Get Certified for Financial Modeling (FMVA)®

Gain in-demand industry knowledge and hands-on practice that will help you stand out from the competition and become a world-class financial analyst.

Activities performed by a company to make sure it got enough resources for day-to-day operating expenses

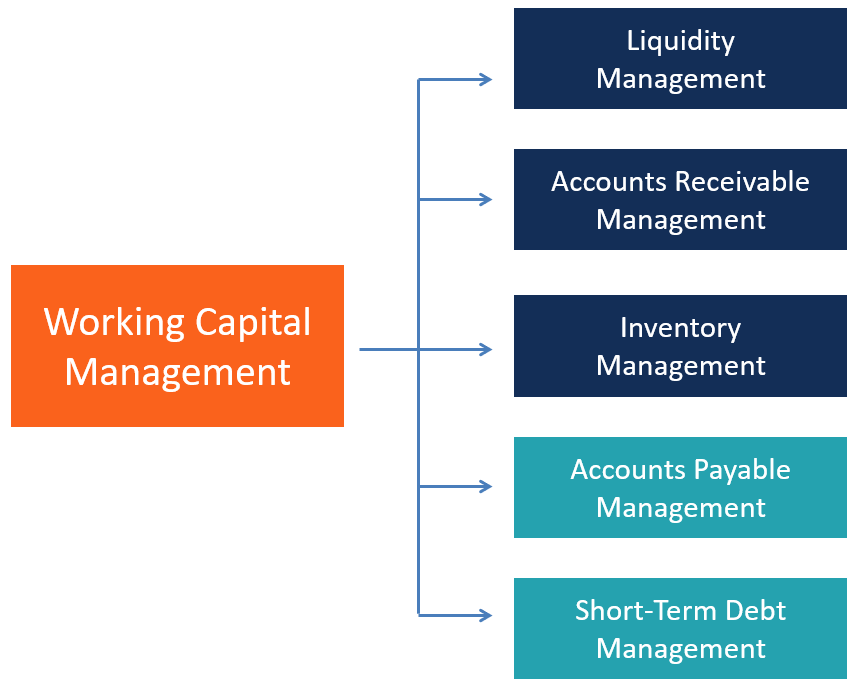

Working capital management refers to the set of activities performed by a company to ensure its resources are enough for day-to-day operating expenses while keeping resources invested in a productive way.

Working capital is the difference between a company’s current assets and its current liabilities.

Current assets include cash, accounts receivable, and inventories.

Current liabilities include accounts payable, short-term borrowings, and accrued liabilities.

Some approaches may subtract cash from current assets and financial debt from current liabilities.

Ensuring that the company possesses appropriate resources for its daily activities means protecting the company’s existence and ensuring it can keep operating as a going concern. Scarce availability of cash, uncontrolled commercial credit policies, or limited access to short-term financing can lead to the need for restructuring, asset sales, and even liquidation of the company.

Working capital needs vary from company to company. The factors that can affect working capital needs can be endogenous or exogenous.

Endogenous factors include a company’s size, structure, and strategy.

Exogenous factors include access to and availability of banking services, interest rate levels, industry type and products or services sold, macroeconomic conditions, and the size, number, and strategy of the company’s competitors.

Properly managing liquidity ensures that the company possesses enough cash resources for its ordinary business needs and unexpected needs of a reasonable amount. It’s also important because it affects a company’s creditworthiness, which can contribute to determining a business’s success or failure.

The lower a company’s liquidity, the more likely it is to face financial distress, other conditions being equal.

However, too much cash parked in low- or non-earning assets may reflect a poor allocation of resources.

Proper liquidity management is manifested at an appropriate level of cash and/or in the ability of an organization to quickly and efficiently generate cash resources to finance its business needs.

A company should grant its customers the proper flexibility or level of commercial credit while ensuring that the right amounts of cash flow in through operations.

A company will determine the credit terms to offer based on the customer’s financial strength, the industry’s policies, and the actual policies of competitors.

Credit terms can be ordinary, which means the customer generally is given a set number of days to pay the invoice (generally between 30 and 90). The company’s policies and the manager’s discretion can determine whether different terms are necessary, such as cash before delivery, cash on delivery, bill-to-bill, or periodic billing.

Inventory management aims to make sure that the company keeps an adequate level of inventory to deal with ordinary operations and fluctuations in demand without investing too much capital in the asset.

An excessive level of inventory means that an excessive amount of capital is tied to it. It also increases the risk of unsold inventory and potential obsolescence eroding the value of inventory.

A shortage of inventory should also be avoided, as it would determine lost sales for the company.

Like liquidity management, managing short-term financing should also focus on making sure that the company possesses enough liquidity to finance short-term operations without taking on excessive risk.

The proper management of short-term financing involves the selection of the right financing instruments and the sizing of the funds accessed via each instrument. Popular sources of financing include regular credit lines, uncommitted lines, revolving credit agreements, collateralized loans, discounted receivables, and factoring.

A company should ensure there will be enough access to liquidity to deal with peak cash needs. For example, a company can set up a revolving credit agreement well above ordinary needs to deal with unexpected cash needs.

Accounts payable arise from trade credit granted by a company’s suppliers, mostly as part of the normal operations. The right balance between early payments and commercial debt should be achieved.

Early payments may unnecessarily reduce the liquidity available, which can be put to use in more productive ways.

Late payments may erode the company’s reputation and commercial relationships, while a high level of commercial debt could reduce its creditworthiness.

Connect what you just learned to a clear career path with CFI’s role‑based courses and certification programs.

CFI is the official provider of the global Financial Modeling & Valuation Analyst (FMVA®) certification program, designed to help anyone become a world-class financial analyst. To keep advancing your career, the additional resources below will be useful: