Get Certified for Financial Modeling (FMVA)®

Gain in-demand industry knowledge and hands-on practice that will help you stand out from the competition and become a world-class financial analyst.

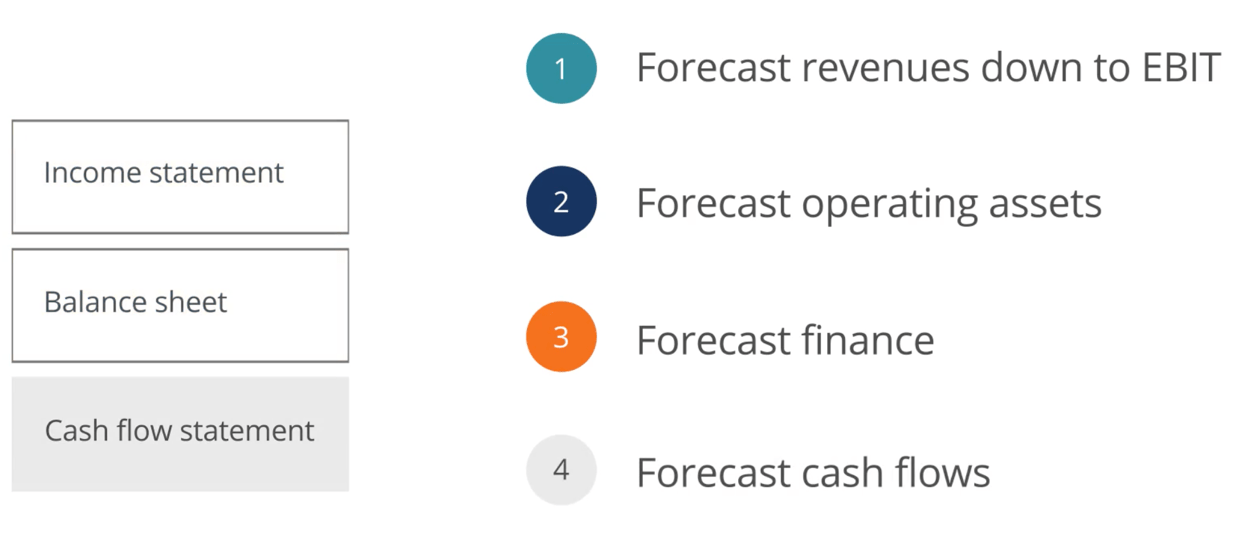

Part four of the four-step financial forecasting model in Excel

This article on forecasting cash flow is the last part of the four-step financial forecasting model in Excel. Having completed our income statement and balance sheet forecasts, we can now turn to the cash flow statement to complete the four-step forecast modeling framework.

By the end of this article, you will be able to:

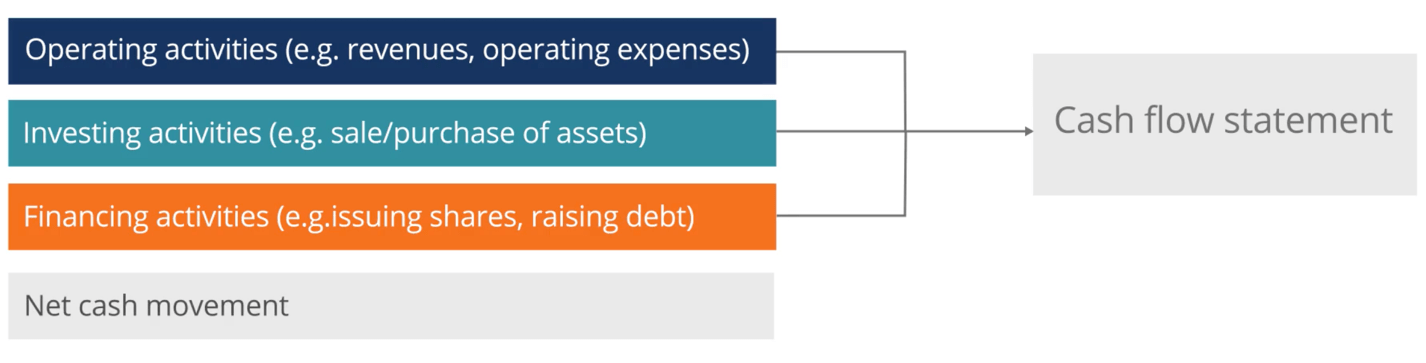

A cash flow forecast can be derived from the balance sheet and income statement. We begin by forecasting cash flows from operating activities before moving on to forecasting cash flows from investing and financing activities.

Operating activities include revenues and operating expenses, while investing activities include the sale or purchase of assets and financing activities with the issuance of shares and raising debt. From forecasting all three activities, we will arrive at the forecast net cash movement.

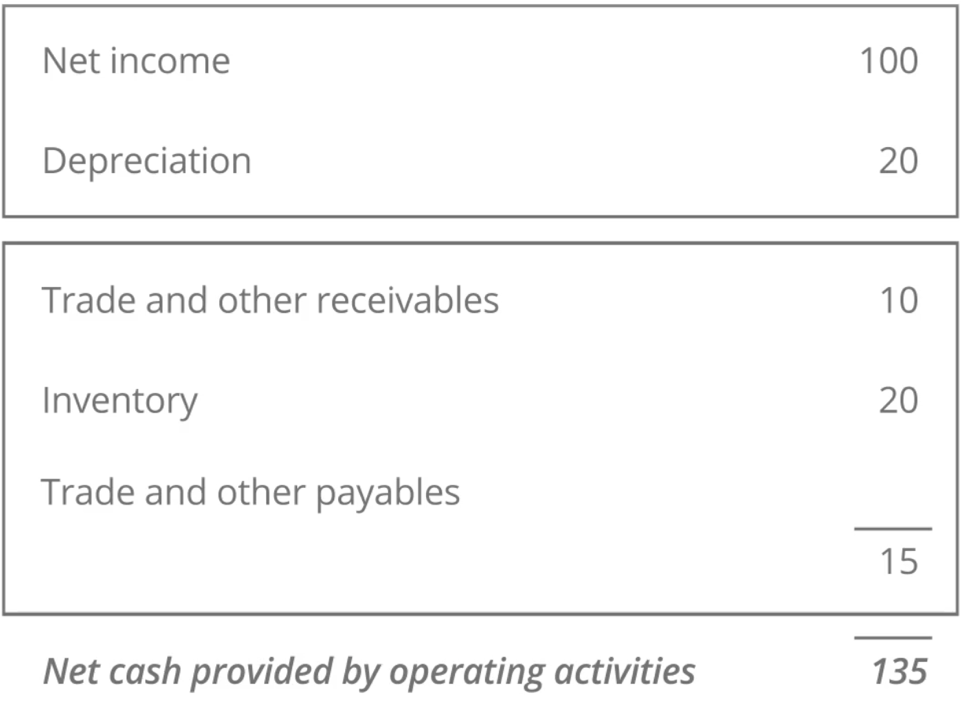

The first step in our cash flow forecast is to forecast cash flows from operating activities, which can be derived from the balance sheet and the income statement.

From the income statement, we use forecast net income and add back the forecast depreciation. We then use the forecast balance sheet to calculate changes in operating assets and liabilities. For each operating asset and liability, we must compare our forecast year in question with the prior year.

In this example, changes in receivables and inventory have the effect of increasing the total cash flows. In other words, receivables and inventory in our forecast year are both lower than in the prior year.

Changes in trade and other payables have a reverse effect – decreasing total cash flows from operating activities. In other words, the payables figure must be lower in our forecast year than in the prior year.

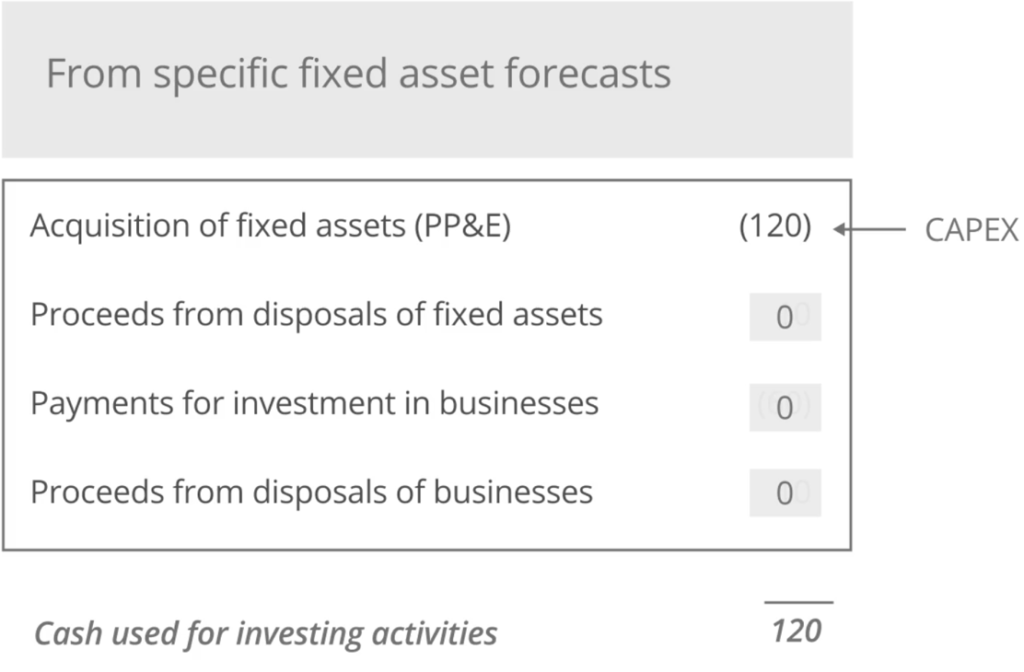

Now that we have learned how to calculate cash flows from operating activities, let’s look at investing activities. All investing activity items come from specific fixed assets or property plant & equipment (PP&E) forecasts.

Our model forecasts fixed assets in detail in the “Supporting Schedules” section, where we assume:

As a result, the only item we will forecast in our model will relate to the acquisition of fixed assets or property, plant & equipment (PP&E). It is often referred to as CAPEX, short for capital expenditures.

After forecasting investing activities, we will now learn how to calculate cash flows from financing activities. Most financing activity items are calculated by simply comparing the forecast year with the prior year. In our model, we included dividends in our financing activity. In practice, some organizations include dividend cash flows in operating activities. The choice should reflect how dividends are reported in financial statements.

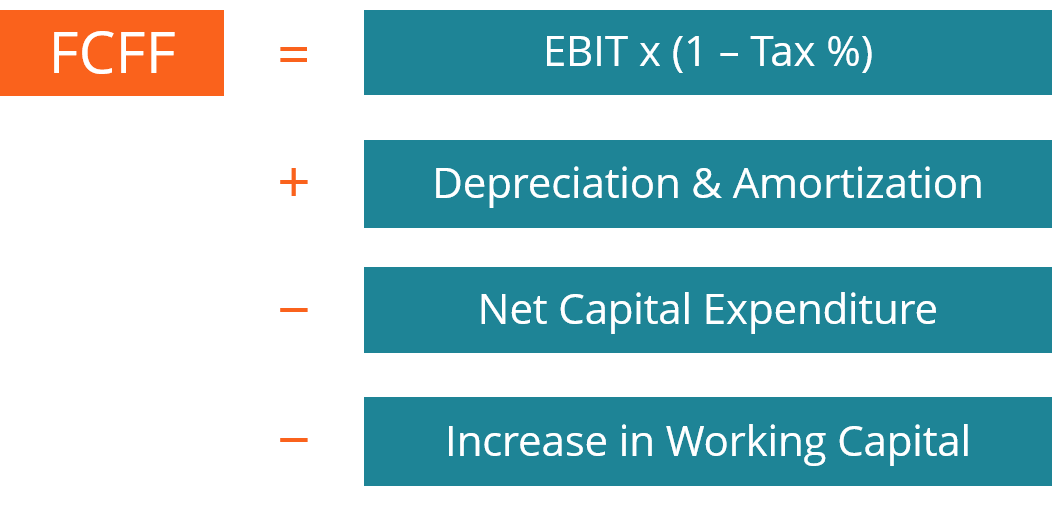

Free cash flow to the firm (aka Unlevered Free Cash Flow) forecast is the preferred approach when valuing equities using discounted cash flows. Free cash flows to the firm can be defined by the following formula:

FCF to the firm is Earnings Before Interests and Taxes (EBIT), times one minus the tax rate, where the tax rate is expressed as a percent or decimal. Since depreciation and amortization are non-cash expenses, they are added back. Net capital expenditures and increases in net working capital are then deducted. Note that decreases in working capital will be added to the equation.

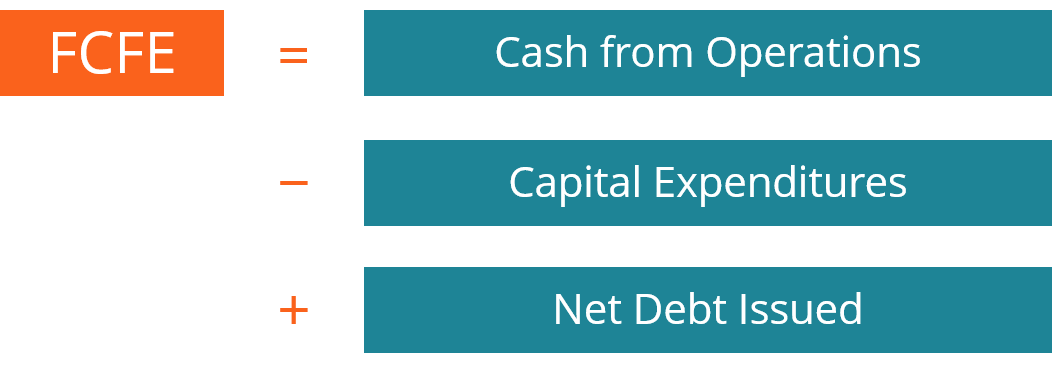

Although FCF to the firm is the preferred approach to equity valuation, it is not the only FCF calculation used. There is another FCF variant that is used called FCF to equity.

Free cash flows to equity are used to determine how much cash is available to equity investors after paying off debt interest and satisfying sustainable obligations. In simple terms, FCF to equity is cash flow from operations, minus capital expenditures, plus net debt issued.

Since there are only two major differences between FCF to the firm and FCF to equity, it is relatively easy to reconcile the two.

Starting with FCF to equity, we simply deduct the net debt issued, add back the interest expense, and deduct the tax shield on interest. The tax shield on interest is the difference between taxes calculated on EBIT and taxes calculated on earnings before tax.

Connect what you just learned to a clear career path with CFI’s role‑based courses and certification programs.

Thank you for reading CFI’s guide to Forecasting Cash Flow. To keep learning and developing your knowledge of financial analysis, we highly recommend the additional CFI resources below: