Get Certified for Financial Modeling (FMVA)®

Gain in-demand industry knowledge and hands-on practice that will help you stand out from the competition and become a world-class financial analyst.

The basis of accounting

The accounting equation is a basic principle of accounting and a fundamental element of the balance sheet. The equation is as follows:

Assets = Liabilities + Shareholder’s Equity

This equation sets the foundation of double-entry accounting, also known as double-entry bookkeeping, and highlights the structure of the balance sheet. Double-entry accounting is a system where every transaction affects at least two accounts.

For example, an increase in an asset account can be matched by an equal increase to a related liability or shareholder’s equity account such that the accounting equation stays in balance. Alternatively, an increase in an asset account can be matched by an equal decrease in another asset account. It is important to keep the accounting equation in mind when performing journal entries.

Journal entries often use the language of debits (DR) and credits (CR). A debit refers to an increase in an asset or a decrease in a liability or shareholders’ equity. A credit in contrast refers to a decrease in an asset or an increase in a liability or shareholders’ equity.

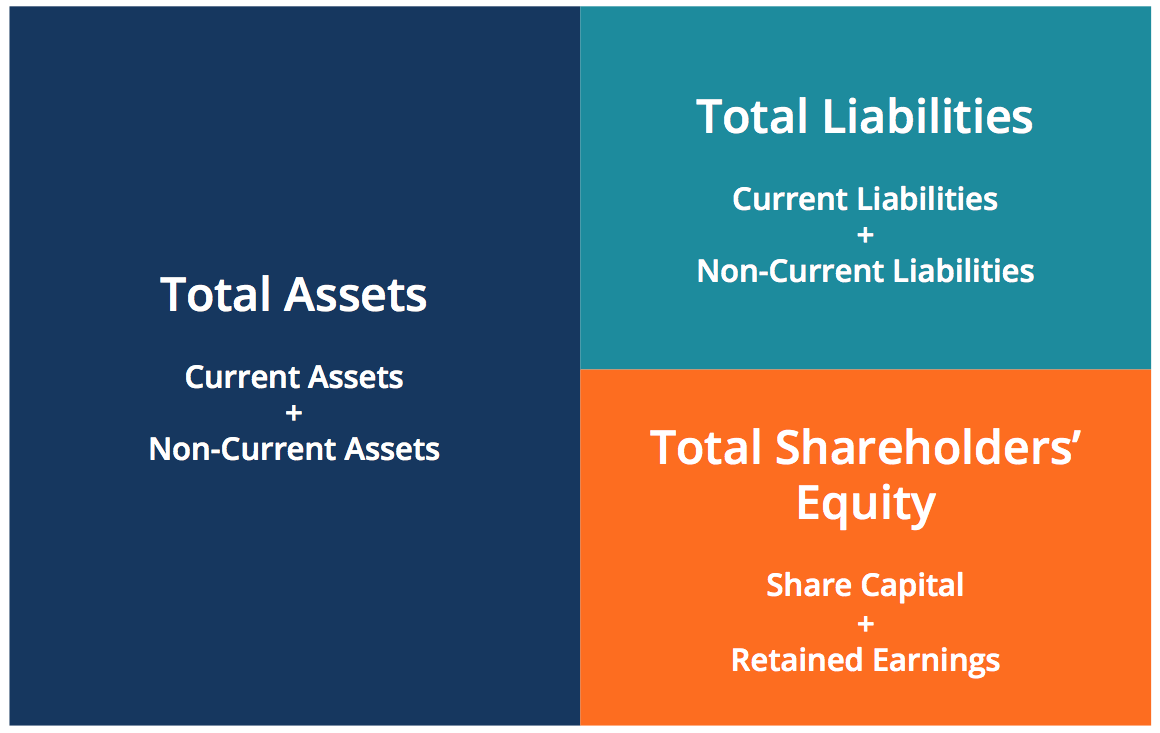

As mentioned above, the accounting equation forms the basis for the balance sheet. The balance sheet is also sometimes referred to as the statement of financial position. The balance sheet is broken down into three major sections and their various underlying items: Assets, Liabilities, and Shareholder’s Equity.

You can learn how to read a balance sheet and other financial statements in much great detail with CFI’s free reading financial statements course!

Below are some examples of items that fall under each section:

Shareholder’s Equity: Share Capital, Retained Earnings

The accounting equation shows the relationship between these items.

The accounting equation can also be rearranged into the following form:

Shareholder’s Equity = Assets – Liabilities

In this form, it is easier to highlight the relationship between shareholder’s equity and debt (liabilities). As you can see, shareholder’s equity is the remainder after liabilities have been subtracted from assets. This is because creditors – parties that lend money such as banks – have the first claim to a company’s assets.

For example, if a company becomes bankrupt, its assets are sold and these funds are used to settle its debts first. Only after debts are settled are shareholders entitled to any of the company’s assets to attempt to recover their investment.

Regardless of how the accounting equation is represented, it is important to remember that the equation must always balance.

For every transaction, both sides of this equation must have an equal net effect. Below are some examples of transactions and how they affect the accounting equation.

CFI’s free accounting fundamentals course will help you better understand these examples!

Company XYZ wishes to purchase a $500 machine using only cash. This transaction would result in a debit (an increase in an asset) to Equipment (+$500) and a credit (a decrease in an asset) to Cash (-$500). The net effect on the accounting equation would be as follows:

This transaction affects only the assets of the equation; therefore there is no corresponding effect in liabilities or shareholder’s equity on the right side of the equation.

Company XYZ wishes to purchase a $500 machine but it only has $250 of cash in its holdings. The company is allowed to purchase this machine with an initial payment of $250 but it owes the manufacturer the remaining amount. It would result in a debit (an increase in an asset) to Equipment (+$500), a credit (an increase in a liability) to Accounts Payable (+$250), and a credit (a decrease in an asset) to Cash (-$250). The net effect on the accounting equation would be as follows:

This transaction affects both sides of the accounting equation; both the left and right sides of the equation increase by +$250.

Connect what you just learned to a clear career path with CFI’s role‑based courses and certification programs.

Thank you for reading CFI’s guide on Accounting Equation. To keep learning and advancing your career, the following resources will be helpful: