Get Certified for Financial Modeling (FMVA)®

Gain in-demand industry knowledge and hands-on practice that will help you stand out from the competition and become a world-class financial analyst.

A liquidity ratio that measures how many times a company pays its creditors over an accounting period

The accounts payable turnover ratio, also known as the payables turnover or the creditor’s turnover ratio, is a liquidity ratio that measures the average number of times a company pays its creditors over an accounting period. The ratio is a measure of short-term liquidity, with a higher payable turnover ratio being more favorable.

The formula for the accounts payable turnover ratio is as follows:

In some cases, the cost of goods sold (COGS) is used in the numerator in place of net credit purchases. Average accounts payable is the sum of accounts payable at the beginning and end of an accounting period, divided by 2.

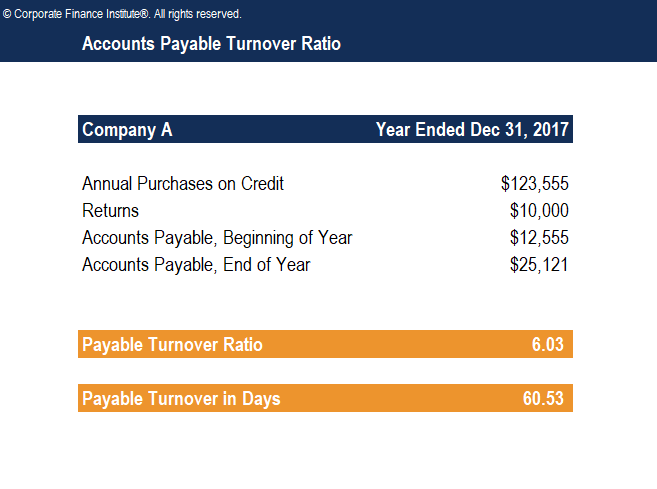

Company A reported annual purchases on credit of $123,555 and returns of $10,000 during the year ended December 31, 2017. Accounts payable at the beginning and end of the year were $12,555 and $25,121, respectively. The company wants to measure how many times it paid its creditors over the fiscal year.

Therefore, over the fiscal year, the company’s accounts payable turned over approximately 6.03 times during the year. The turnover ratio would likely be rounded off and simply stated as six.

The accounts payable turnover in days shows the average number of days that a payable remains unpaid. To calculate the accounts payable turnover in days, simply divide 365 days by the accounts payable turnover ratio.

Payable Turnover in Days = 365 / Payable Turnover Ratio

Determining the accounts payable turnover in days for Company A in the example above:

Payable Turnover in Days = 365 / 6.03 = 60.53

Therefore, over the fiscal year, the company takes approximately 60.53 days to pay its suppliers.

Download CFI’s Free Accounts Payable Turnover Ratio Template

Download CFI’s Free Accounts Payable Turnover Ratio TemplateClick the button below to download our free Accounts Payable Turnover Ratio template!

The accounts payable turnover ratio indicates to creditors the short-term liquidity and, to that extent, the creditworthiness of the company. A high ratio indicates prompt payment is being made to suppliers for purchases on credit. A high number may be due to suppliers demanding quick payments, or it may indicate that the company is seeking to take advantage of early payment discounts or actively working to improve its credit rating.

A low ratio indicates slow payment to suppliers for purchases on credit. This may be due to favorable credit terms, or it may signal cash flow problems and hence, a worsening financial condition. While a decreasing ratio could indicate a company in financial distress, that may not necessarily be the case. It might be that the company has successfully managed to negotiate better payment terms which allow it to make payments less frequently, without any penalty.

The accounts payable turnover ratio of a company is often driven by the credit terms of its suppliers. For example, companies that obtain favorable credit terms usually report a relatively lower ratio. Large companies with bargaining power who are able to secure better credit terms would result in lower accounts payable turnover ratio (source).

Although a high accounts payable turnover ratio is generally desirable to creditors as signaling creditworthiness, companies should also be taking advantage of the credit terms extended by suppliers, as doing so will result in discounts on purchases.

As with most financial metrics, a company’s turnover ratio is best examined relative to similar companies in its industry. For example, a company’s payables turnover ratio of two will be more concerning if virtually all of its competitors have a ratio of at least four.

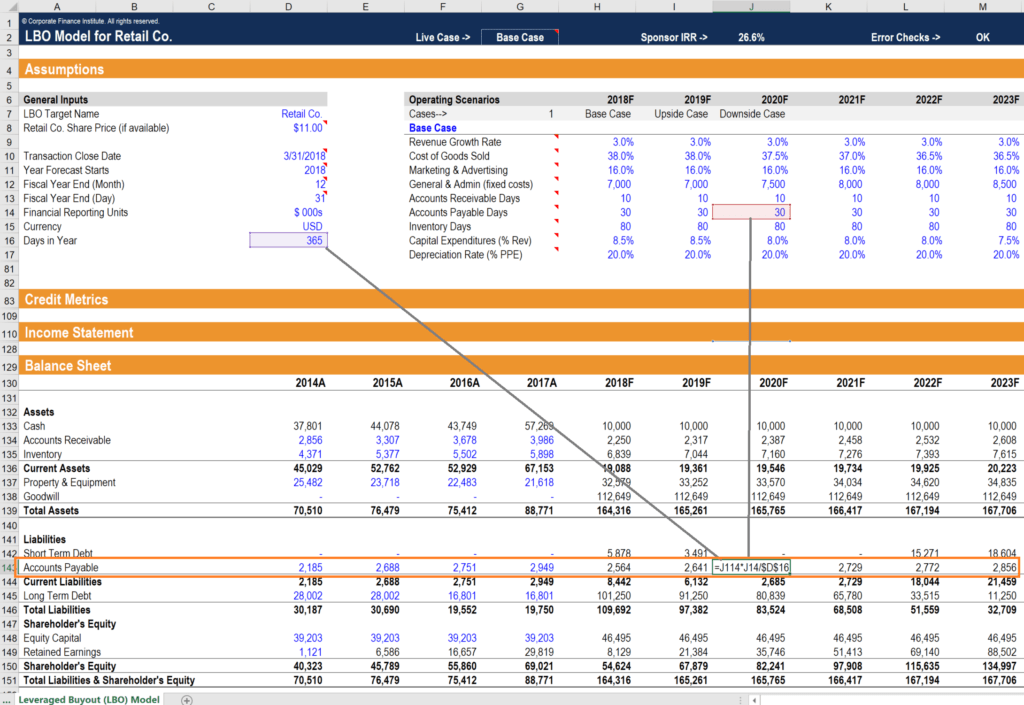

In financial modeling, the accounts payable turnover ratio (or turnover days) is an important assumption for creating the balance sheet forecast. As you can see in the example below, the accounts payable balance is driven by the assumption that the cost of goods sold (COGS) takes approximately 30 days to be paid (on average). Therefore, COGS in each period is multiplied by 30 and divided by the number of days in the period to get the AP balance.

The above screenshot is taken from CFI’s Financial Modeling Course.

Connect what you just learned to a clear career path with CFI’s role‑based courses and certification programs.

Thank you for reading CFI’s guide to Accounts Payable Turnover Ratio. To learn more and advance your career, the following CFI resources will be helpful: