Get Certified for Financial Modeling (FMVA)®

Gain in-demand industry knowledge and hands-on practice that will help you stand out from the competition and become a world-class financial analyst.

Rate of return from an accounting perspective

Accounting Rate of Return is the average net income an asset is expected to generate divided by its average capital cost, expressed as an annual percentage. It is a formula used to make capital budgeting decisions.

The accounting rate of return is used in situations where companies are deciding on whether or not to invest in an asset (a project, an acquisition, etc.) based on the future net earnings expected compared to the capital cost.

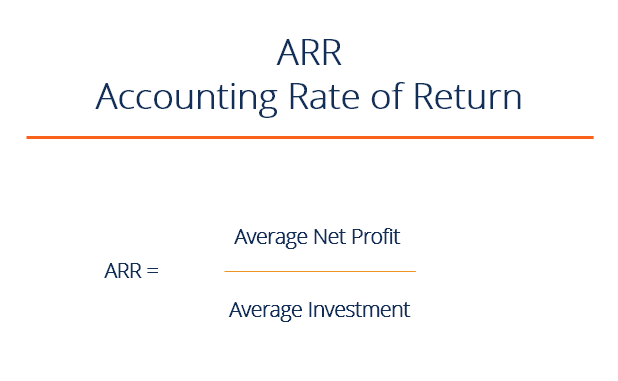

The formula for calculating the accounting rate of return is:

Accounting Rate of Return = Average Annual Profit / Average Investment

Where:

To learn more, launch our financial analysis courses!

If the accounting rate of return is equal to 5%, this means that the project is expected to earn five cents for every dollar invested per year.

In terms of decision making, if the accounting rate of return is equal to or greater than a company’s required rate of return, the project is acceptable because the company will earn at least the required rate of return.

If the accounting rate of return is less than the required rate of return, the project should be rejected. Therefore, the higher the accounting rate of return, the more profitable the company will become.

Read more about hurdle rates.

XYZ Company is looking to invest in some new machinery to replace its current malfunctioning one. The new machine, which costs $420,000, would increase annual revenue by $200,000 and annual expenses by $50,000. The machine is estimated to have a useful life of 12 years and zero salvage value.

| Step 1: Calculate Average Annual Profit | ||

| Inflows, Years 1-12 | ||

| (200,000*12) | $2,400,000 | |

| Less: Annual Expenses | ||

| (50,000*12) | -$600,000 | |

| Less: Depreciation | -$420,000 | |

| Total Profit | $1,380,000 | |

| Average Annual Profit | ||

| (1,380,000/12) | $115,000 | |

| Step 2: Calculate Average Investment | ||

| Average Investment | ||

| ($420,000 + $0)/2 = $210,000 | ||

| Step 3: Use the Formula | ||

| Accounting Rate of Return = $115,000/$210,000 = 54.76% | ||

Therefore, this means that for every dollar invested, the investment will return a profit of about 54.76 cents.

XYZ Company is considering investing in a project that requires an initial investment of $100,000 for some machinery. There will be net inflows of $20,000 for the first two years, $10,000 in years three and four, and $30,000 in year five. Finally, the machine has a salvage value of $25,000.

| Step 1: Calculate Average Annual Profit | ||

| Inflows, Years 1 & 2 | ||

| (20,000*2) | $40,000 | |

| Inflows, Years 3 & 4 | ||

| (10,000*2) | $20,000 | |

| Inflow, Year 5 | $30,000 | |

| Less: Depreciation | ||

| (100,000-25,000) | -$75,000 | |

| Total Profit | $15,000 | |

| Average Annual Profit | ||

| (15,000/5) | $3,000 | |

| Step 2: Calculate Average Investment | ||

| Average Investment | ||

| ($100,000 + $25,000) / 2 = $62,500 | ||

| Step 3: Use the Formula | ||

| Accounting Rate of Return = $3,000/$62,500 = 4.8% | ||

Click the button below to download CFI’s free Accounting Rate of Return template!

Although the accounting rate of return is an effective tool to grasp a general idea of whether to proceed with a project in terms of its profitability, there are several limitations to this approach:

To learn more, launch our financial analysis courses!

We hope the above article has been a helpful guide to understanding the Accounting Rate of Return, the formula, and how you can use it in your career. To keep learning and advancing your career, the additional CFI resources below will be helpful: