Get Certified for Financial Modeling (FMVA)®

Gain in-demand industry knowledge and hands-on practice that will help you stand out from the competition and become a world-class financial analyst.

The ratio of the company’s retained income to its net income

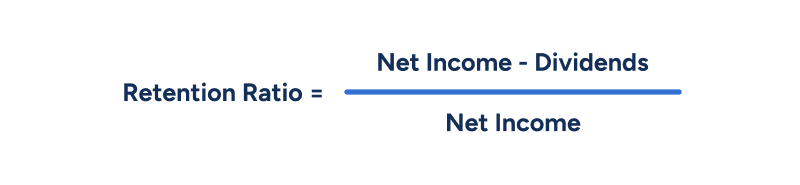

The retention ratio (also known as the net income retention ratio or plowback ratio) is the ratio of a company’s retained income to its net income. The retention ratio measures the percentage of a company’s profits that are reinvested into the company in some way, rather than being paid out to investors as dividends.

There is a simple formula for calculating the retention ratio: divide a company’s retained income by its net income.

Net income can be found at the bottom of a business’ income statement, and the dividend figure can either be found in the shareholder’s equity section of the balance sheet or in the financing section of the cash flow statement.

The ratio can also be calculated on a per-share basis.

Alternatively, the retention ratio can also be calculated as 1 minus the dividend payout ratio.

Click the button below to download our free Retention Ratio template!

* By submitting your email address, you consent to receive email messages (including discounts and newsletters) regarding Corporate Finance Institute and its products and services and other matters (including the products and services of Corporate Finance Institute's affiliates and other organizations). You may withdraw your consent at any time.

This request for consent is made by Corporate Finance Institute, #1392 - 1771 Robson Street, Vancouver, BC V6G 3B7, Canada. www.corporatefinanceinstitute.com. [email protected]. Please click here to view CFI`s privacy policy.

Alice owns a software business that focuses on web design. She’s been in business for three years and wants to calculate her business’ retention ratio. In year 1, Alice’s recorded a net income of $1,000 and did not pay any dividends. In year 2, Alice posted a net income of $5,000 and paid out $500 in dividends. In year 3, Alice reported a net income of $15,000 and paid out a total of $1,000 in dividends.

Using the formula above, we can calculate the retention ratio for each period:

In the example above, we can see that the retention ratio for Alice’s business is going down each year. This is because net income is rising each year and dividends are rising by a proportionally larger amount, leading to a downward trend in the ratio.

The change may be indicative of the business’ lack of focus on growth as it chooses to give out its earnings to shareholders rather than reinvest them into the business. To understand whether that is a good thing or a bad thing, we should compare the figure to the ratio of Alice’s competitors in the industry.

A high retention ratio may not always be indicative of financial health. To better understand the retention ratio, we must first understand the company that we are calculating the ratio for.

Smaller, newer companies will typically report higher retention ratios. Smaller businesses tend to prioritize business development and investments in research and development (R&D), which can be a reason why they are more likely to retain their earnings rather than distribute them as dividends. A startup business may also be experiencing slow sales in the early stages of business, which would mean that there is less income to distribute to shareholders, thus resulting in a higher retention ratio.

Larger, more mature companies will usually post lower retention ratios, as they are already quite profitable and do not need to invest as heavily in R&D. Thus, such companies may opt to pay investors consistent dividends in preference to retaining more earnings.

As with any financial ratio, there is not much meaning behind a single or standalone number. In order to draw meaningful insights, analysts consider the ratio in relation to the ratios of similar companies operating in the same industry. This makes it easier to compare one company to another in terms of their earnings retention.

Ratios can also be looked at over a period of time in order to observe trends and year-over-year changes in the metric. This enables analysts to evaluate changes in the company’s performance over a given time interval.

Forecasting Balance Sheet Line Items