Get Certified for Financial Modeling (FMVA)®

Gain in-demand industry knowledge and hands-on practice that will help you stand out from the competition and become a world-class financial analyst.

An accounting principle that outlines the specific conditions in which revenue is recognized

Revenue recognition is an accounting principle that outlines the specific conditions under which revenue is recognized. In theory, there is a wide range of potential points at which revenue can be recognized. The following guide addresses recognition principles for both IFRS and U.S. GAAP.

According to the IFRS criteria, for revenue to be recognized, the following conditions must be satisfied:

Conditions (1) and (2) are referred to as Performance. Regarding performance, it occurs when the seller has done what is expected to be entitled to payment.

Condition (3) is referred to as Collectability. The seller must have a reasonable expectation that he or she will be paid for the performance.

Conditions (4) and (5) are referred to as Measurability. Due to the accounting guideline of the matching principle, the seller must be able to match the revenues to the expenses. Hence, both revenues and expenses should be able to be reasonably measured.

IFRS 15, Revenue from Contracts with Customers, establishes the specific steps for revenue recognition. It is important to note that there are some exclusions from IFRS 15 such as:

The five steps for revenue recognition in contracts are as follows:

All conditions must be satisfied for a contract to form:

Some contracts may involve more than one performance obligation. For example, the sale of a car with a complementary driving lesson would be considered as two performance obligations – the first being the car itself and the second being the driving lesson.

Performance obligations must be distinct from each other. The following conditions must be satisfied for a good or service to be distinct:

The transaction price is usually readily determined; most contracts involve a fixed amount. For example, a price of $20,000 for the sale of a car with a complementary driving lesson. The transaction price, in this case, would be $20,000.

The allocation of the transaction price to more than one performance obligation should be based on the standalone selling prices of the performance obligations.

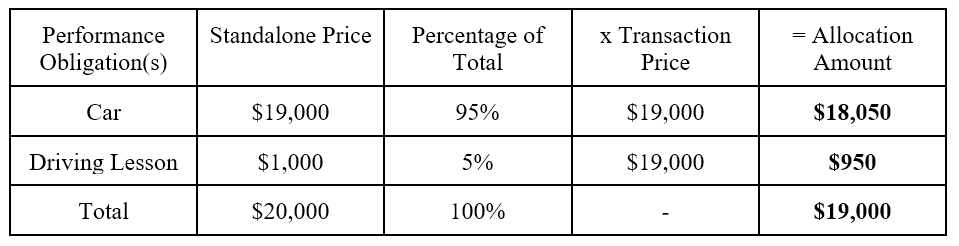

For example, a contract involves the sale of a car with a complementary driving lesson. The total transaction price is $20,000. The standalone selling price of the car is $19,000 while the standalone selling price of the driving lesson is $1,000. The transaction price allocation would be as follows:

Note: The percentage of the total is simply the standalone price divided by the total standalone price. For example, the percentage of total for the car would be calculated as $19,000 / $20,000 = 95%.

Recall the conditions for revenue recognition. Conditions (1) and (2) state that revenue would be recognized when the seller has done what is expected to be entitled to payment. Therefore, revenue is recognized as either:

In the example above, the revenue associated with the car would be recognized at the time the buyer takes possession. On the other hand, the complementary driving lesson would be recognized upon service provision.

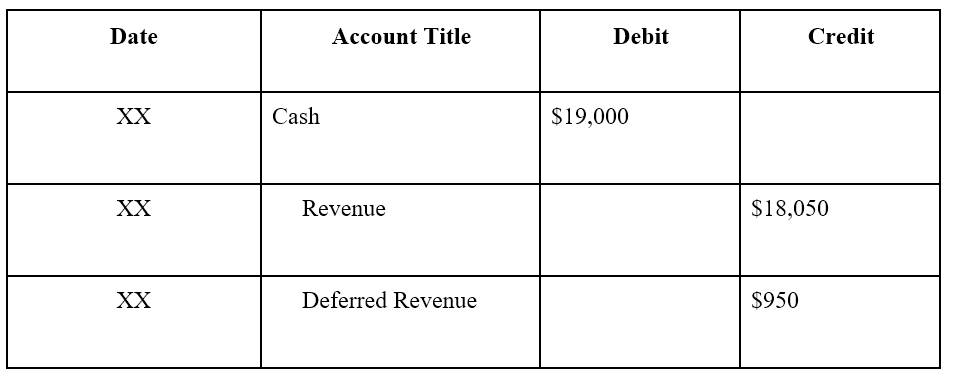

The revenue recognition journal entries for the two performance obligations (car and driving lesson) would be as follows:

For the sale of the car and a complimentary driving lesson:

Note: Revenue is recognized for the sale of the car ($18,050) but not for the complementary driving lesson because it has not yet been provided.

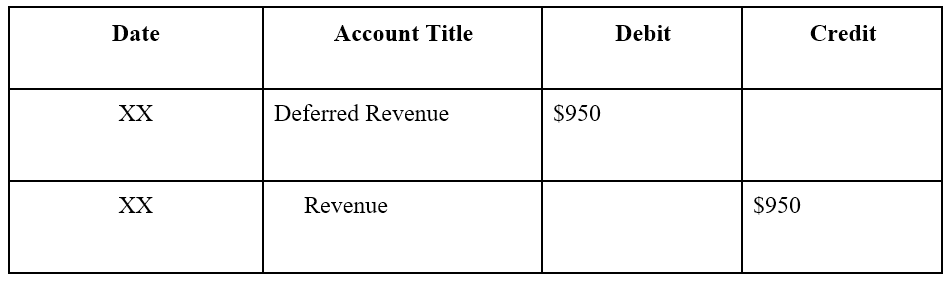

When the complementary driving lesson has been provided:

Note: Revenue is deferred until the driving lesson has been provided.

The Financial Accounting Standards Board (FASB), which sets the standards for U.S. GAAP, mandates the following five principles for recognizing revenue:

Learn more about the principles on FASB’s website.

Connect what you just learned to a clear career path with CFI’s role‑based courses and certification programs.

Thank you for reading CFI’s guide to Revenue Recognition. To keep advancing your career, the additional CFI resources below will be useful: