Accidental Death and Dismemberment Insurance (AD&D)

An insurance policy that pays out to beneficiaries in the events of accidental death or dismemberment

What is Accidental Death and Dismemberment Insurance (AD&D)?

Accidental Death and Dismemberment Insurance (AD&D) is an insurance policy that pays out to beneficiaries in the events of accidental death or dismemberment. Dismemberment includes full or partial loss of bodily functions, such as sight, hearing, or use of a limb.

Summary

- Accidental death and dismemberment insurance (AD&D) is an insurance policy that pays out to beneficiaries in the events of accidental death or dismemberment.

- Accidental deaths include deaths resulting from falls, homicide, motor vehicle/heavy equipment accidents, and drowning.

- Dismemberment refers to the loss of an appendage, hearing, sight, or other bodily functions.

How AD&D Insurance Works

AD&D insurance will outline a schedule with the terms of the agreement. It includes the timeframe covered under the insurance and the percentages of benefits. Generally, a full payout will only occur in the event of death, and dismemberment will result in a partial payout.

A range of payout situations will be outlined by the insurance company on a tiered basis. For example, loss of sight in one eye may result in a partial payout relative to the full loss of sight. As with all insurance contracts, the premium paid will be related to the risk of the insured party. AD&D insurance is usually offered through an employer; however, it can be purchased on an individual basis.

Accidental Death

Accidental deaths include deaths resulting from falls, homicide, motor vehicle/heavy equipment accidents, and drowning. Based on current statistics, they represent the fifth-leading cause of death in Canada and the US.

Individuals can take out a life insurance policy, as well as an AD&D policy (known as double indemnity coverage), and in the event of accidental death, both policies will pay out. In the case of a claim, the insured will undergo an investigation and may need to undergo an autopsy.

Dismemberment

Dismemberment refers to the loss of an appendage, hearing, sight, or another bodily function. In a dismemberment payout, only a portion of the contract will be paid out. The portion relates to the severity of the injury sustained and how it is outlined in the contract.

As people age, the terms of their AD&D policy will be revised; however, the policy will automatically renew without action by the insured party.

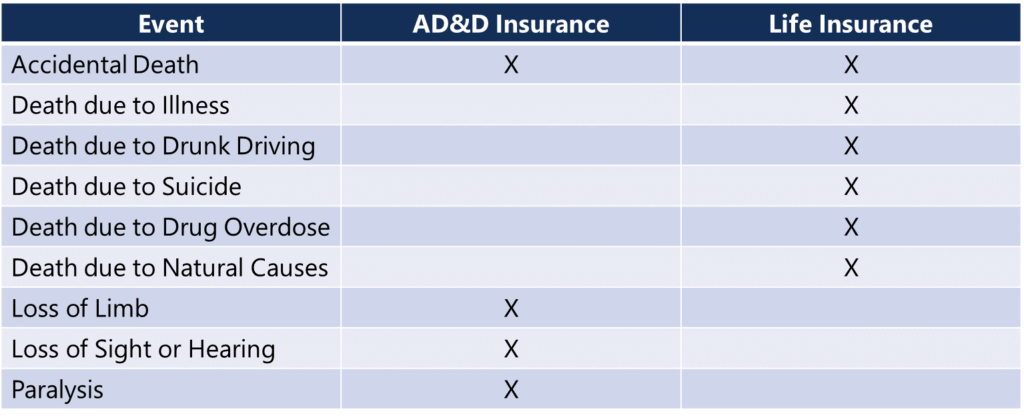

AD&D Insurance vs. Life Insurance

While AD&D insurance and life insurance cover many of the same events, they are also different in a few ways. The main difference is that life insurance will cover death in almost any situation (regardless of accidental or not), while AD&D insurance will not.

Conversely, AD&D insurance will cover accidental dismemberment, while life insurance will not. The table below helps to better visualize the difference in coverage between AD&D insurance and life insurance.

AD&D is also significantly cheaper than life insurance due to a few exclusions. For example, a significant portion of the population will be impaired or killed by cancer or heart disease. While cancer and heart disease would be covered by life insurance, it wouldn’t be covered by AD&D insurance.

For such reasons, it is essential that individuals looking to purchase AD&D insurance know exactly what is covered, as well as exclusions within the policy.

Exclusions

Within AD&D contracts, the insurer usually lists some events that would cause the contract to become void. While they differ between contracts, there are general commonalities between exclusions.

The first is if the insured party is under the influence of drugs or alcohol at the time of injury or death, the contract is void whether the substance was the direct or indirect cause of the accident.

Additionally, deaths related to suicide, illness, or natural causes are generally not covered by the policy. In some cases, policies will include them within coverage; however, premiums will be higher.

Practical Example

An individual takes out a life insurance policy and an AD&D policy (double indemnity coverage). The payout for both policies is $100,000, with fractional amounts on the AD&D contract in the event of dismemberment.

The individual later dies in a car accident, and the toxicology report reveals that the policyholder was under the influence of alcohol during the accident. In such a situation, only the life insurance policy would pay out, and the beneficiaries would receive $100,000.

Also, imagine a similar situation where the individual wasn’t under the influence of alcohol and lost an arm. The policy specifies a 50% payout in the event that the insured party loses a limb. In this situation, the insured individual would receive $50,000 (50% payout from the AD&D policy, and a 0% payout from the life insurance policy).

Related Readings

CFI is the official provider of the global Commercial Banking & Credit Analyst (CBCA)™ certification program, designed to help anyone become a world-class financial analyst. To keep advancing your career, the additional resources below will be useful: