Backstop

A financial arrangement that creates a secondary source of funds in case the primary source is insufficient

What is a Backstop?

A backstop is a financial arrangement that creates a secondary source of funds in case the primary source is not enough to meet current needs. It can also be thought of as an insurance policy that covers the inadequacy of a source of funds.

The backstop can take various forms in different contexts. The following are three applications that will be discussed in some detail in later sections:

- Backstop in underwriting

- Private equity backstop

- Backstop in financial management

Backstop in Underwriting

The most common use of a backstop is seen in underwriting share issues or initial public offerings (IPOs). In an IPO, a company wishing to raise equity capital issues its shares to the public. The issues are underwritten by an investment bank or a group of investment banks.

If a company is unable to sell all its shares to the public, then the underwriter provides a backstop provision. Under the provision, the underwriter will buy the remaining shares that were not bought by the public.

Such an arrangement is provided in exchange for a backstop fee, which is typically calculated as a percentage of the total issue.

Example

Consider a company that wishes to raise equity capital and issues 500 shares. Of the 500, only 400 shares are bought by the public. If the company did not enter into a backstop arrangement, then it must work with a lesser amount.

On the other hand, the company can pay a small fee and sell the remaining shares to the underwriters. Hence, they will be able to meet their funding requirements more closely. The following tables illustrate the two scenarios:

Private Equity Backstop

A private equity firm typically uses the leveraged buyout (LBO) method to acquire target companies. Under the LBO method, the firm finances the purchase of the target using mostly debt and contributes the remainder in the form of equity.

A private equity backstop, also known as the full equity backstop, is an arrangement in which a private equity firm agrees to buy the target company by contributing equity up to 100% in case it fails to raise the required debt to fund the purchase.

The private equity firm employs such a strategy with a significant potential loss to itself. It is significant because it essential to use a larger portion of debt compared to equity in an LBO strategy. Hence, a full equity backstop mostly uses an aggressive posturing tool in negotiations to make the deal more attractive to the target company and raise the stakes for the competition.

Backstop in Financial Management

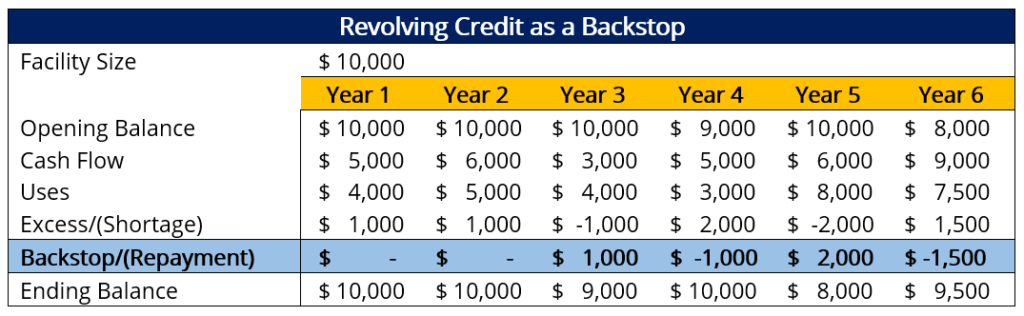

Another important application of the backstop is in the day-to-day financial management of a company. The backstop typically takes the form of a revolving credit facility. A revolving credit facility is a simple short-term lending arrangement where the borrower is allowed to borrow a certain amount up to a maximum every year or a shorter period.

A revolving credit facility can be used as a backstop to fulfill any shortage of funds that might arise in the short term.

For example, in the table below, the company faces a shortage of $1,000 in Year 3. The company can use the revolving credit facility as a secondary source of financing to borrow $1,000 and meet all its financial obligations for the year. Hence, a revolving credit facility acts as a backstop for the short-term financing needs of the business.

Additional Resources

CFI is the official provider of the global Commercial Banking & Credit Analyst (CBCA)™ certification program, designed to help anyone become a world-class financial analyst. To keep advancing your career, the additional CFI resources below will be useful: