Get Certified for

Commercial Banking (CBCA®)

Stand out and gain a competitive edge as a commercial banker, loan officer, or credit analyst with advanced knowledge, real-world analysis skills, and career confidence.

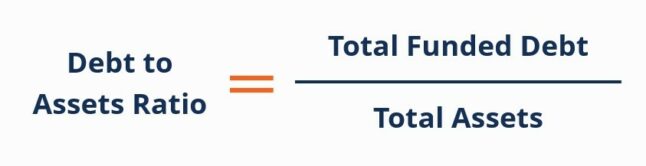

Measuring the proportion of a company’s assets that are funded by debt

The debt to asset ratio is a financial metric used to help understand the degree to which a company’s operations are funded by debt. It is one of many leverage ratios that may be used to understand a company’s capital structure.

The debt to asset ratio is calculated by using a company’s funded debt, sometimes called interest bearing liabilities. This refers to actual credit provided by direct lenders for which there are interest obligations (like bonds, term loans from a commercial bank, or subordinated debt); the ratio does not include total liabilities (like accounts payable, etc.).

The total funded debt — both current and long term portions — are divided by the company’s total assets in order to arrive at the ratio. This ratio is sometimes expressed as a percentage (so multiplied by 100).

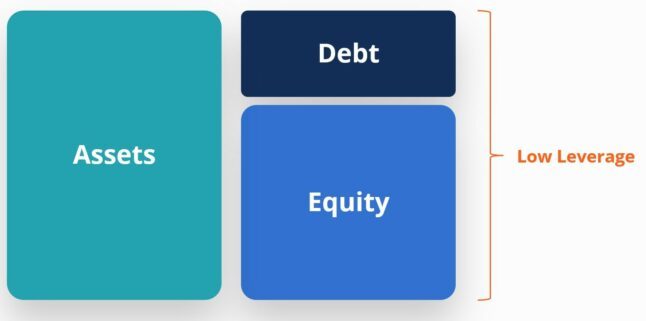

The fundamental accounting equation is Assets = Liabilities + Equity. And while not all liabilities are funded debt, the equation does imply that all assets are funded either by debt or by equity.

A company with a higher proportion of debt as a funding source is said to have high leverage.

A company with a lower proportion of debt as a funding source is said to have low leverage.

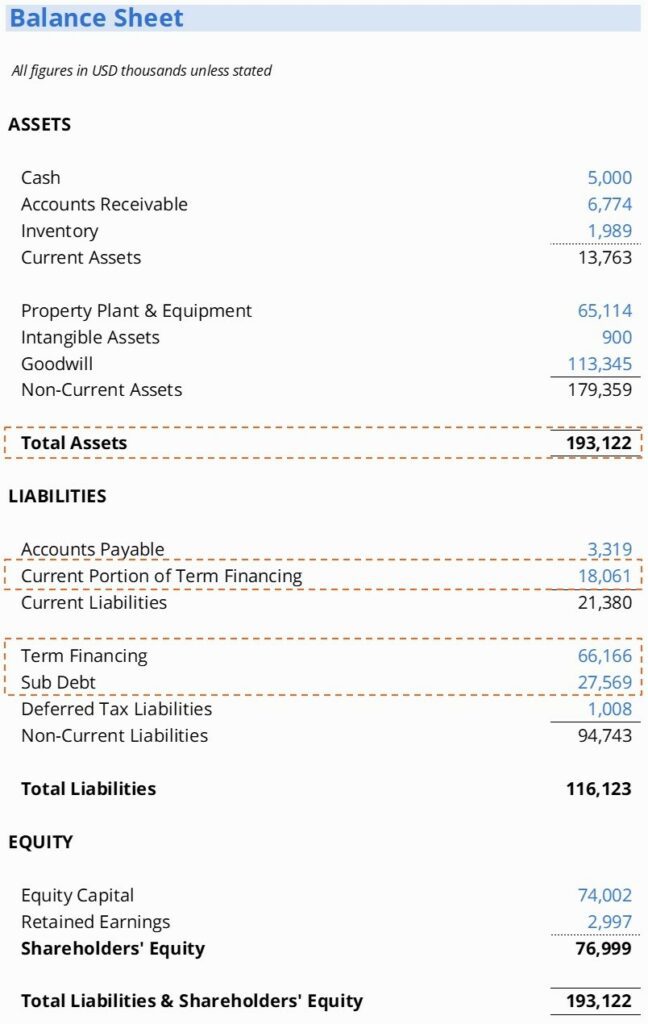

Looking at the following balance sheet, we can see that this company has employed funded debt in its capital structure.

In order to calculate the debt to asset ratio, we would add all funded debt together in the numerator: (18,061 + 66,166 + 27,569), then divide it by the total assets of 193,122.

In this case, that yields a debt to asset ratio of 0.5789 (or expressed as a percentage: 57.9%).

Of all the leverage ratios used by the analyst community to understand the financial position of a company, debt to assets tends to be one of the less common ones.

It represents the proportion (or the percentage of) assets that are financed by interest bearing liabilities, as opposed to being funded by suppliers or shareholders. As a result it’s slightly more popular with lenders, who are less likely to extend additional credit to a borrower with a very high debt to asset ratio.

In the above-noted example, 57.9% of the company’s assets are financed by funded debt. As with any ratio, however, it can’t be taken in isolation. Analysts will want to compare figures period over period (to assess the ratio over time), or against industry peers and/or a benchmark (to measure its relative performance).

A valid critique of this ratio is that the proportion of assets financed by non-financial liabilities (accounts payable in the above example, but also things like taxes or wages payable) are not considered. In other words, the ratio does not capture the company’s entire set of cash “obligations” that are owed to external stakeholders – it only captures funded debt.

There is no perfect score or ideal debt to asset ratio. As with all financial metrics, a “good ratio” is dependent upon many factors, including the nature of the industry, the company’s lifecycle stage, and management preference (among others).

Some important considerations include the following:

Connect what you just learned to a clear career path with CFI’s role‑based courses and certification programs.

Financial Analysis Fundamentals