Get Certified for

Capital Markets (CMSA®)

From equities and fixed income to derivatives, the CMSA certification bridges the gap from where you are now to where you want to be — a world-class capital markets analyst.

Agents in financial markets demonstrate a preference for liquidity

The Theory of Liquidity Preference states that agents in financial markets demonstrate a preference for liquidity. Formally, if U(Asset A) > U(Asset B) and rA = rB, then L(Asset A) > L(Asset B), where:

Under the Theory of Liquidity Preference, an investor faced with two assets offering the same rate of return will always choose the more liquid asset. The term liquidity preference was introduced by English economist John Maynard Keynes in his 1936 book, “The General Theory of Employment, Interest, and Money.” Keynes called the aggregate demand for money in the economy liquidity preference.

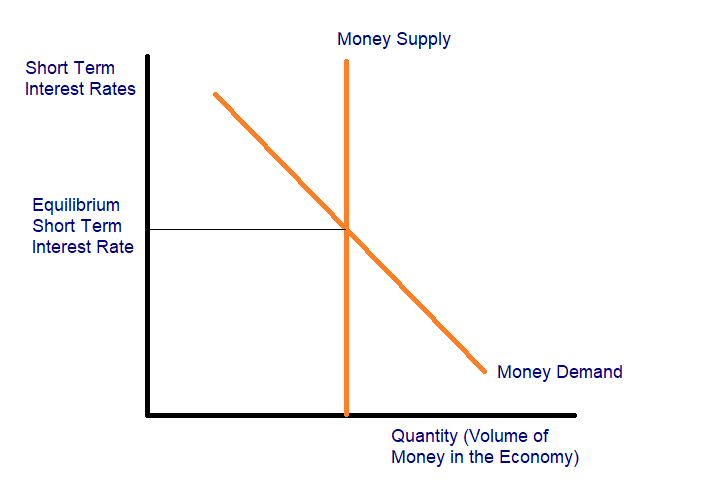

According to Keynes General Theory, the short-term interest rate is determined by the supply and demand for money. Holding money is the opportunity cost of not investing that money in short-term bonds. The demand for money is a function of the short-term interest rate and is known as the liquidity preference function.

Money supply is usually a fixed quantity set by a central banking authority. L(r,Y) is a liquidity preference function if and if , where r is the short-term interest rate and Y is the level of output in the economy.

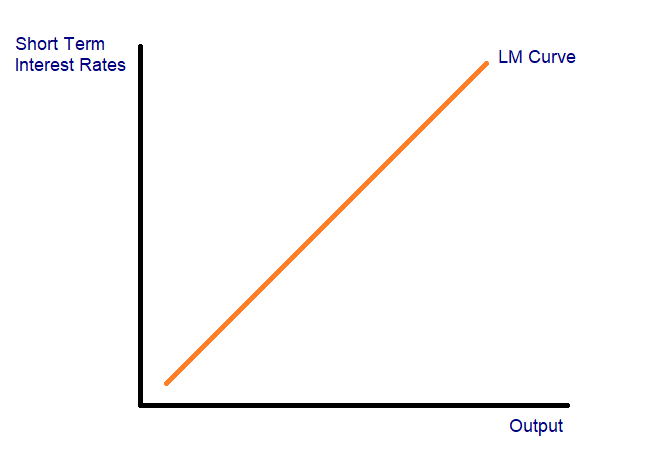

Formally, the liquidity money (LM) curve is the locus of points in Output – Interest Rate space such that the money market is in equilibrium. Alternatively, we can say that the LM curve maps changes in money demand or supply to changes in the short-term interest rate.

According to the Theory of Liquidity Preference, the short-term interest rate in an economy is determined by the supply and demand for the most liquid asset in the economy – money. The concept, when extended to the bond market, gives a clear explanation for the upward sloping yield curve. Since investors strictly prefer liquidity, in order to persuade investors to buy long-term bonds over short-term bonds, the return offered by long-term bonds must be greater than the return offered by short-term bonds.

Formally, if U(Asset A) > U(Asset B), and L(Asset A) > L(Asset B), then rA > rB. The difference in interest rates is known as the liquidity premium or the term premium. A commonly used measure of the term premium is the 10-2 spread.

The Theory of Liquidity Preference is a special case of the Preferred Habitat Theory in which the preferred habitat is the short end of the term structure. The Preferred Habitat Theory states that the market for bonds is ‘segmented’ on the basis of the bonds’ term structure, and these “segmented” markets are linked on the basis of the preferences of bond market investors.

Under the Preferred Habitat Theory, bond market investors prefer to invest in a specific part or “habitat” of the term structure. The theory was introduced by Italian-American economist Franco Modigliani and American economic historian Richard Sutch in their 1966 paper titled “Innovations in Interest Rates Policy.”

Thank you for reading CFI’s guide on the Theory of Liquidity Preference. To keep learning and developing your knowledge of financial analysis, we highly recommend the additional resources below: