Get Certified for Financial Modeling (FMVA)®

Gain in-demand industry knowledge and hands-on practice that will help you stand out from the competition and become a world-class financial analyst.

An important measure of profitability for a business

Operating margin, also known as return on sales, is an important profitability ratio measuring revenue after the deduction of operating expenses. It is calculated by dividing operating income by revenue. The operating margin indicates how much of the generated sales is left when all operating expenses are paid off.

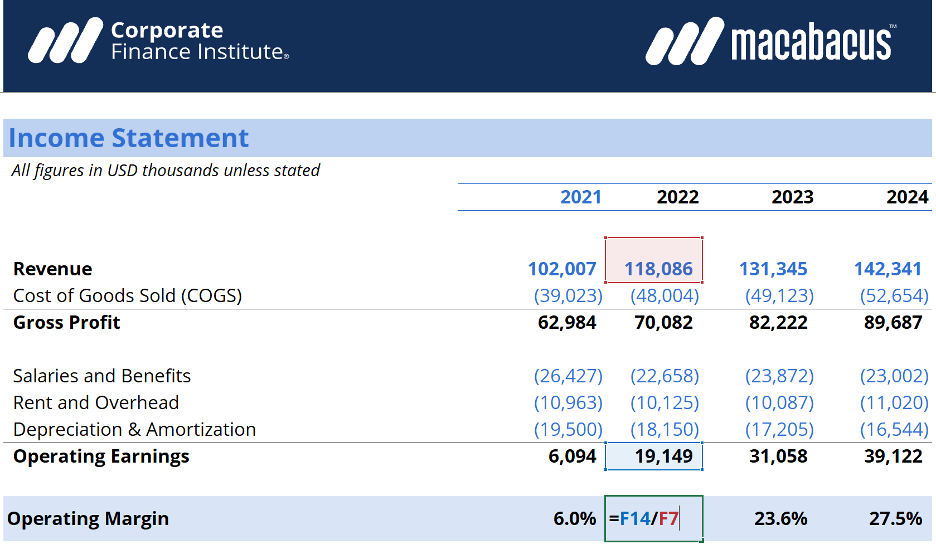

In the above example, you can clearly see how to arrive at the 2022 operating margin for this company. 2022 has revenue of $118.1 million, less COGS of $48.0 million, resulting in gross profit of $70.1 million.

From there, another $22.7 million of salaries and benefits, $10.1 million of rent and overhead and $18.2 million of depreciation and amortization expenses are deducted, to arrive at operating income of $19.1 million.

By taking $19.1 million and dividing it by $118.1 million in revenue, we arrive at an operating margin of 16.2%, which is why operating margin is sometimes referred to as return on sales.

Another example: DT Clinton Manufacturing company reported on $125 million in revenue in its 2022 annual income statement. Operating income before tax was $45 million after deducting $80 million in operating expenses for the year. As a result, the company has an operating margin of 36%. In other words, for every dollar in sales achieved, $0.36 cents is retained as operating profit.

A business that can generate operating profit rather than operating at a loss is a positive sign for potential investors and existing creditors. This means that the company’s operating margin creates value for shareholders and continuous loan servicing for lenders. The higher the margin a company has, all things being equal, the less financial risk it has. However, different industries will have different operating margins so any comparisons made should be relative to other, similar companies in the same industry.

Continued increases in profit margin over time shows that profitability is improving. This may either be attributed to efficient control of operating costs or other factors that influence revenue, such as higher pricing, better marketing and increases in customer demand.

Operating profit is an accounting metric and, therefore, not an indicator of economic value or cash flow. Profit includes several non-cash expenses such as depreciation and amortization, stock-based compensation, and other items. Conversely, it doesn’t include capital expenditures and changes in working capital.

In conjunction, these various items that are included or excluded can cause cash flow (the ultimate driver of value for a business) to be very different (higher or lower) than operating profit.

To learn more, read all about business valuation.

Connect what you just learned to a clear career path with CFI’s role‑based courses and certification programs.