Get Certified for Financial Modeling (FMVA)®

Gain in-demand industry knowledge and hands-on practice that will help you stand out from the competition and become a world-class financial analyst.

Strong financial analysis starts with a clear view of a company’s real earnings. But one-time gains and losses — known as non-recurring items — can distort financial statements, making it harder for you to assess financial results. That’s why you need to normalize income statements to remove these distortions, ensuring a clearer picture of ongoing business performance.

By adjusting for non-recurring items, you can build more reliable financial models for valuation and forecasting. In some cases, you may also adjust for recurring expenses to improve comparability across companies.

This guide walks you through the key adjustments you need to make to normalize an income statement effectively.

The first step in normalizing an income statement is identifying non-recurring items — but this isn’t always straightforward.

Finding these items requires a solid understanding of accounting and the ability to analyze financial statements with a critical eye. Some one-time items are obvious, like a large lawsuit settlement, but others are buried deep in financial reports.

The good news? Companies are usually willing to tell you what they think requires adjusting. Nearly every company in the S&P 500 reports adjusting items to present a “cleaner” version of earnings. These are typically labeled as:

Non-recurring items are often disclosed in:

Once you’ve identified non-recurring items, the next step is to understand why these adjustments matter and how they affect financial analysis.

Non-recurring items can significantly impact a company’s earnings, making it seem more or less profitable than it actually is. By adjusting for these events, analysts ensure that a company’s financial performance reflects only its ongoing operations and not temporary fluctuations.

Companies frequently report adjustments to their financials, either due to one-time charges (like a major lawsuit settlement) or accounting rules that may not fully capture financial reality.

The table below presents the most common types of non-recurring adjustments and how they affect the income statement.

| Restructuring Costs | Expenses from layoffs, closures, or reorganizations | Temporary increase in expenses, lowers net income |

| Mergers & Acquisitions (M&A) Costs | One-time legal, advisory, and integration costs | Increases expenses, lowers net income |

| Litigation or Regulatory Gains/Losses | Lawsuit settlements or government fines | Can either increase or decrease net income |

| Gains/Losses on Asset Sales | Profit or loss from selling non-operating assets | Creates one-time income or loss |

| Impairments and Reversals | Write-down or recovery of asset value | Reduces or increases reported earnings |

| Early Debt Extinguishment | Costs incurred when repaying loans early | One-time loss due to prepayment penalties |

| Discontinued Operations | Business segments being sold or shut down | Must be removed to assess ongoing operations |

Once these non-recurring items are identified, they must be removed or adjusted in financial models using the following steps:

Ready to master income statement adjustments and normalization? Enroll in CFI’s expert-led Normalizing Income Statements course!

Analysts sometimes adjust for recurring expenses to improve comparability across companies. These adjustments don’t eliminate one-time distortions but instead align accounting treatments across different companies.

Even though the following items appear on the income statement every year, they may distort financial comparisons due to differences in accounting treatment. Companies often encourage analysts to adjust for them so that financial metrics better reflect economic reality and increase comparability.

The table below provides a breakdown of common recurring adjustments and the reasons why these items need adjusting.

| Stock-Based Compensation | Non-cash expense, affects EPS but not cash flow |

| Amortization of Acquired Intangibles | Creates inconsistencies between companies that acquire vs. internally develop assets |

| Amortization of Debt Discounts | Non-cash accounting expense, does not impact actual interest payments |

| LIFO vs. FIFO Adjustments | Ensures comparability between companies using different inventory accounting methods |

Once non-recurring items have been removed, there’s one more critical adjustment — taxes. Since many of the items analysts adjust are tax-deductible expenses, removing them increases taxable income, which means taxes must be adjusted accordingly.

Conversely, if a company’s reported income includes one-time gains, then removing them lowers taxable income, requiring a downward tax adjustment.

Ignoring tax implications can lead to inaccurate financial models. If analysts remove a large non-recurring expense but fail to increase tax expenses accordingly, they overstate adjusted net income.

A company reports a $933 million non-recurring expense in its financials. If this expense is removed, the tax adjustment must reflect the additional taxable income.

Assuming a 25% tax rate, the tax adjustment is calculated as:

$933M × 25%= $233M

This means $233 million in additional tax expense should be accounted for in the normalized income statement.

By correctly adjusting for taxes, analysts ensure that normalized net income reflects post-tax profitability, leading to more accurate comparisons and valuation models.

Now that we’ve removed non-recurring items and adjusted taxes, we can calculate the final normalized net income and assess a company’s true ongoing profitability.

Note that normalization directly impacts key financial metrics, including:

A company’s reported earnings might make it look more or less profitable than it truly is. Normalization ensures analysts can:

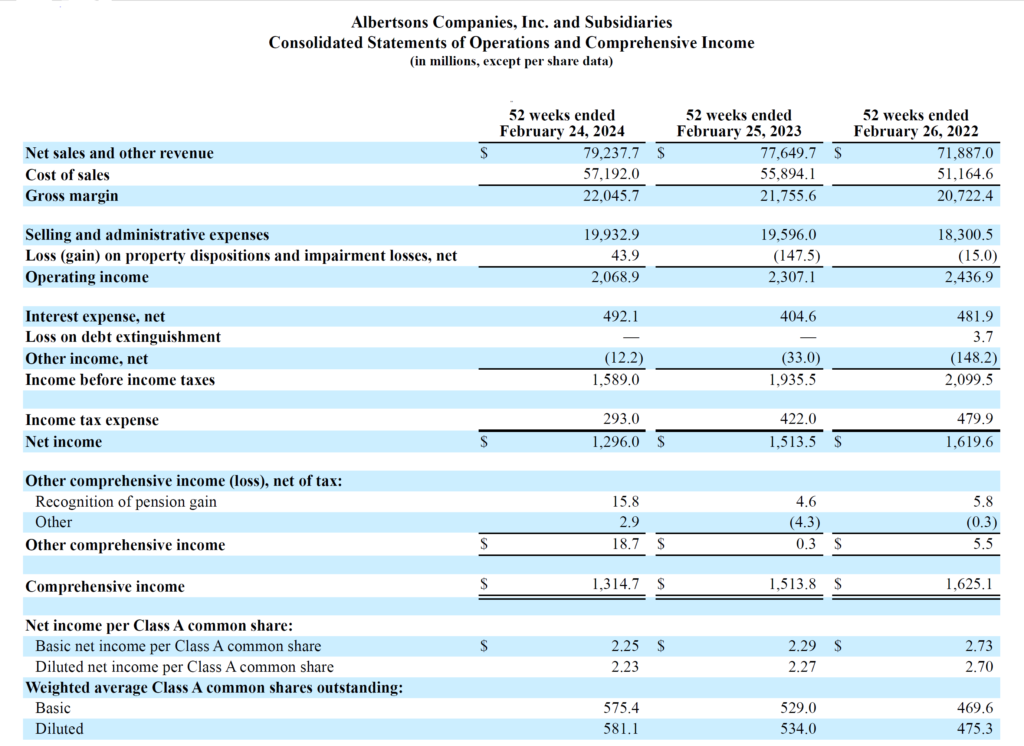

Albertsons, a U.S. grocery chain, follows GAAP and includes several non-recurring items in its income statements. Analysts must adjust for these items to compare Albertsons’ profitability with competitors that follow different accounting standards (e.g., those using FIFO instead of LIFO for inventory valuation).

By making these adjustments, analysts ensure that Albertsons’ earnings reflect ongoing operations, making it easier to compare against competitors that use different accounting methods.

Ready for hands-on practice by normalizing real companies’ income statements? Enroll in CFI’s expert-led Normalizing Income Statements course!

Understanding how to normalize an income statement is critical for financial analysts, investors, and corporate finance professionals. Whether you’re analyzing a company for investment, building financial projections, or conducting due diligence, normalized income statements give you a more accurate foundation for decision-making.

Ready to dive deeper into normalizing income statements? Enroll in CFI’s Normalizing Income Statements course for expert instruction in analyzing and adjusting income statements for accurate financial analysis and decision-making.

Enroll in Normalizing Income Statements Now!

Analyzing Financial Statements: Key Metrics and Methods

Essential Guide to Accounting for Financial Analysts

How the Three Financial Statements are Linked