Agency Bonds

Debt issued by a government-sponsored enterprise (GSE) or a federal agency

What are Agency Bonds?

Agency bonds, also known as agency debt, is the debt issued by a government-sponsored enterprise (GSE) or a federal agency.

The key difference between a GSE and a federal agency is that a GSE’s obligations are not guaranteed by the government, whereas a federal agency’s debt is backed up by a government guarantee.

For example, the Federal National Mortgage Association (FNMA), also known as Fannie Mae, is a GSE. The Government National Mortgage Association (GNMA), also called Ginnie Mae, is a federal agency.

Mechanics of Agency Debt Market

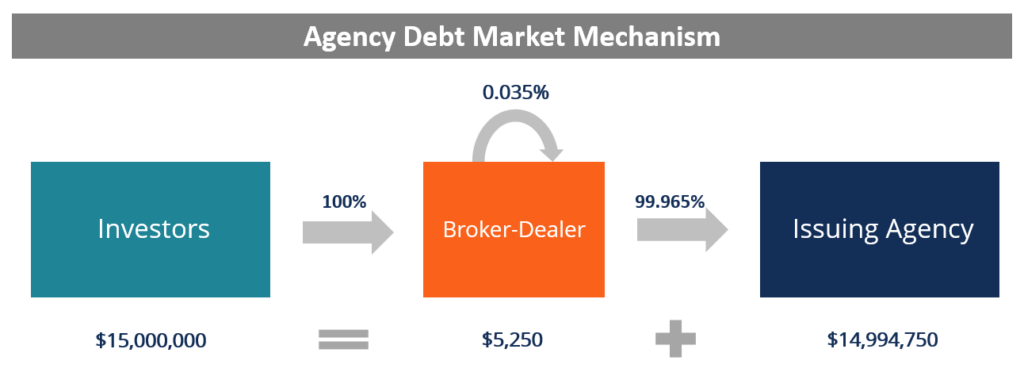

Agency bond is typically issued through broker-dealers. Some well-known broker-dealers, such as J.P. Morgan, Nomura, and BNY Mellon, participate in the market by underwriting agency debt. They buy agency debt wholesale at a discount, then sell the debt to investors in the secondary market at a higher price.

Characteristics of Agency Bonds

Below are the important characteristics of agency bonds:

- Low risk: Agency bonds are considered very safe and typically come with high credit ratings.

- Higher return: They provide higher returns relative to treasuries, which are considered risk-free.

- Highly liquid: They are actively traded and hence, are highly liquid.

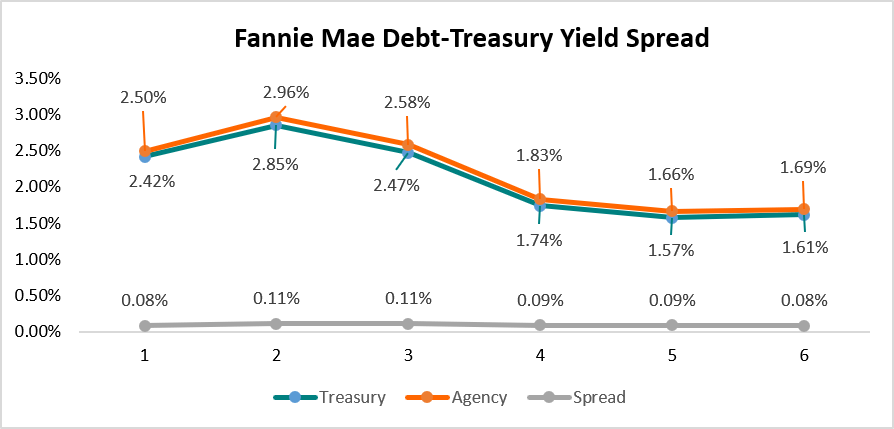

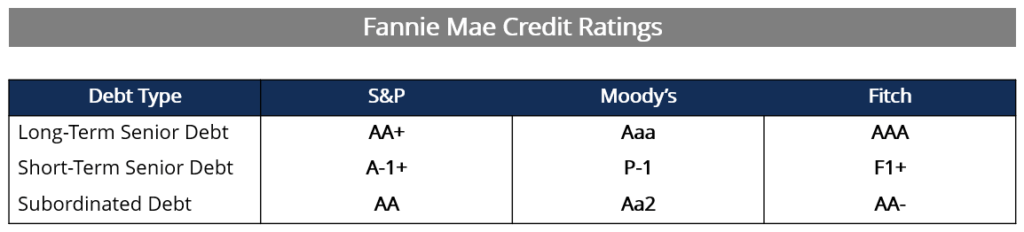

The following figures show the credit ratings and excess returns relative to treasuries for Fannie Mae debt:

Types of Agency Bonds

Agency bond is offered across many maturities, ranging from less than a year to 30-year bonds. Some common bond structures that include agency debt are listed below:

- Short-term notes

- Medium-term notes

- Callable bonds

- Fixed coupon bonds

Two additional bond structures that can be found in the agency market, include floaters, which come with a variable coupon payment, and zero-coupon discount bonds (sometimes called “discos”).

Real-World Example

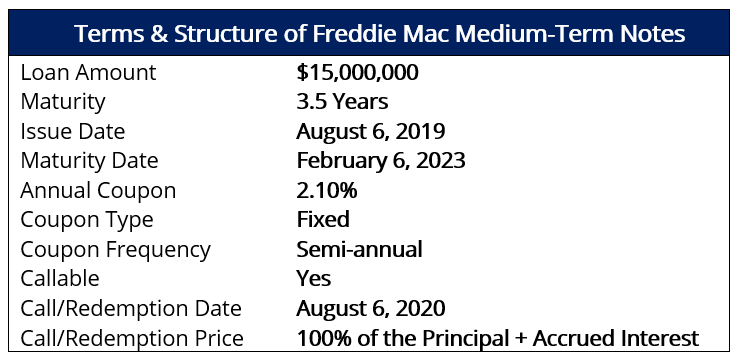

Let us look at a real-world example of agency debt issued by another well-known GSE, the Federal Home Loan Mortgage Corporation (FHLMC), also known as Freddie Mac. The example below illustrates some of the aforementioned concepts:

There’s a lot of information in the table above. Let us discuss it step-by-step.

Loan Amount and Maturity

It is clear from the table that Freddie Mac raised $15 million on August 6, 2019, and the loan is due 3.5 years later on February 6, 2023.

Coupon

The bond pays a fixed annual coupon of 2.10%. The payments are made semi-annually (i.e., every six months), as shown by the coupon frequency.

Call Provision or Redemption

The bond is callable, which means the issuer owns the option to buy it back at a pre-specified time (the redemption date) at the redemption price.

In the example, the redemption date is August 6, 2020. The issuer cannot call or redeem the bond on any date other than the pre-specified date.

The redemption price is 100% of the principal payment plus accrued interest, which, in this case, means that the bondholders will get the $15 million principal plus the portion of the coupon payable by the redemption date.

Investing in Agency Debt

Just like any investment vehicle, agency debt comes with its advantages and disadvantages. In addition, tax considerations must be taken into account.

Advantages

Low risk and higher returns:

- Agency debt is considered to come with low default risk even when it is not backed up by the government.

- It provides higher returns relative to treasuries, which are considered default-free.

High liquidity:

- Agency debt is actively traded and can be bought or sold without a high transaction cost.

Disadvantages

Inflation risk and costs:

- Returns from holding agency debt are reduced in a high inflation environment or if the transaction costs are too high.

Interest rate risk:

- Just like any debt security, agency debt will likely fluctuate in price due to interest rate changes.

Complexity:

- Agency debt is offered in a variety of structures, with some being more complex than others.

- It is difficult to analyze different structures and decide if agency debt is suitable for one’s portfolio.

Tax Considerations

It is important to differentiate between GSE and federal agency debt for tax purposes as well. Interest earned on GSE debt is not tax-exempt, while interest on federal agency debt is tax-exempt. It is an important detail as tax may exert a significant effect on a company’s investments.

More Resources

CFI is the official provider of the Commercial Banking & Credit Analyst (CBCA)™ certification program, designed to transform anyone into a world-class financial analyst.

In order to help you become a world-class financial analyst and advance your career to your fullest potential, these additional resources will be very helpful: