Get Certified for Financial Modeling (FMVA)®

Gain in-demand industry knowledge and hands-on practice that will help you stand out from the competition and become a world-class financial analyst.

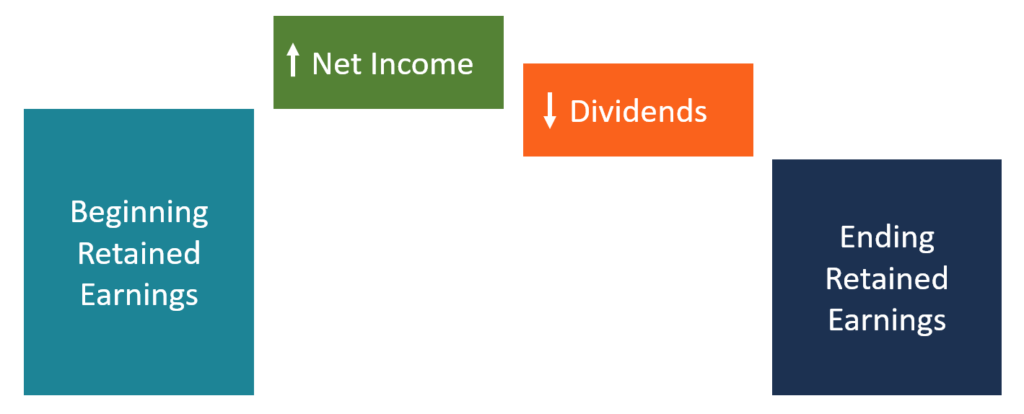

An overview of the changes in retained earnings during a specific accounting cycle

The statement of retained earnings provides an overview of the changes in a company’s retained earnings during a specific accounting cycle. It is structured as an equation, such that it opens with the retained earnings at the beginning of the reporting period, makes adjustments for items such as net income and dividends, and closes with the retained earnings balance for that accounting cycle. The closing balance for that accounting cycle forms the opening balance for the next accounting period of the company.

The statement of retained earnings can be created as a standalone document or be appended to another financial statement, such as the balance sheet or income statement. The statement can be prepared to cover a specified cycle, either monthly, quarterly or annually. In the United States, it is required to follow the Generally Accepted Accounting Principles (GAAP).

The statement of retained earnings is mainly prepared for outside parties such as investors and lenders, since internal stakeholders can already access the retained earnings information. Some of the information that external stakeholders are interested in is the net income that is distributed as dividends to investors.

Retained earnings are the profits that the company keeps for use internally or for when a need arises. The profits may be reinvested into certain revenue-generating activities of the company or used to make debt repayments. Other possible uses of retained earnings include:

The company may use the retained earnings to fund an expansion of its operations. The funds may go into building a new plant, upgrading the current infrastructure, or hiring more staff to support the expansion.

A company may also use the retained earnings to finance a new product launch to increase the company’s list of product offerings. For example, a beverage processing company may introduce a new flavor or launch a completely different product that boosts its competitive position in the marketplace.

The surplus can be distributed to the company’s shareholders according to the number of shares they own in the company.

During the growth phase of the business, the management may be seeking new strategic partnerships that will increase the company’s dominance and control in the market.

A merger occurs when the company combines its operations with another related company with the goal of increasing its product offerings, infrastructure, and customer base. An acquisition occurs when the company takes over a same-size or smaller company within its industry.

The statement of retained earnings is usually condensed and does not include as much information as other financial statements. The following are the main steps involved when calculating the retained earnings balance at the end of the reporting period:

The starting balance in the statement of retained earnings is carried over from the retained earnings balance of the previous period. The beginning balance is obtained, for example, from the balance sheet of the previous year. For example, assume that the retained earnings balance for the previous year is $100,000. The figure will be recorded as follows:

Beginning Retained Earnings Balance: $100,000

The next step is to add the net income (or net loss) for the current accounting period. The net income is obtained from the company’s income statement, which is prepared first before the statement of retained earnings. Assume that the net income for the current period is $50,000.

Beginning Retained Earnings Balance: $100,000

Add: Net Income $50,000

Note: If the company incurred a net loss of $50,000, the amount should be deducted from the beginning balance.

If the company paid dividends to investors in the current year, then the amount of dividends paid should be deducted from the total obtained from adding the starting retained earnings balance and net income. If the company did not pay out any dividends, the value should be indicated as $0. Let us assume that the company paid out $30,000 in dividends out of the net income.

Beginning Retained Earnings Balance: $100,000

Add: Net Income $50,000

Less: Dividends ($30,000)

Finally, calculate the amount of retained earnings for the period by adding net income and subtracting the amount of dividends paid out. The ending retained earnings balance is the amount posted to the retained earnings on the current year’s balance sheet.

Beginning Retained Earnings Balance: $100,000

Add: Net Income $50,000

Total: $150,000

Less: Dividends ($30,000)

Ending Retained Earnings Balance $120,000

The following are the two main users of the statement of retained earnings:

As shareholders of the company, investors are looking to benefit from increased dividends or a rising share price due to the company’s continued profitability. Investors look at the current year’s and previous year’s retained earnings balance to predict future dividend payments and growth in the company’s share price.

Lenders are interested in knowing the company’s ability to honor its debt obligations in the future. Lenders want to lend to established and profitable companies that retain some of their reported earnings for future use. Even if the company is experiencing a slowdown in business activities, it can still make use of the retained earnings to pay down its debt obligations.

CFI offers the Financial Modeling & Valuation Analyst (FMVA)™ certification program for those looking to take their careers to the next level. To keep learning and advancing your career, the following CFI resources will be helpful:

Below is a break down of subject weightings in the FMVA® financial analyst program. As you can see there is a heavy focus on financial modeling, finance, Excel, business valuation, budgeting/forecasting, PowerPoint presentations, accounting and business strategy.

A well rounded financial analyst possesses all of the above skills!

CFI is the global institution behind the financial modeling and valuation analyst FMVA® Designation. CFI is on a mission to enable anyone to be a great financial analyst and have a great career path. In order to help you advance your career, CFI has compiled many resources to assist you along the path.

In order to become a great financial analyst, here are some more questions and answers for you to discover: