Get Certified for Financial Modeling (FMVA)®

Gain in-demand industry knowledge and hands-on practice that will help you stand out from the competition and become a world-class financial analyst.

Accounting for debt securities that companies hold to maturity

Held to maturity securities are securities that companies purchase and intend to hold until they mature. They are unlike trading securities or available for sale securities, where companies don’t usually hold on to securities until they reach maturity.

Companies mostly use held to maturity securities to protect themselves against interest rate fluctuations, diversify their investment portfolios, and realize a small, low-risk capital gain over a longer period of time. The investments usually comprise debt instruments, such as government bonds or corporate bonds.

The biggest difference between held to maturity securities and the other security types mentioned above is their accounting treatment. As opposed to being recorded and updated on the company’s balance sheet according to the security’s fair market value, held to maturity securities are recorded at their original purchase cost. It means that from one accounting period to another, the value of the securities on the company’s balance sheet will remain constant.

Any gains or losses resulting from changes in interest rates (for bonds and other debt instruments) will be recorded when the securities reach maturity. Below is an example of how a 2-year bond will appear on a company’s balance sheet:

Upon purchase, the offsetting account will likely be cash, as the company likely bought the securities with cash. Here, we can see that no changes are recorded in the 2017 accounting period, despite any changes in the security’s fair value during that time period. For example, if interest rates fell sharply in 2016, which would cause a rise in the bond’s market value, there was no accounting of the change in the company’s balance sheet.

In 2018, the company saw a net addition of $500 million in held to maturity securities, which was likely a purchase of additional securities.

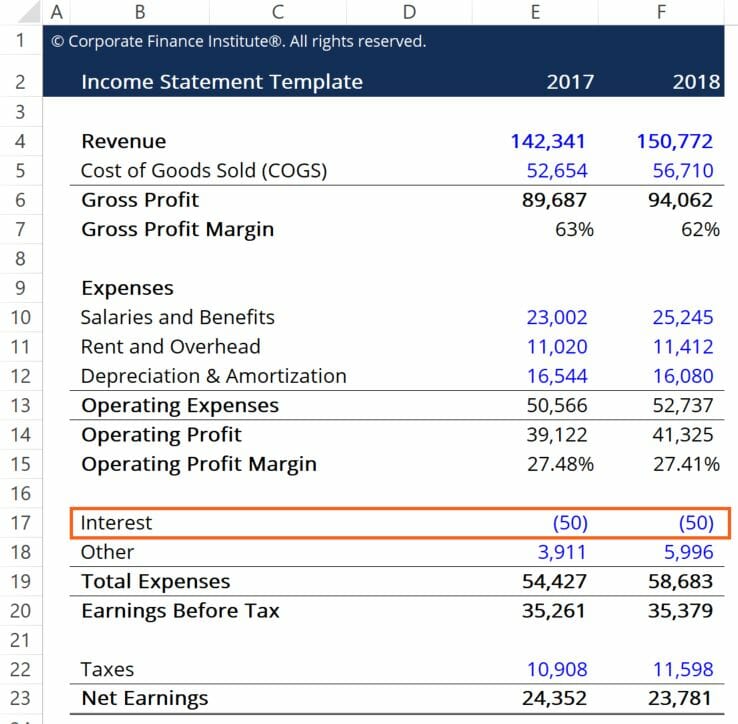

Interest payments made to the debt-holding company will appear in the company’s income statement on a periodic basis. Let’s assume that the bonds pay a 10% annual coupon rate, which equates to $50 million in additional income each year. Here’s how this would look on a company’s income statement:

Here, we can see how the 10% coupon is captured in the interest line item. For simplicity, it is assumed that the company does not have any other interest revenues. The interest income from coupon payments is recorded as a credit or negative expense in the Total Expenses grouping of the Income Statement.

CFI offers the Financial Modeling & Valuation Analyst (FMVA)® certification program for those looking to take their careers to the next level. To learn more about related topics, check out the following CFI resources: