Get Certified for

Capital Markets (CMSA®)

From equities and fixed income to derivatives, the CMSA certification bridges the gap from where you are now to where you want to be — a world-class capital markets analyst.

A process to verify the identity and other credentials of a financial services user

The Know Your Client (KYC) or Know Your Customer (KYC) is a process to verify the identity and other credentials of a financial services user. KYC is a regulatory process of ascertaining the identity and other information of a financial services user.

The Know Your Client (KYC) process helps against money laundering and prevents the financing of terrorist activities. It is a mandatory process required by many countries to ensure that the customers are actually who they are claiming to be.

To be mandated by the law, the Know Your Client (KYC) process also helps the financial institutions in several ways:

A number of countries and economic regions oversee financial anti-money laundering agencies or regulators that oversee financial transactions to prevent tax evasion, terrorism financing, and other anti-social activities. All the agencies are a part of the Global Financial Action Task Force (FATF), which oversees financial transactions globally.

The KYC process is carried out for both individuals and organizations. KYC authentication is based on the verification of identity and place of residence. The documents required for the KYC process for individuals include the usual documents that individuals generally use, such as:

For proof of residence, the following documents can be furnished:

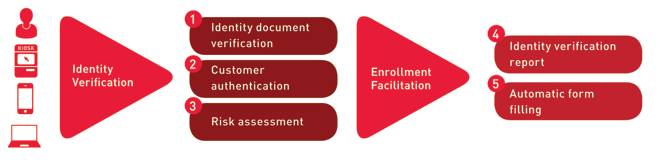

The KYC process is simple and differs only slightly from country to country. A simple KYC process flow is depicted below:

The KYC process can follow the following steps, although not always in the same order:

An applicant or potential user of financial services is required to submit documents for the verification of their identity and residence status. The submission can be either in electronic form or physical form.

The identity verification is carried out from the authorized agency/organization based on the document submitted. For example, if the applicant submits a driver’s license, the verification will be done from the Department of Motor Vehicles (DMV).

The residency verification requires ascertaining the resident status (domestic or foreign), current residential address, alternative residential address, citizenship status, etc.

The assets and liabilities claimed are verified using documents, contacting the issuer, and physical checks. This reduces the risk of misrepresentation.

The financial institution checks the transactions conducted by the customer/client, and any transaction that is different/high-valued, frequent, etc., is flagged automatically and then undergoes stringent manual checks.

After completion of all the above steps, the individual/body is deemed KYC verified. It may also include a verification certificate, but that is generally not the case. The process may be simple for the user, but the financial institution’s verification process needs dedication and diligence. The KYC process is an integral part of various due diligence checks made by companies, investors, banks, etc.

As discussed earlier, the KYC process consumes a significant amount of time and effort. Hiring staff and performing physical verification is a cumbersome and costly affair. The cost becomes higher for smaller financial institutions. As a result, the KYC process is usually contracted out to agencies that specialize in them. The two major reasons for doing so are:

Choosing an agency to perform KYC depends on the type of verification needed. Some processes, such as a bank account opening, may not involve checks on assets and liabilities. Therefore, some important facts to consider include:

Connect what you just learned to a clear career path with CFI’s role‑based courses and certification programs.

CFI is the official provider of the global Capital Markets & Securities Analyst (CMSA)® certification program, designed to help anyone become a world-class financial analyst. To keep advancing your career, the additional CFI resources below will be useful: