Subsidiary Merger

A type of merger in which the acquiring company uses its subsidiary to acquire a target company

What is a Subsidiary Merger?

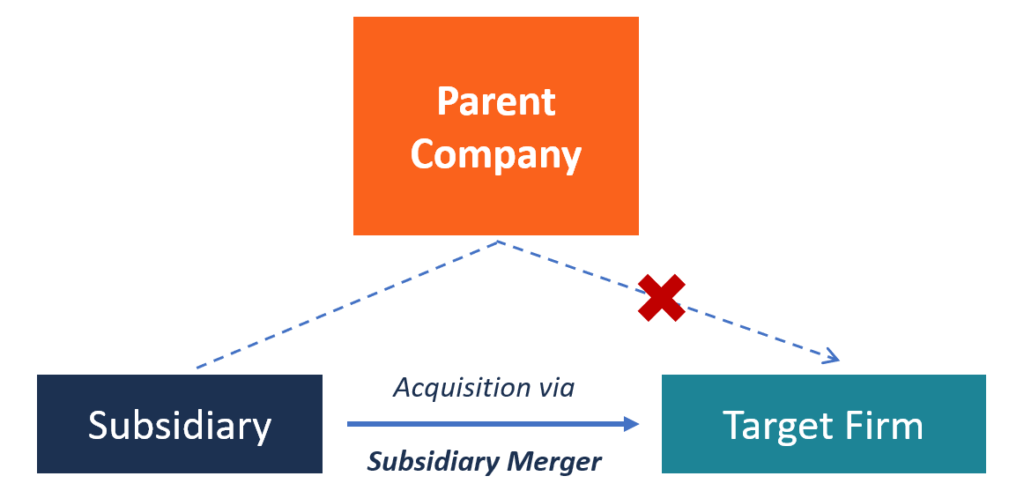

A subsidiary merger is a type of merger that occurs when the acquiring company uses its subsidiary company to acquire a target company. The acquirer may create a subsidiary company or use one of its existing subsidiary companies to execute the merger and acquisition transaction.

In a subsidiary merger, the acquired company is merged with the subsidiary of the acquirer rather than merging directly with the acquiring company (the parent company) in a regular M&A deal.

Following the deal, the target company becomes a wholly-owned subsidiary of the acquiring company, with the buyer (the parent company) as the sole shareholder. This means that the acquirer exerts total control over the entity, potentially gaining control of the latter’s non-transferable assets and contracts. The main purpose of a subsidiary merger is to protect the buyer from the liabilities of the target company.

Types of Subsidiary Merger

The following are the two main types of subsidiary mergers:

1. Forward Triangular Merger

A forward triangular merger is an indirect merger where a subsidiary of the purchasing company completes the acquisition on behalf of its parent company. The subsidiary company acquires all the assets and liabilities of the target company. The acquired company then becomes a fully owned subsidiary of the purchasing entity. After the acquisition, the target company is liquidated, and the buyer becomes the sole shareholder of the combined entity.

Pros and Cons of a Forward Triangular Merger

One of the reasons buyers prefer a forward triangular merger is that it gives them more flexibility in purchasing the target company. Buyers can use a combination of both cash and stock. Half of the consideration used to pay the target company’s shareholders must be at least 50% stock of the acquirer. If the consideration for the transaction were 100% cash, it would make the transaction taxable.

On the downside, forward triangular mergers are less preferred than reverse triangular mergers due to issues regarding access to the target company’s licenses and authorizations. The properties will need to be reassessed, and some third parties may withhold consent to the acquirer gaining use of the target company’s contracts, licenses, and authorizations. The acquiring entity may incur additional costs to be granted consent to the rights of the licenses and assignment of contracts.

2. Reverse Triangular Merger

A reverse triangular merger shares many similarities with a forward triangular merger; however, they differ in the liquidated party. In a forward triangular merger, the target company is liquidated, whereas, in a reverse triangular merger, the subsidiary created by the purchasing entity is liquidated.

A reverse triangular subsidiary merger begins when an acquiring entity uses its subsidiary to acquire another company. After the acquisition, the subsidiary is absorbed into the acquired company, and the buyer (the parent company) becomes the only shareholder. The acquired company becomes a wholly-owned subsidiary of the acquiring entity, and the buyer acquires all the assets and liabilities of the acquired company.

Pros and Cons of Reverse Triangular Merger

A reverse triangular merger retains the selling entity and liquidates the shell company created for the purpose of executing the acquisition. The acquired entity continues its regular operations as a subsidiary of the buyer, and the acquiring entity will not need to sign new contracts, licenses, and authorizations. This makes the reverse triangular merger more often preferred over a forward triangular merger.

For the merger transaction to be tax-free, the acquiring entity must use its stock to acquire 80% of the target company’s stock. Cash and other non-stock consideration must not exceed 20% of the total consideration paid if the buyer wants to enjoy a tax-free acquisition transaction.

Additional Resources

CFI is the official provider of the Financial Modeling and Valuation Analyst (FMVA)® certification program, designed to transform anyone into a world-class financial analyst.

To keep learning and developing your knowledge of financial analysis, we highly recommend the additional CFI resources below:

Analyst Certification FMVA® Program

Below is a break down of subject weightings in the FMVA® financial analyst program. As you can see there is a heavy focus on financial modeling, finance, Excel, business valuation, budgeting/forecasting, PowerPoint presentations, accounting and business strategy.

A well rounded financial analyst possesses all of the above skills!

Additional Questions & Answers

CFI is the global institution behind the financial modeling and valuation analyst FMVA® Designation. CFI is on a mission to enable anyone to be a great financial analyst and have a great career path. In order to help you advance your career, CFI has compiled many resources to assist you along the path.

In order to become a great financial analyst, here are some more questions and answers for you to discover:

- What is Financial Modeling?

- How Do You Build a DCF Model?

- What is Sensitivity Analysis?

- How Do You Value a Business?