VantageScore

A credit rating service that caters directly to individual consumers

What is VantageScore?

VantageScore is a credit rating service that caters directly to individual consumers. It is a credit rating product that was jointly developed by three credit rating bureaus, i.e., Equifax, Experian, and TransUnion. The product was created as an alternative to the FICO score, which was developed by the Fair Isaac Corporation.

Summary

- VantageScore is a credit rating service that caters directly to individual consumers.

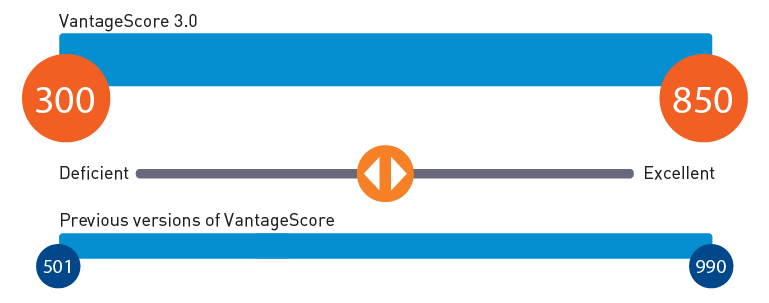

- The scores generated by VantageScore fall between 300 and 850 (VantageScore 3.0).

- The credit rating service also provides an alphabetical score, ranging from A to F.

What is a Credit Rating?

Credit ratings are essentially an assessment of the creditworthiness of a borrower, and they can be expressed in quantifiable terms by credit rating agencies. A credit rating may be assigned either in general terms or as associated with a particular debt or financial obligation. The rating may be assigned to any entity seeking to borrow capital, namely, an individual, a corporation, or even a sovereign government.

A credit score, on the other hand, is assigned to individual consumers. VantageScore provides credit scores.

How is VantageScore Calculated?

Initially launched in 2006, VantageScore uses a different metric to evaluate the creditworthiness of a customer. To arrive at the score, a weighted average of key factors of a consumer’s repayment capacity is calculated. The key determinants include the following:

- Consumer’s available credit

- Consumer’s recent credit – Refers to the total number of hard inquiries that may have been made into a consumer’s account.

- Consumer’s payment history – Includes whether or not the consumer has a steady track record of making their bill payments in full and on time.

- Consumer’s credit utilization in the past – Refers to the total revolving credit that is used by the consumer and is expressed in terms of a percentage of funds utilized. For example, if a borrower utilizes only $5,000 out of a total of $10,000 worth of credit available to her, then her utilization stands at 50%

- Consumer’s depth of credit – Entails the number of years for which the borrower has had a credit record. Borrowers with a higher depth of credit are considered to be more reliable. Depth of credit also includes the number and type of credit accounts they currently hold or have operated in the past.

- Consumer’s current credit balances – Refers to the total outstanding loans currently owed by the borrower.

How Does the VantageScore Work?

Borrowers with a VantageScore of under 630 are considered to have poor credit. A credit rating that is anywhere between 630 and 690 is considered to be the average. A rating that falls between 690 and 720 is considered a good credit score.

A VantageScore of over 720 is considered an excellent score. Thus, the higher the credit score of the consumer, the higher the likelihood of paying back the principal amount of the debt on time. Credit ratings, hence, are inversely proportional to the risk undertaken by the lender.

In order to provide a parallel to the numerical score assigned by it, VantageScore also provides an alphabetical score, which ranges from A to F. A determination of A represents the highest level of creditworthiness, while a score of F represents the lowest level.

Similarities between VantageScore and FICO Score

Both VantageScore and FICO place the greatest weight on two metrics – payment history and credit utilization.

Both agencies use models of statistical analyses in order to predict the likelihood of the borrower paying a loan back on time or defaulting on it. In order to operate their models, they collate data from the consumer credit files compiled and maintained by the three credit rating agencies.

Both the credit rating services’ models numerically represent the risk of loan defaults by assigning three-digit scores. A higher score indicates a lower risk for the lender and vice versa.

Differences between VantageScore and FICO Score

The scores generated by VantageScore fall between 501 and 990. On the other hand, the scored generated by FICO fall within the range of 300 and 850.

FICO develops scores using data collected separately by each credit reporting agency. On the other hand, VantageScore uses a combination of data made available by all three bureaus to run its statistical analysis.

More Resources

CFI offers the Commercial Banking & Credit Analyst (CBCA)™ certification program for those looking to take their careers to the next level. To keep learning and developing your knowledge base, please explore the additional relevant resources below: