Get Certified for Financial Modeling (FMVA)®

Gain in-demand industry knowledge and hands-on practice that will help you stand out from the competition and become a world-class financial analyst.

Direct costs associated with the manufacturing of products for revenue generation

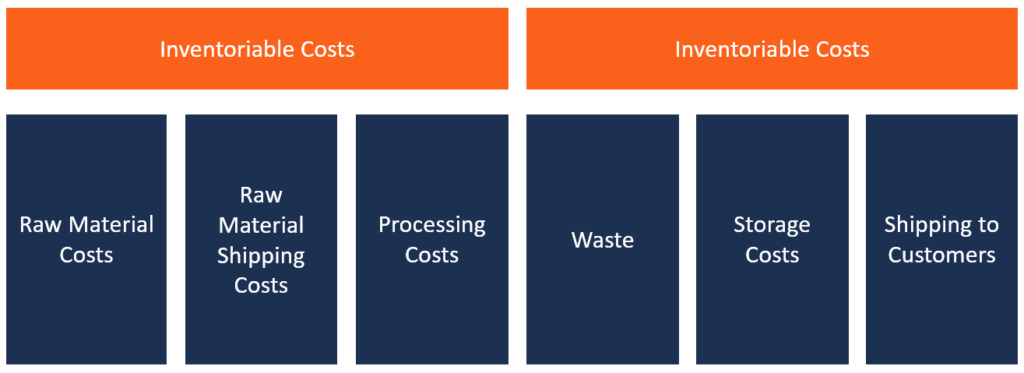

Inventoriable costs, also known as product costs, refer to the direct costs associated with the manufacturing of products and in getting them ready for sale. Often, inventoriable costs include direct labor, direct materials, factory overhead, and freight-in.

Once a product is sold to a customer or disposed of in another way, the cost of the product is charged to the expense account. Before the inventory is sold, it is recorded on the balance sheet as an asset. The sale of these products moves inventory from the balance sheet to the cost of goods sold (COGS) expense line in the income statement.

Inventoriable costs vary from one industry to another, and they may also differ from one supplier to another down the supply chain. Therefore, what one manufacturer considers as inventoriable costs may be different from what a retailer treats as inventoriable costs. For instance, for a retailer, inventoriable costs include all costs related to the acquisition of the product from the manufacturer all the way to its premises.

However, for a manufacturer, their inventoriable costs are direct material, direct labor, and all manufacturing overheads.

When managers want to determine the production cost per unit, they narrow down all the costs related to the production of a given batch of products. They sum all the costs of producing a batch and divide the value obtained by the total units produced, as shown in the formula below:

Product unit cost = (Total direct labor + Total direct material + Consumable supplies + Freight-in + Total allocated overhead)/Total number of units

Once the managers determine the production unit cost, they may use that information to develop a pricing model. The pricing model enables them to identify the number of units that they need to produce and sell to break even. This is important because, for a product line to be profitable, they need to determine a unit price that covers the cost per unit and produces a reasonable profit margin that will cover any fixed costs.

Failure to break even means that the production results in a loss and the manufacturer needs to respond by increasing their sales price, cutting the number of units produced, or closing the entire product line.

Accountants use the inventory account to record inventoriable costs. However, when the manufacturer sells the goods, the costs are transferred to an expense account (COGS). It allows accountants to monitor the revenues against the COGS in the income statement, which eventually end up in the company’s financial statements as net profits.

Example: Inventoriable Costs

Let’s say Company X assembles laptops for resale in Ontario, California. The company imports different computer parts from various parts of the world and different manufacturers. For example, the displays may be from CoolTouch Monitors, motherboards and casings from China, hard disks from Seagate, processors and RAM from Intel, with the rest of the components made in-house.

To aggregate the inventoriable costs of manufacturing, the manufacturer must account for all costs incurred from the point of acquisition up to the point when the goods are brought to their warehouse. This includes all costs incurred before and during assembly, such as the cost of acquiring each part, direct labor, freight-in, and any other manufacturing overheads.

Therefore, if producing 1,000 pieces of laptops costs the manufacturer $250,000, the production unit cost will be $250 ($250,000/1,000 units). To break even and make profits, a single unit/laptop must be sold for a price that is higher than $250. Initially, the company will record these costs in the inventory assets accounts. Once the product is sold to retailers, it is recorded as COGS on the income statement.

The cost of business is divided into two categories, based on whether the expense is capitalized to the cost of the goods sold. The two categories are inventoriable costs and period costs.

Inventoriable costs are the costs incurred in the manufacturing or acquisition of a product. These costs are initially recorded in the balance sheet as current assets and do not appear in the income statement until the first unit is sold. Once the products are sold, they are charged to the expense account, and this allows businesses to match the revenue from a product with its cost of goods sold. Examples of product costs are direct materials, direct labor, and factory overheads.

On the other hand, period costs are associated with the passage of time and are not included in the inventoriable costs. If a business does not have production or inventory purchasing activities, the business will not incur inventoriable costs, but will still incur period costs.

Period costs are associated with the selling activities of the business, and they are treated as expenses in the actual year when they occur. The US GAAP requires that all selling and administrative expenses be treated as period costs. Examples of period costs include marketing costs, office rent, and indirect labor.

Direct materials – Refers to all raw materials and sub-assemblies built into the final product.

Direct labor – Refers to the costs of employees engaged directly in the assembly and production of a product that is assigned either to a specific product, cost center, or work order. For instance, machine operators in a production line, employees at the assembly lines, or even technical officers operating and monitoring production operations.

Freight-in – Refers to the costs associated with the transportation of production inputs. It is charged when goods are delivered from the supplier to the manufacturer.

Manufacturing overheads – Refers to the manufacturing costs other than variable costs that a manufacturer incurs during a given period of production. They are fixed costs that are directly related to the manufacturing of a product. They include all costs related to direct material, and direct labor. For example, the cost of electricity required to operate manufacturing machinery is a manufacturing overhead cost.

CFI is the official provider of the Financial Modeling and Valuation Analyst (FMVA)® certification program, designed to transform anyone into a world-class financial analyst.

To keep learning and developing your knowledge of financial analysis, we highly recommend the additional CFI resources below:

CFI is a global provider of financial modeling courses and of the FMVA Certification. CFI’s mission is to help all professionals improve their technical skills. If you are a student or looking for a career change, the CFI website has many free resources to help you jumpstart your Career in Finance. If you are seeking to improve your technical skills, check out some of our most popular courses. Below are some additional resources for you to further explore:

CFI is a global provider of financial modeling courses and of the FMVA Certification. CFI’s mission is to help all professionals improve their technical skills. If you are a student or looking for a career change, the CFI website has many free resources to help you jumpstart your Career in Finance. If you are seeking to improve your technical skills, check out some of our most popular courses. Below are some additional resources for you to further explore:

Below is a break down of subject weightings in the FMVA® financial analyst program. As you can see there is a heavy focus on financial modeling, finance, Excel, business valuation, budgeting/forecasting, PowerPoint presentations, accounting and business strategy.

A well rounded financial analyst possesses all of the above skills!

CFI is the global institution behind the financial modeling and valuation analyst FMVA® Designation. CFI is on a mission to enable anyone to be a great financial analyst and have a great career path. In order to help you advance your career, CFI has compiled many resources to assist you along the path.

In order to become a great financial analyst, here are some more questions and answers for you to discover: