Get Certified for

Commercial Banking (CBCA®)

Stand out and gain a competitive edge as a commercial banker, loan officer, or credit analyst with advanced knowledge, real-world analysis skills, and career confidence.

A period during which the borrower is not obligated to make payments

A moratorium period is a period during which the borrower is not obligated to make payments. In other words, during a moratorium period, the borrower is permitted to halt their payments. It is commonly incorporated in home loans – called an equated monthly installments holiday – and educational loans.

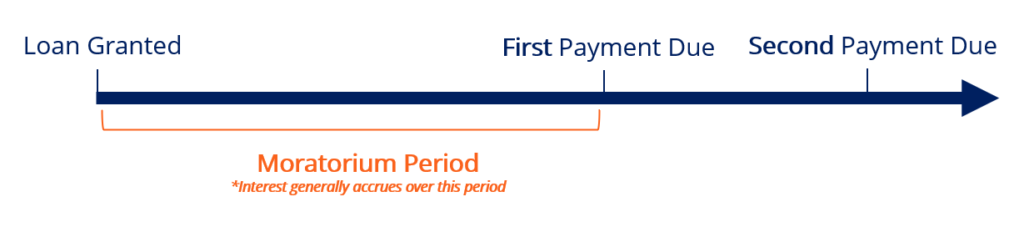

A moratorium period is illustrated below:

A moratorium period typically commences once a loan is granted. It is primarily extended to give the borrower adequate time to sort out finances and prepare for loan repayment. A moratorium period can also occur during the mid-life of a loan. It would be the case if the lender allows the borrower to stop making payments over a specified period for a specific reason – for example, due to financial hardship. It should be noted that interest on the loan generally accrues over the moratorium period.

John was provided a $500,000 loan by Money Tree Bank, a fictitious bank, in January 2020 to expand his restaurant business. John agreed to pay fixed monthly payments of $100,000 over six months (total repayment of $600,000) to secure the loan, with the first payment due at the start of February 2020 and subsequent payments at the start of each following month.

However, in mid-March 2020, John’s restaurant business was forced to close due to the coronavirus pandemic. Due to such an unprecedented event, Money Tree Bank decided to grant John a moratorium period from mid-March 2020 to June 2020 for no additional charge. As a result, John is now able to defer his April 2020 payment to July 2020.

The example above is graphically summarized below:

Examples of moratorium periods in the news are provided below:

The ability to defer payments into the future offers greater financial flexibility. However, it is important to recall that interest generally accrues over the moratorium period, resulting in a higher total loan amount payable.

Unless the borrower is under financial distress – i.e., unable to make payments – the financial flexibility of a moratorium period is largely offset by the additional interest charge.

A moratorium period is commonly confused with a grace period. It is important to note that a grace period is a set length of time after payment is due, where a payment can be made without penalty. In other words, a borrower is expected to make a payment over the grace period or face penalization – such as a late fee, credit rating downgrade, etc.

On the other hand, over a moratorium period, a borrower is not required to make a payment over the period. In addition to the distinct difference as outlined above, a moratorium period length can range from weeks to months, whereas a grace period length is usually 15 days.

CFI is the official provider of the global Commercial Banking & Credit Analyst (CBCA)™ certification program, designed to help anyone become a world-class financial analyst. To keep advancing your career, the additional resources below will be useful: