Get Certified for Financial Modeling (FMVA)®

Gain in-demand industry knowledge and hands-on practice that will help you stand out from the competition and become a world-class financial analyst.

The choice of inventory accounting method has significant implications for financial analysts

Inventory accounting is an essential aspect of financial management and significantly impacts business operations and profitability. The choice of inventory valuation method has far-reaching implications for profitability, financial analysis, and even taxes. Companies must carefully select and consistently apply the most appropriate inventory accounting method for their business models while also considering the financial impact and the management of inventory control.

Inventory accounting is a critical component of financial management for companies that make or sell tangible goods. Inventory accounting involves the methods and practices used to assign value to and record inventory on financial statements.

Inventory is an accounting term for goods that are either held for sale to customers or goods that are in the process of being converted to a product that is ready for sale. Broadly speaking, inventory breaks down into three categories: 1) raw materials, 2) work-in-progress, and 3) finished goods.

The main purpose of inventory accounting is to accurately reflect the value of inventory on the balance sheet and the cost of goods sold (COGS) on the income statement. The inventory accounting process ensures that a company’s financial statements provide a true and fair view of its financial position and performance.

Inventory represents one of the most significant assets for many businesses, especially those in the manufacturing and retail sectors. It can tie up substantial amounts of cash flow and resources, which impacts sales and costs, including the cost of labor and accounting software designed to accurately track inventory.

Effective inventory management is crucial because it directly affects a company’s profitability. Overstocking can lead to increased holding costs and obsolete inventory while understocking can result in lost sales and dissatisfied customers. Inventory is not just a static asset but a dynamic element that influences the overall efficiency and success of a company’s operations.

Inventory valuation is the process of assigning a monetary value to the items in a company’s inventory. This valuation is crucial for determining the cost of goods sold and, ultimately, the gross profit of a business.

The choice of inventory valuation method can also significantly impact various ratios and complicate the ability of analysts to compare financial statements between companies that choose different inventory accounting methods. Having said that, companies should choose the method that best reflects the flow of goods and their associated costs.

There are several methods for assigning inventory value, each with different implications for financial reporting:

Note that the weighted average, FIFO, and LIFO methods are based on assumptions about the physical movement of inventory. These assumptions may differ from the actual movement of inventory. These methods would be used when it’s not practical to track each good individually.

Regardless of the method used, companies should always verify their physical inventory by conducting regular inventory counts whenever possible. This will help ensure that the reported inventory will match the actual inventory.

Another method permitted under both US GAAP and IFRS is the retail inventory method (RIM). This method is usually a little less complex than the aforementioned methods since it relies on a general assumption known as the cost-to-retail ratio.

The cost-to-retail ratio is calculated as the cost of a product divided by its retail price. COGS is then estimated by taking the cost-to-retail ratio and multiplying it by the sales during the period. Of course, the retail inventory method works best when the markup is consistent across all products. If this is not the case, then the result will not be very accurate.

Inventory directly impacts both a company’s balance sheet and income statement. Inventory is an asset to a company (usually a current asset); therefore, the inventory value affects both the current and total assets of the business, as well as the business’s working capital.

On the income statement, cost of goods sold is subtracted from revenues to determine gross profit. The method used to calculate inventory value (e.g., FIFO, LIFO, or weighted average) affects COGS, which in turn affects gross profit, operating income, and net income.

As discussed previously, during inflationary periods, LIFO COGS will be higher, reducing gross profit and net income (but also reducing income taxes). Conversely, FIFO will show lower COGS, resulting in higher gross profit and net income.

Inventory accounting plays a critical role in financial analysis. Professionals often analyze companies using inventory-related metrics, such as inventory turnover and days sales of inventory (DSI), to assess how well a company manages its inventory.

Of course, these metrics and ratios are meaningless in isolation and should be compared to comparable companies or over time in order to better judge company performance.

The different inventory valuation methods discussed earlier will lead to differences in these ratios, affecting comparability. For example, LIFO will show a higher inventory turnover due to higher COGS and lower inventory values. However, this in and of itself does not mean the company is better at managing its inventory (especially if compared to a company that uses FIFO, which will have a lower turnover, all else being equal).

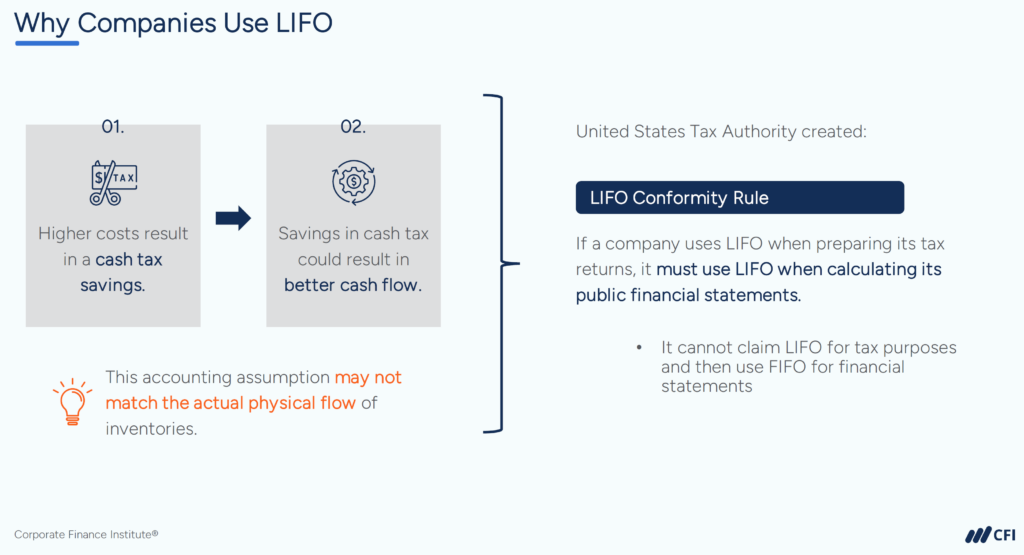

Inventory valuation methods may have significant tax implications, depending on the jurisdiction to which the taxes are subject. As discussed previously, US-based companies can use the LIFO method. This method normally results in higher COGS and lower taxable income. This results in tax savings for companies that use this method.

However, the US Internal Revenue Service requires that if a company uses LIFO for tax purposes, it must also use LIFO for reporting purposes. In other words, the company must prepare its GAAP-based financial statements using LIFO if the company uses LIFO for tax purposes. This prevents companies from using LIFO to minimize taxes, while then using FIFO to show better profitability to investors.

Because of the investment in inventory, and how important it is for many businesses, effective inventory management is absolutely critical. Managing inventory isn’t just about counting the physical inventory, but also optimizing inventory levels and minimizing costs.

Effective inventory management is crucial for optimizing the balance between inventory costs and availability. Techniques include:

Thank you for reading CFI’s guide on Inventory Accounting. To keep advancing your career and skills, the following CFI resources will be useful:

CFI’s Accounting Fundamentals course