Net Income After Tax (NIAT)

An entity’s profits after deducting all expenses and taxes in a fiscal period

What is Net Income After Tax (NIAT)?

Net income after tax (NIAT) is an entity’s profits after deducting all expenses and taxes in a fiscal period. NIAT is also commonly referred to as a company’s bottom-line profitability.

Summary

- Net income after tax (NIAT) is an entity’s profits after deducting all expenses and taxes. It is also referred to as bottom-line profitability.

- NIAT is frequently used in ratio analysis to identify the company’s profitability.

- Net income after tax is either reinvested back into the company, paid out in dividends, or is used to acquire treasury stock.

How to Calculate Net Income After Tax?

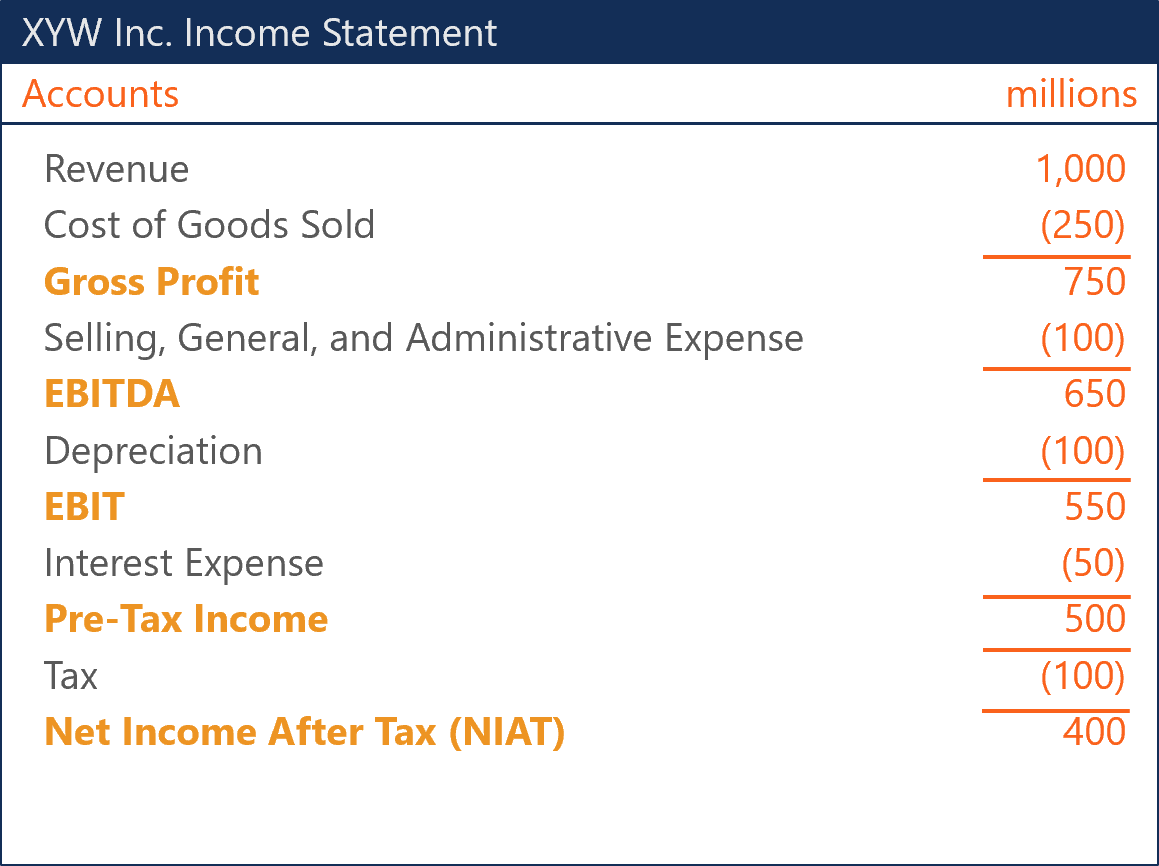

Calculating net income after tax involves deducting all expenses and costs from revenues in a given fiscal period. The expenses and costs are the following:

Cost of Goods Sold (COGS)

The cost of goods sold (COGS) is the carrying value of goods sold in a given period. Recording the cost of goods sold is dependent on the applied inventory valuation method. Generally accepted accounting principles (GAAP) dictate that inventory can be valued via the specific identification method, average cost basis, or first-in-first-out method.

Selling, General, and Administrative (SG&A) Expense

SG&A expense consists of the direct costs, indirect costs, and overhead costs that are instrumental for the company’s day-to-day operations. For example, commissions, salaries, insurance, and supplies are also examples of selling, general, and administrative expenses. Alternatively, the SG&A account is also referred to as operating expenses.

Depreciation

The acquisition of tangible assets like PP&E deteriorates with use and eventually wears out. Accountants try to best allocate this deterioration cost across the asset’s useful life in order to faithfully represent the asset’s value.

Interest Expense

Interest expense refers to the cost of borrowing for the debtor. It is accrued and expensed over time. Each debt payment is made up of principal repayment and interest expense.

Net Income After Tax in Ratio Analysis

Net income after tax is often used in relation to other account balances to interpret the company’s ability to generate profit. There are primarily two ways net income after tax is used in an analysis to interpret a company’s profitability.

Firstly, through the calculation of return ratios, analysts can quantify a company’s ability to generate profit given asset investments and equity financing. Secondly, profitability can be assessed relative to revenues generated.

Return on Assets

Return on assets (ROA) shows the ratio of net income after tax relative to the company’s total asset balance over a given period. The application of ROA expresses how much after-tax profit a company earns for every dollar of assets it holds. The lower the after-tax profit is relative to the total asset balance, the more intensive the assets are.

Return on Equity

Return on equity (ROE) expresses net income after tax as a ratio of shareholder’s equity over a given period. ROE is simply the rate of return the company generates with its equity capital raising. It is frequently used in profitability analysis to indicate a company’s ability to generate profits without utilizing debt.

Net Profit Margin

Net profit margin refers to a company’s bottom-line profitability. It is the ratio of net income after tax over total sales over a given period. A net profit margin indicates what percentage of revenues are profit, and therefore, demonstrates how efficient a company is in converting sales to after-tax profits.

What is Net Income After Tax Used For?

There are three primary ways net income after tax is used:

1. Reinvestment

Companies can choose to reinvest net income after tax back into the company. It often signifies to investors of a company’s strong growth prospects. Specifically, investors believe that the company is holding positive net present value projects in its pipeline and can generate further returns on their investment.

2. Dividends

Dividends can be a very attractive characteristic of equity ownership for investors who value cash flows rather than growth prospects. Furthermore, a company that pays consistent dividends is generally very stable. However, some investors see dividend payouts to symbolize that the company lacks positive net present value projects in its pipeline.

3. Share Repurchase

Repurchasing stock is known as negative share issuance, and the shares are held in the company’s treasury. An increase in treasury stock indicates a reduction in the number of shares outstanding.

There are two primary reasons why a company would purchase its own shares on the secondary market. Firstly, the company could be trying to fend off other companies from taking a controlling equity stake. Secondly, the company may believe the shares are trading at a discount and that buying them will create more shareholder value than investing in internal projects.

Additional Resources

CFI is the official provider of the global Commercial Banking & Credit Analyst (CBCA)™ certification program, designed to help anyone become a world-class financial analyst. To keep advancing your career, the additional resources below will be useful:

Analyst Certification FMVA® Program

Below is a break down of subject weightings in the FMVA® financial analyst program. As you can see there is a heavy focus on financial modeling, finance, Excel, business valuation, budgeting/forecasting, PowerPoint presentations, accounting and business strategy.

A well rounded financial analyst possesses all of the above skills!

Additional Questions & Answers

CFI is the global institution behind the financial modeling and valuation analyst FMVA® Designation. CFI is on a mission to enable anyone to be a great financial analyst and have a great career path. In order to help you advance your career, CFI has compiled many resources to assist you along the path.

In order to become a great financial analyst, here are some more questions and answers for you to discover:

- What is Financial Modeling?

- How Do You Build a DCF Model?

- What is Sensitivity Analysis?

- How Do You Value a Business?

Accounting Crash Courses

Learn accounting fundamentals and how to read financial statements with CFI’s online accounting classes.

These courses will give you the confidence to perform world-class financial analyst work. Start now!

Boost your confidence and master accounting skills effortlessly with CFI’s expert-led courses! Choose CFI for unparalleled industry expertise and hands-on learning that prepares you for real-world success.