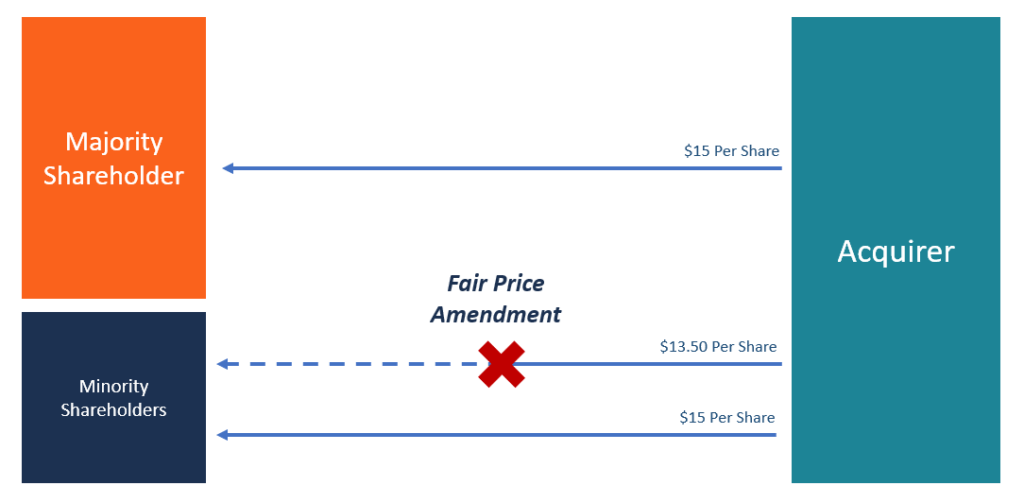

Fair Price Amendment

A provision requiring potential bidders to pay a fair price to acquire the shares held by minority stockholders

What is a Fair Price Amendment?

A fair price amendment is a provision contained in a public company’s charter that requires potential acquirers of the company to pay “a fair price” in order to acquire shares held by the company’s stockholders. The formula for calculating the fair market price that bidders should pay is provided for in the company’s charter and is frequently based on the company’s historical stock prices.

The goal of the fair price provision is to discourage hostile takeovers by making the acquisition more expensive. The provision also protects minority stockholders who may be offered a lower price for their shares than shareholders who own a significant percentage of the company’s stock.

Summary

- A fair price amendment is a provision contained in a public company’s charter or by-laws, usually inserted as a defense measure against a hostile takeover.

- The amendment requires bidders to offer a fair market price for all the stock shares they attempt to acquire.

- It protects minority stockholders from getting a lower price per share than what major stockholders of the company may receive.

How the Fair Price Amendment Works

Basically, the “fair price” is defined in practical, working terms as the highest price that a potential acquirer pays in order to attempt to obtain a majority stake in the target company. The price must exceed an amount determined by the board of directors of the target company. This amount is usually calculated relative to the book value of the company’s shares or recent annual earnings.

The fair price amendment deters acquirers from offering varied prices for stocks at different stages of acquisition. It protects stockholders from two-tier tender offers that discriminate against a portion of the stockholders – namely, those who only own a small percentage of the target company’s equity.

The fair price amendment protects the stockholders from such discrimination by requiring a uniform offer for all shares tendered for purchase. The provision can only be reversed by the board of directors of the target company through a supermajority decision, i.e., one exceeding 95% of the voting rights.

Two-Tier Tender Offer: How Does it Work

A two-tier tender offer is an offer where the acquirer starts by offering an attractive price (higher price per share or a higher proportion of cash) for a limited number of shares in the target company. The first tier is designed to give the acquiring entity greater control in the decision-making process of the target company. It is followed by another offer to acquire more shares, but at a reduced price per share as compared to the original offer. The goal of completing an acquisition through a two-tier system is to reduce the overall cost of acquisition.

For example, an acquirer may present a premium offer of $60 per share in the first tier, so that a majority of the stockholders may agree to dispose of their shareholding. The first offer is designed to provide the acquiring company with an upper hand in the control of the target company.

After gaining majority ownership of the target, the acquirer then offers $40 per share for the remaining shares at a later date. The strategy benefits the acquirer by reducing the overall cost of the acquisition compared to offering a single tender offer at a higher price.

However, a two-tiered tender offer is not beneficial for the stockholders of the target company since it forces them to accept an offer immediately or else risk having to accept a reduced offer later.

Calculating the Fair Market Value

One of the most commonly used criteria for calculating the fair market price of a stock is the P/E ratio. The Price-to-Earnings ratio can be computed as a multiple of the historical earnings reported by the target company, or by looking at the average P/E ratio for all the stocks of publicly traded companies in the same industry category as the target company.

An alternative to using the P/E ratio to price the stock is to use the Enterprise Value to Revenue ratio. The EV to Revenue ratio can be used to calculate a fair price for the stock as a multiple of the company’s historical revenues. You may also consider the price-to-sales ratio of other companies that are in the same industry as the target company.

Additional Resources

CFI is the official provider of the global Financial Modeling & Valuation Analyst (FMVA)™ certification program, designed to help anyone become a world-class financial analyst. To keep advancing your career, the additional CFI resources below will be useful:

Analyst Certification FMVA® Program

Below is a break down of subject weightings in the FMVA® financial analyst program. As you can see there is a heavy focus on financial modeling, finance, Excel, business valuation, budgeting/forecasting, PowerPoint presentations, accounting and business strategy.

A well rounded financial analyst possesses all of the above skills!

Additional Questions & Answers

CFI is the global institution behind the financial modeling and valuation analyst FMVA® Designation. CFI is on a mission to enable anyone to be a great financial analyst and have a great career path. In order to help you advance your career, CFI has compiled many resources to assist you along the path.

In order to become a great financial analyst, here are some more questions and answers for you to discover:

- What is Financial Modeling?

- How Do You Build a DCF Model?

- What is Sensitivity Analysis?

- How Do You Value a Business?