt and loan loss provisions, offering less protection than CET1.

To remain compliant, banks must meet minimum capital ratios set by Basel III regulations, with CET1 being the most critical for valuation.

After the 2008 financial crisis, many banks lacked sufficient capital to withstand financial distress. In response, Basel III introduced stricter capital requirements to strengthen financial stability.

✅ Higher capital requirements to ensure banks hold sufficient reserves.

✅ Minimum CET1 ratio of 4.5%, but most banks maintain much higher levels.

✅ Capital buffers that prevent excessive risk-taking.

These regulatory constraints mean banks cannot freely distribute all their earnings to shareholders. They must first ensure capital adequacy.

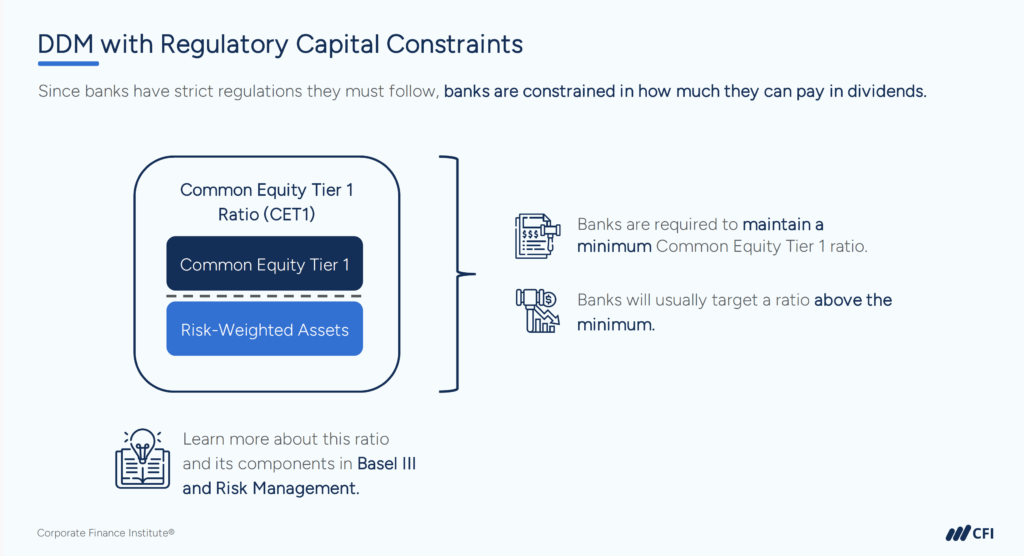

A bank’s CET1 ratio is one of the most important metrics for assessing financial health and investment potential.

Formula: CET1 Ratio = Common Equity Tier 1 Capital ÷ Risk-Weighted Assets (RWA)

Higher CET1 ratios indicate strong financial stability, but banks with excessive capital reserves may see lower returns on equity (ROE), which can impact valuation multiples.

Learn more about the CET1 ratio and its components in CFI’s Basel III and Risk Management course.

Regulatory capital constraints directly impact dividend policies. Banks must maintain required capital buffers before distributing earnings to shareholders.

For example:

A bank’s ability to expand its loan book is directly tied to its regulatory capital position. For instance:

Capital constraints can affect growth potential and may require banks to issue new equity or retain more earnings, both of which can influence valuation.

The collapse of First Republic Bank (FRB) in 2023 highlights how regulatory capital constraints can limit a bank’s ability to recover from financial distress. While FRB met minimum CET1 requirements, it struggled with:

Despite technical solvency under capital regulations, FRB faced a critical challenge:

✅ Regulatory capital rules restricted how it could use reserves. Drawing down capital would have pushed CET1 ratios below required thresholds.

❌ Raising new capital became nearly impossible as its stock price plummeted.

Liquidity dried up, and without market confidence, the bank could not absorb losses or reassure depositors.

Ultimately, capital strength alone wasn’t enough — liquidity management, asset-liability strategy, and investor confidence all proved just as critical.

The Dividend Discount Model assumes companies can freely distribute excess cash flows, but for banks, regulatory capital constraints limit available dividends.

Adjusted DDM Approach for Banks:

Let’s apply the DDM approach while considering regulatory capital constraints.

A bank reports:

To fund its loan growth, the bank must increase its CET1 capital by $40 million to maintain its regulatory capital ratio. Additionally, management sets aside $10 million to strengthen its capital buffer before distributing dividends.

CET1 Ratio Formula

Since the bank needs $40 million in CET1 capital to support $500 million in new RWA, we can estimate its target CET1 ratio:

40 / 500 = 8%

If the bank maintains its capital ratios before and after growth, this suggests its CET1 ratio is approximately 8%.

Because dividends are paid only after capital requirements are met, the CET1 ratio acts as a constraint on distributions. In this example, the bank’s available dividend payout of $50 million is determined only after fulfilling capital retention needs, reinforcing why bank valuation models must account for regulatory capital constraints.

The RI model accounts for capital costs and regulatory constraints better than DDM. It focuses on:

✅ Earnings beyond required capital levels.

✅ Capital intensity of different business lines (e.g., lending vs. trading).

For instance, a capital-light trading business might generate higher risk-adjusted returns than traditional lending, making regulatory capital allocation crucial in valuation.

Banks with higher CET1 ratios often trade at higher Price-to-Book (P/B) multiples, reflecting their stronger capital position. However:

Bank regulatory capital directly impacts valuation, risk assessment, and financial decision-making. It dictates how much capital banks must retain, what they can distribute to shareholders, and how they finance growth. Analysts and investors who factor in these constraints can better assess a bank’s valuation and long-term profitability.

Understanding regulatory capital improves valuation accuracy and risk assessment. Factoring capital requirements into models provides a clearer picture of a bank’s intrinsic value, while capital adequacy ratios reveal its ability to generate sustainable returns. Dividend policies also reflect how capital constraints affect shareholder value and distributions.

Want to strengthen your expertise in bank valuation? CFI’s Financial Modeling & Valuation Analyst (FMVA®) Certification equips you with practical training in advanced and specialized valuation methods, including techniques for valuing banks.

Earn Your FMVA® Certification!

Bank Valuation: Why Traditional Methods Don’t Work (And What Does)