Get Certified for Financial Modeling (FMVA)®

Gain in-demand industry knowledge and hands-on practice that will help you stand out from the competition and become a world-class financial analyst.

The difference between the purchase price paid for an asset and its actual fair market value

The negative goodwill (NGW) amount, also known as the “bargain purchase” amount, is the difference between the purchase price paid for an asset and its actual fair market value.

Negative goodwill is an accounting principle that occurs when the price paid for an asset is lower than its value in the market and can be thought of as a “discount” to the buyer.

It is important to distinguish between tangible and intangible assets:

Tangible assets come in a physical form and hold monetary value. Primary examples include property, plant, and equipment.

Intangible assets lack a physical form, do not hold monetary value, and can be unidentifiable at times. Examples of intangible assets include intellectual property (patents, copyrights), brand recognition, and useful life.

Goodwill accounts for the value of the intangible assets – such as brand recognition and intellectual property – which can be highly valuable for well-established and/or innovative companies. Intangible assets are not included in the calculation of the market value but may be included in the purchase price.

However, the presence of negative goodwill itself implies that the purchase price was lower than the market value – indicating that intangible assets had a discounted or no value or that the company is being sold under pressure without reaping the benefits of its intangible assets.

Therefore, negative goodwill implies that the selling company is under extremely unfavorable circumstances – it could either be financially distressed, under high selling pressure, and/or facing high debt obligations, which lead to a discount on the purchase price of a company.

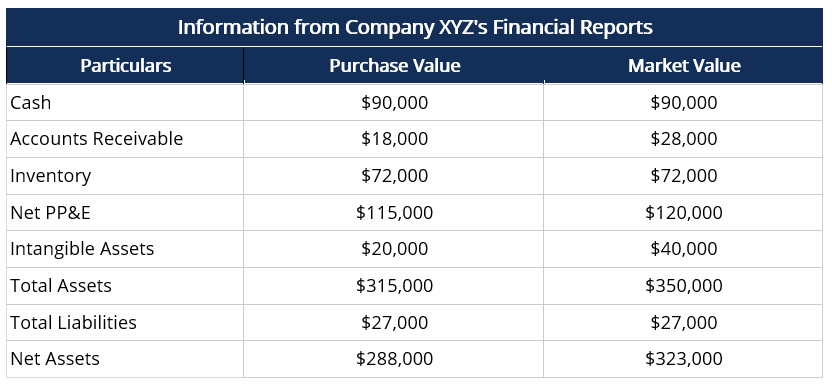

Company XYZ faced growing competition and incurred debt obligations that it could not cover. The board of directors had two choices – either file for bankruptcy or sell the company.

The company was recently sold for $288,000, which was lower than its fair market value. The table below reports consolidated information from Company XYZ’s financial statements:

Here:

Negative goodwill occurs when the purchase price paid for an asset is lower than its value in the market. In contrast, goodwill occurs when the purchase price is higher than its market value – i.e., the goodwill amount is the premium paid by the buyer for the intangible value of the company’s assets.

While negative goodwill is an indicator of unfavorable circumstances, the presence of goodwill (i.e., “positive” goodwill) implies that the intangible value of assets is high, and the company is under relatively low pressure to sell – this situation favors the seller.

Negative goodwill usually arises due to one of the following:

Companies that are financially distressed and under pressure to sell may be willing to sell the company at a discount in the form of negative goodwill since the value of intangible assets for a distressed firm is likely to be lower.

Valuation of assets, especially long-term fixed assets, may be incorrect – given that macroeconomic factors are constantly changing – and result in inaccurate market values. Similarly, an inaccurate valuation of intangible assets may also result in lower market values and negative goodwill.

According to US GAAP and IFRS, both goodwill and negative goodwill must be recognized and accounted for in the acquiring company’s financial statements.

Negative goodwill must be recognized as a “gain on acquisition” in the acquirer’s income statement, under non-cash sources of income.

In the balance sheet of the selling company, goodwill is recorded as an asset, whereas negative goodwill is part of the liabilities since it reduces the valuation. Alternatively, goodwill may be recorded as a contra-asset, or a reduction to assets to indicate the amount of NGW.

In the statement of cash flows, negative goodwill is usually recorded as a “gain on acquisition” or “gain on bargain purchase” to indicate the additional value acquired in the form of NGW.

Thank you for reading CFI’s guide to Negative Goodwill. To keep learning and advancing your career, the following resources will be helpful:

Below is a break down of subject weightings in the FMVA® financial analyst program. As you can see there is a heavy focus on financial modeling, finance, Excel, business valuation, budgeting/forecasting, PowerPoint presentations, accounting and business strategy.

A well rounded financial analyst possesses all of the above skills!

CFI is the global institution behind the financial modeling and valuation analyst FMVA® Designation. CFI is on a mission to enable anyone to be a great financial analyst and have a great career path. In order to help you advance your career, CFI has compiled many resources to assist you along the path.

In order to become a great financial analyst, here are some more questions and answers for you to discover: