Cash Offer

An all-cash offer made by a purchaser to the seller of a real estate property

What is a Cash Offer?

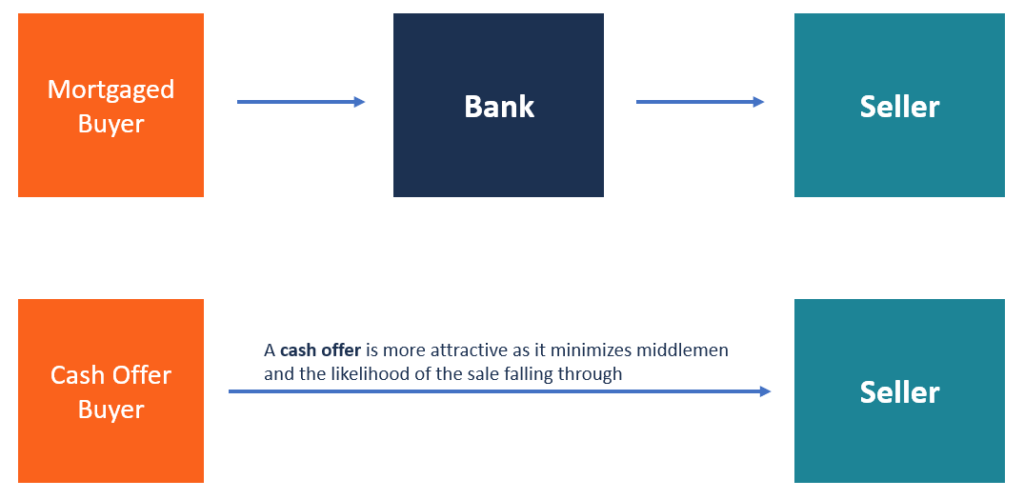

A cash offer refers to an all-cash offer made by a purchaser to the seller of a real estate property. The purchaser does not need a mortgage or any other type of financing to complete the transaction and is willing to pay cash to close the transaction. A cash buyer enjoys an advantage over other buyers who need a mortgage because the seller is interested in choosing a buyer who can close the transaction quickly without an uncertain underwriting process.

For a mortgaged buyer, there is no guarantee that the lender will approve the loan. Various factors such as credit score and home appraisal may cause the bank to reject the loan application. These factors make a financed offer usually less attractive to the seller, as compared to a cash offer that comes with no strings attached.

How to Make a Cash Offer on a House

Depending on the nature of the market, a cash offer provides several benefits to both the seller and the buyer. The buyer should follow the right procedure when making a cash offer to make sure it is accepted by the seller over other offers. Here is how to do it the right way:

1. Accumulate cash into one account

A buyer can source cash from various sources such as personal savings, cash gifts from family and friends, inheritance money, employment income, business income, etc. Accumulating the funds into one account can make it easy to track the money you will need at the time of closing. It will also be easy to produce one bank statement as proof of funds rather than having to provide multiple documents to the seller as proof of funds.

If the buyer intends to use proceeds from the sale of securities or real estate, the assets should be liquidated into cash before entering into a sale contract. The buyer should have ready cash before sitting down with an agent of the seller to write an offer to buy the property.

2. Prepare a budget for home-buying expenses

Apart from having ready cash for the real estate property, the buyer should also have a budget for other home-buying expenses. Some of the expenses may include property taxes, home inspection fees, and homeowner association fees. The total budget for all the expenses varies from state to state. The buyer should check out the specific costs before entering into a purchase contract.

3. Create the cash offer

The buyer or his/her agent should fill the form used in the state where the property is located. The buyer should include a modest deposit that boosts the credibility of the offer. They should also attach a copy of the latest bank statement as proof that the buyer has the funds required to close the transaction.

Presenting a cash offer removes the need for a financing contingency, which is a common requirement in real estate transactions where the buyer is using bank financing. Depending on market conditions, the buyer may present a lower offer than what other bidders with financing are offering the seller. The seller may be willing to accept a lower purchase price in exchange for being able to close a deal quickly.

4. Make the deal attractive

Where the seller is presented with a host of cash offers from interested bidders, the buyer will need to sweeten the deal to convince the seller that their offer is the best. Since a cash offer does not involve an underwriting process, the buyer may propose a nearby closing date of about 10 days instead of the usual 30 to 40 days or more.

If the property is new or recently renovated, the buyer can remove the home inspection contingency and offer to conduct a home inspection for information purposes only. Another way to sweeten the deal is to offer a premium price that is above all existing offers.

Benefits of a Cash Offer

The following are some of the reasons why sellers prefer a cash offer over other offers with loan financing:

1. Fast closing

A buyer who is offering cash for the purchase of a home does not need the lengthy waiting period of a traditional home sale. Once all the required contingencies have been met, the two parties can close the transaction in less than 10 days. The seller will get their money sooner, and the buyer will take over the ownership of the property within a short duration.

If the buyer is using loan financing, the process can go longer than a month as the lender verifies the creditworthiness of the buyer. If there are questions regarding the credibility of the borrower, the lender will not approve the loan, which will derail the process.

2. No contingencies

A traditional home sale that includes a mortgaged home buyer typically requires various contingencies before the transaction can be closed. Some of the contingencies include home inspection, appraisal, mortgage financing, etc. The contingencies serve to slow down the process. In the case of a cash offer, the buyer may choose to skip the contingencies and remove potential stumbling blocks that may derail the purchase of the property.

Drawbacks of a Cash Offer

Despite its advantages, a cash offer also comes with a number of drawbacks, including:

1. Tying up funds

Buyers will be tying up a lot of funds by offering to pay for the property all at once. They may face a shortage of cash that could have been used to invest in other assets.

2. Sacrifice tax deductions

A buyer that uses a mortgage to purchase a real estate property enjoys tax breaks on the mortgage interest payments. When a buyer decides to purchase a home using cash only, they miss out on the tax deductions that they would’ve enjoyed if they used mortgage financing to complete the transaction.

More Resources

CFI is the official provider of the Financial Modeling and Valuation Analyst (FMVA)® certification program, designed to transform anyone into a world-class financial analyst.

To keep learning and developing your knowledge of financial analysis, we highly recommend the additional CFI resources below:

Analyst Certification FMVA® Program

Below is a break down of subject weightings in the FMVA® financial analyst program. As you can see there is a heavy focus on financial modeling, finance, Excel, business valuation, budgeting/forecasting, PowerPoint presentations, accounting and business strategy.

A well rounded financial analyst possesses all of the above skills!

Additional Questions & Answers

CFI is the global institution behind the financial modeling and valuation analyst FMVA® Designation. CFI is on a mission to enable anyone to be a great financial analyst and have a great career path. In order to help you advance your career, CFI has compiled many resources to assist you along the path.

In order to become a great financial analyst, here are some more questions and answers for you to discover:

- What is Financial Modeling?

- How Do You Build a DCF Model?

- What is Sensitivity Analysis?

- How Do You Value a Business?