Get Certified for Financial Modeling (FMVA)®

Gain in-demand industry knowledge and hands-on practice that will help you stand out from the competition and become a world-class financial analyst.

Net profit is not recognized until the cash collected exceeds the cost of the good or service sold

The cost recovery method of revenue recognition is a concept in accounting that refers to a method in which a business does not recognize profit related to a sale until the cash collected exceeds the cost of the good or service sold. In other words, using this method, profits are only recognized when cash payments have recovered the seller’s cost.

The cost recovery method is a method of revenue recognition in which there is uncertainty. Therefore, it is used to account for revenue when revenue streams from a sale cannot be accurately determined. Accounting standards IAS 18 require a company to recognize revenue only when the amount is measurable and cash flows are probable. The underlying concept behind this method is as follows:

Net profit is not recognized until the cash collected exceeds the cost of the item and/or service sold.

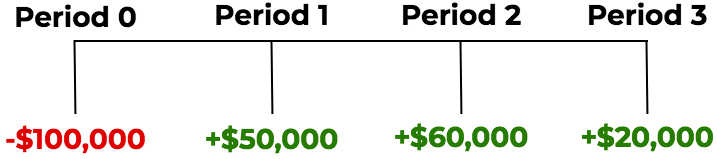

Shiny Clothes Ltd. is a retail store that recently purchased inventory costing $100,000. The retail store sells its inventory to multiple customers for a total sale price of $130,000, implying a $30,000 profit. The sales were made on credit, and Shiny Clothes Ltd. does not know the recovery rate of their sales to customers. The company decides to use the cost recovery method to recognize revenue.

The retail store made sales of $100,000 in period 0 and received cash flows from sales of $50,000, $60,000, and $20,000 in the following three periods, respectively. The cash flows from the sale of $100,000 inventory are shown as follows:

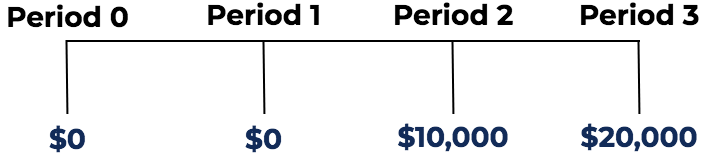

Recall that costs must be covered before any profit is recognized. In the scenario above, Shiny Clothes Ltd. would start recognizing profit in period 2 when the money inflow exceeds the cost of the sale. Profit for the sale of inventory under the cost recovery method would be recognized as follows:

With reference to the example above, the journal entries for Shiny Clothes Ltd for the sale of $100,000 worth of inventory would be as follows:

Learn more with CFI’s Free Accounting Courses.

If we accounted for the sale by Shiny Clothes Ltd. as a regular sale, the amount of profit recognized would be $30,000 in period 0. It would result in an immediate impact on a company’s earnings:

Period 1: +$30,000 in earnings

However, with the cost recovery method, there is uncertainty in the collection of money resulting from the sale. Therefore, no earnings will be recognized until the cash inflows exceed the cost. In the example above with Shiny Clothes Ltd., under the cost recovery method, the company’s earnings will be impacted as follows:

Connect what you just learned to a clear career path with CFI’s role‑based courses and certification programs.

Thank you for reading CFI’s guide to the Cost Recovery Method. To keep advancing your career, the additional CFI resources below will be useful: