Get In-Demand Finance Certifications

Costs incurred from the issuance of securities

Flotation costs are the costs that are incurred by a company when issuing new securities. The costs can be various expenses including, but not limited to, underwriting, legal, registration, and audit fees. Flotation expenses are expressed as a percentage of the issue price.

After the flotation costs are determined by a company, the expenses are incorporated into the final price of the issued securities. Essentially, the incorporation of the costs reduces the final price of the issued securities and subsequently lowers the amount of capital that a company can raise.

The size of flotation expenses depends on many factors, such as the type of issued securities, their size, and risks associated with the transaction. Note that the costs for issuing debt securities or preferred shares are generally lower than those for issuing common shares. The flotation costs for the issuance of common shares typically ranges from 2% to 8%.

The concept of flotation costs is strongly related to the concept of cost of capital. Since flotation expenses affect the amount of capital that can be raised by issuing new securities, the costs must somehow impact a company’s cost of capital. There are two main views regarding the matter:

The first approach states that the flotation expenses must be incorporated into the calculation of a company’s cost of capital. Essentially, it states that flotation costs increase a company’s cost of capital. Recall that the cost of capital of a company consists of the cost of debt and cost of equity. Thus, expenses affect the cost of capital by changing either cost of debt or cost of equity, depending on a type of securities issued (e.g., issuance of common stock affects the cost of equity).

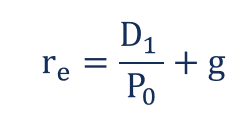

For example, let’s assume that a company issues new common shares. Before the transaction, a company’s cost of equity can be calculated using the following formula:

Where:

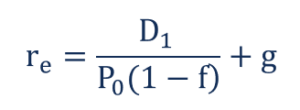

However, the issuance of new shares causes a company to incur flotation expenses. Thus, the current share price (denoted as ) must be adjusted for the effect of such costs.

As a result, the cost of equity formula adjusted for the flotation costs will look:

Where:

Nevertheless, the abovementioned approach is not accurate because the incorporation of flotation expenses does not depict the actual picture. In such a scenario, the cost of capital is overstated by the percentage of flotation expenses incurred. The costs of flotation are non-recurring expenses that are incurred by a company only once when new securities are issued.

Alternatively, the second approach is to adjust the company’s cash flows for the flotation expenses. Unlike the first method, the adjustment approach does not modify the actual cost of capital. Instead, a company deducts the costs from the cash flows that are used in the calculation of net present value (NPV).

The cash flow adjustment method was initially suggested by John R. Ezzell and R. Burr Porter in the article “Flotation Costs and Weighted Average Cost of Capital.” The main idea behind the method is that the costs are only one-time expenses paid to third parties.

The approach of deducting the flotation expenses from the company’s cash flows is more appropriate than the direct incorporation of the costs into a cost of capital because it considers the one-time nature of the expenses. Simultaneously, a company’s cost of capital remains unaffected by the flotation expenses, and it is not overstated.

Thank you for reading CFI’s guide to Flotation Costs. To keep advancing your career, the additional CFI resources below will be useful: