Get Certified for Financial Modeling (FMVA)®

Gain in-demand industry knowledge and hands-on practice that will help you stand out from the competition and become a world-class financial analyst.

A common investment banking interview question

If you’re going for an investment banking interview, you’re almost guaranteed to get a question along the lines of… “Walk me through a DCF analysis” or, “How would you build a DCF model?”

The super-fast answer is: Build a 5-year forecast of unlevered free cash flow based on reasonable assumptions, calculate a terminal value with an exit multiple approach, and discount all those cash flows to their present value using the company’s WACC.

Of course, it’s also a bit more complicated than that… To answer this interview question in more detail, we’ve broken it down into several basic steps below.

The key to answering “Walk me through a DCF” is a structured approach… and lots of direct experience building DCF models in Excel.

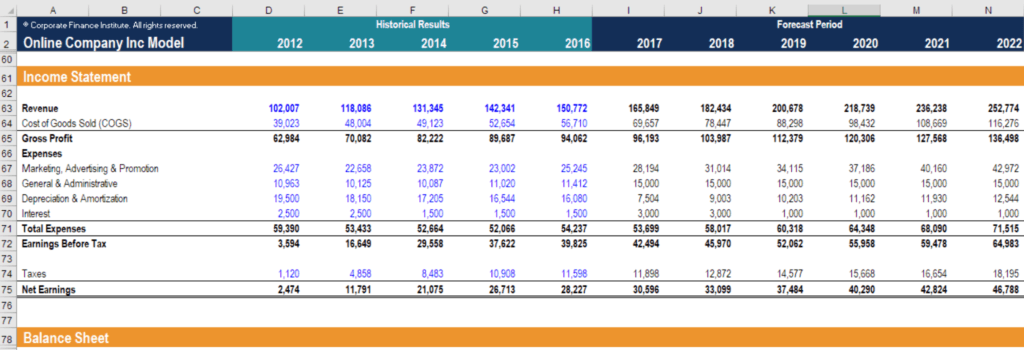

Screenshot of a DCF model from CFI’s online financial modeling courses!

Enter your name and email in the form below and download our free DCF Model template now!

The first step in the DCF model process is to build a forecast of the three financial statements based on assumptions about how the business will perform in the future. On average, this forecast typically goes out about five years. Of course, there are exceptions, and it may be longer or shorter than this.

The forecast has to build up to unlevered free cash flow (free cash flow to the firm or FCFF). We’ve published a detailed guide on how to calculate unlevered free cash flow, but the quick answer is to take EBIT, less capital expenditures, plus depreciation and amortization, less any increases in non-cash working capital.

See our ultimate cash flow guide to learn more about the various types of cash flows.

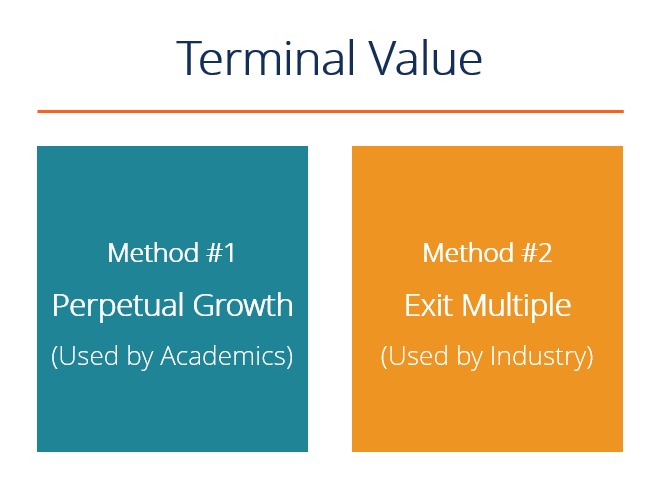

We continue walking through the DCF model by calculating the terminal value. There are two approaches to calculating a terminal value: perpetual growth rate and exit multiple.

In the perpetual growth rate technique, the business is assumed to grow it’s unlevered free cash flow at a steady rate forever. This growth rate should be fairly moderate, otherwise, the company would become unrealistically large. This poses a challenge for valuing early-stage, high-growth businesses.

With the exit multiple approach, the business is assumed to be sold based on a valuation multiple, such as EV/EBITDA. This multiple is typically based on comparable company analysis. This method is more common in investment banking.

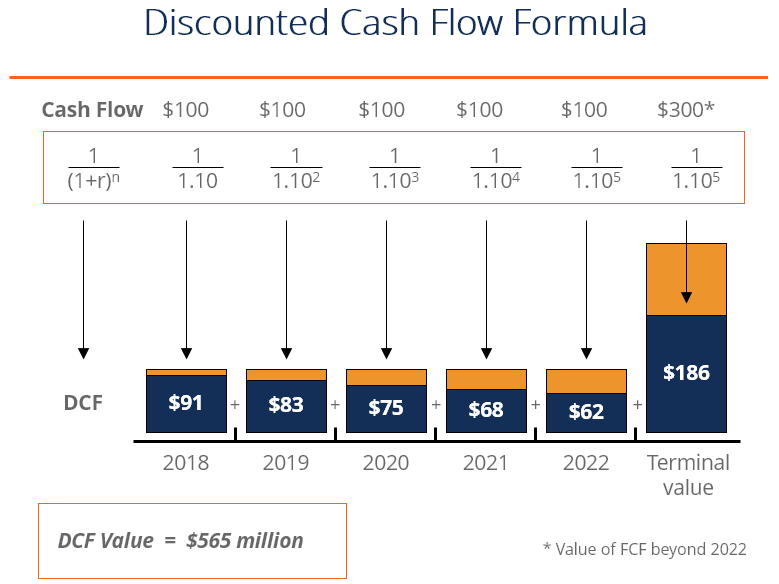

In step 3 of this DCF walk-through, it’s time to discount the forecast period (from step 1) and the terminal value (from step 2) back to the present value using a discount rate. The discount rate is almost always equal to the company’s weighted average cost of capital (WACC).

See our guide to calculating WACC for more details on the subject, but the quick summary is that this represents the required rate of return investors expect from the company and thus represents its opportunity cost.

The best way to calculate the present value in Excel is with the XNPV function, which can account for unevenly spaced out cash flows (which are very common).

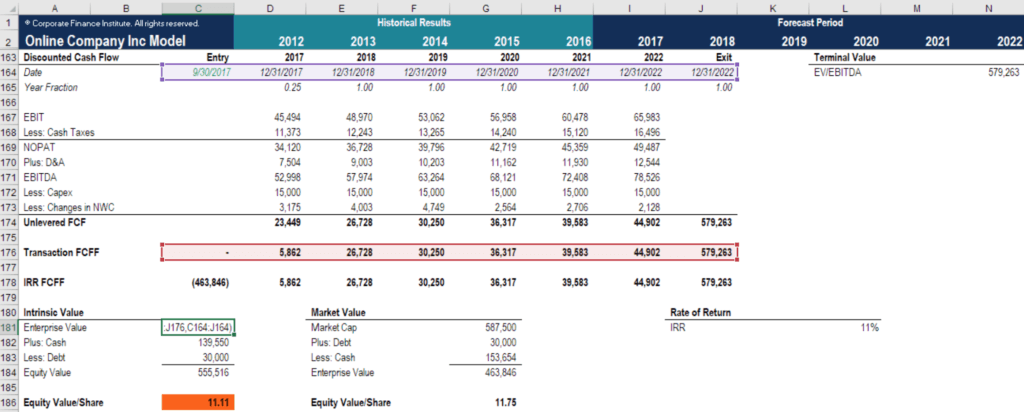

At this point, we’ve arrived at the enterprise value for the business since we used unlevered free cash flow. It’s possible to derive equity value by subtracting any debt and adding any cash on the balance sheet to the enterprise value. See our guide on equity value vs. enterprise value.

At this point in the modeling process, an investment banking analyst will typically perform extensive sensitivity and scenario analysis to determine a reasonable range of values for the business, as opposed to arriving at a singular value for the company. By now, you’ve really satisfied the question of “Walk me through a DCF analysis.”

Now you’re all set to properly answer “Walk me through a DCF model” or “How do you perform a discounted cash flow analysis” in an interview.

CFI is the official provider of the global Financial Modeling and Valuation Analyst (FMVA)® certification program, designed to help anyone become a world-class financial analyst.

To make sure you’ll be completely prepared, check out these additional resources below: