Get Certified for Financial Modeling (FMVA)®

Gain in-demand industry knowledge and hands-on practice that will help you stand out from the competition and become a world-class financial analyst.

Represents an expense incurred during a specific period but has yet to be billed for

An accrued liability represents an expense a business has incurred during a specific period but has yet to be billed for. Accrued liabilities are only reported under accrual accounting to represent the performance of a company regardless of their cash position. They appear on the balance sheet under current liabilities.

Accrued liabilities are expenses that have yet to be paid for by a company. They are recorded to better represent the financial position of the company regardless if a cash transaction has occurred.

Recording accrued liabilities is part of the matching accounting principle. Under the matching principle, all expenses need to be recorded in the period they are incurred to accurately reflect financial performance.

When an accrued liability is paid for, the balance sheet side is reversed, leaving a net zero effect on the account. Accrued liabilities can also be thought of as the opposite of prepaid expenses.

There are two types of accrued liabilities: routine or recurring and infrequent or non-routine.

Routine/Recurring occurs as a normal operational expense of the business. An example would be accrued wages, as a company knows they have to periodically pay their employees.

Infrequent/Non-Routine is the opposite and does not occur as a normal operational part of the business. An example is a one-off purchase from a supplier where a bill is not immediately received. As the event isn’t recurring, it is considered an infrequent/non-routine accrued liability.

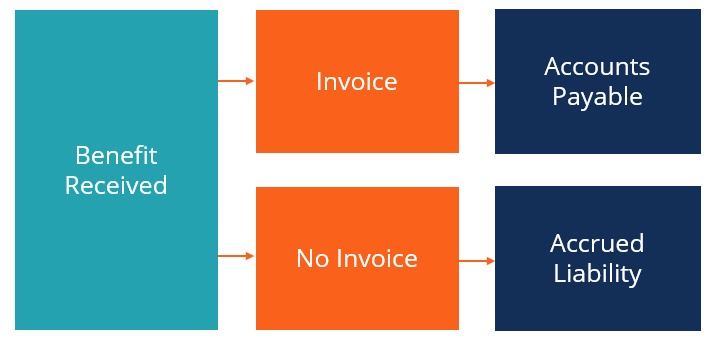

Accrued liabilities and accounts payable are both current liabilities. However, the difference between them is that accrued liabilities have not been billed, while accounts payable have. Accrued liabilities may not have been billed either because they are a regular expense that doesn’t require billing (i.e., payroll), or because the company hasn’t received a bill from the supplier.

For example, if a company has received a shipment from a supplier and has yet to receive a bill, they will record an accrued liability. However, if they were to receive the shipment and the bill before the end of the period, they would record an accounts payable.

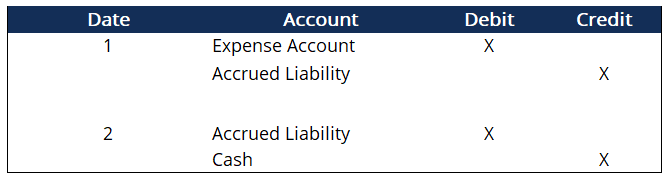

The journal entry is typically a credit to accrued liabilities and a debit to the corresponding expense account. Once the payment is made, accrued liabilities are debited, and cash is credited. At such a point, the accrued liability account will be completely removed from the books.

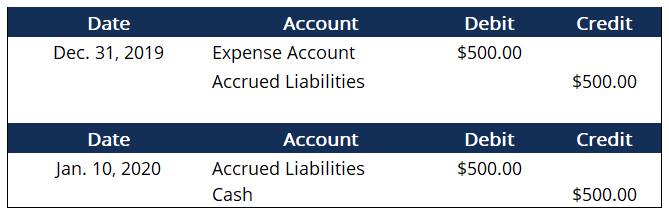

Company ABC has received product from their supplier on December 31st, costing $500. However, the supplier has yet to bill them. They receive the bill on January 10th and pay the same day.

Above are the journal entries for December 31st and January 10th. As you can see, the accrued liabilities account is net zero following the payment. The net effect on financial statements is an increase in the expense account and a decrease in the cash account. The purpose of accrued liabilities is to create a timeline of financial events.

Connect what you just learned to a clear career path with CFI’s role‑based courses and certification programs.

Thank you for reading CFI’s explanation of Accrued Liability. To keep learning and advancing your career, the following resources will be helpful: