Get Certified for

Capital Markets (CMSA®)

From equities and fixed income to derivatives, the CMSA certification bridges the gap from where you are now to where you want to be — a world-class capital markets analyst.

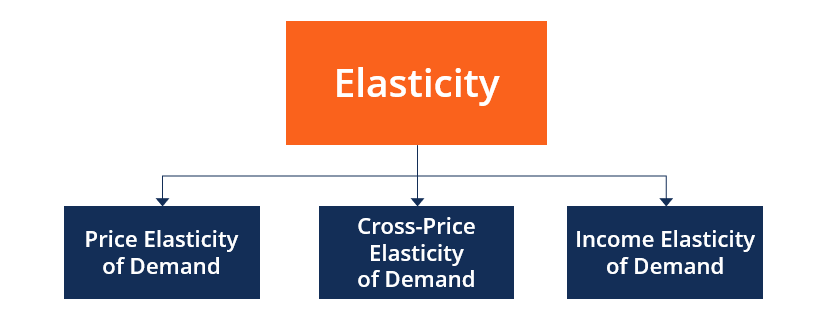

A general measure of the responsiveness of an economic variable in response to a change in another economic variable

Elasticity is a general measure of the responsiveness of an economic variable in response to a change in another economic variable. Economists utilize elasticity to gauge how variables affect each other. The three major forms of elasticity are price elasticity of demand, cross-price elasticity of demand, and income elasticity of demand.

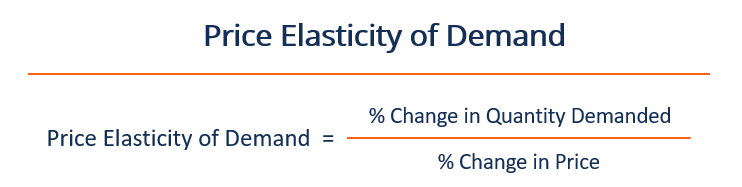

Price elasticity of demand demonstrates how a change in price affects the quantity demanded. It is computed as the percentage change in quantity demanded over the percentage change in price, and it will commonly result in a negative elasticity because of the law of demand.

The law of demand states that an increase in price reduces the quantity demanded, and it is why demand curves are downwards sloping unless the good is a Giffen good. It is common to simply drop the negative of the quotient.

The larger the price elasticity of demand, the more responsive quantity demanded is given a change in price. When the price elasticity of demand is greater than one, the good is considered to demonstrate elastic demand. When the quantity demanded drops to zero with a rise in price, it is said that demand is perfectly elastic. If the price of an elastic good increases, there is a corresponding quantity effect, where fewer units are sold, and therefore reducing revenue.

The lower the price elasticity of demand, the less responsive the quantity demanded is given a change in price. When the price elasticity of demand is less than one, the good is considered to show inelastic demand. When the quantity demanded does not respond to a change in price, it is said that demand is perfectly inelastic. If an inelastic good has its price increased, it will lead to increased revenues because each unit will be sold at a higher price.

If a change in price comes with the same proportional change in the quantity demanded, it is said that the good is unit elastic. Indicating that X% change in price results in an X% change in the quantity demanded. Therefore, if the price elasticity of demand equals one, the good is unit elastic. If a good shows a unit elastic demand, the quantity effect and price effect exactly offset each other.

The midpoint method is a commonly used technique to calculate the percent change of price. The primary difference is that it calculates the percentage change of quantity demanded and the price change relative to their average.

If consumers can substitute the good for other readily available goods that consumers regard as similar, then the price elasticity of demand would be considered to be elastic. If consumers are unable to substitute a good, the good would experience inelastic demand.

The price elasticity of demand is lower if the good is something the consumer needs, such as Insulin. The price elasticity of demand tends to be higher if it is a luxury good.

The price elasticity of demand tends to be low when spending on a good is a small proportion of their available income. Therefore, a change in the price of a good exerts a very little impact on the consumer’s propensity to consume the good. Whereas, when a good represents a large chunk of the consumer’s income, the consumer is said to possess a more elastic demand.

In the long term, consumers are more elastic over longer periods, as over the long term after a price increase of a good, they will find acceptable and less costly substitutes.

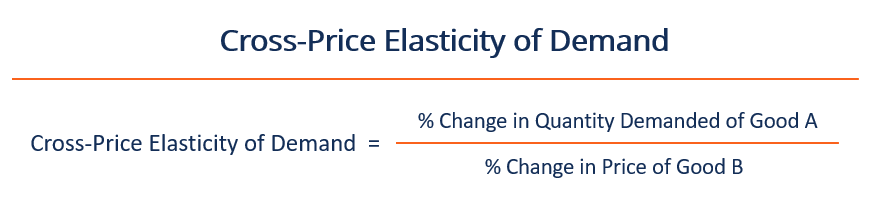

The cross-price elasticity of demand measures how the demand for one good is impacted by a change in the price of another good. It is calculated as the percentage change of Quantity A divided by the percentage change in the price of the other.

If the cross-price elasticity of demand between two goods is positive, it implies that the two goods are substitutes. Consider the following substitute goods – good A and good B. If the price of good B rises, the demand for good A rises.

On the contrary, if the aforementioned goods were complements, when the price of good B increases, the demand for good A should decrease. It is what is implied through the cross-price elasticity of demand formula. It is important to note that the cross-price elasticity of demand is a unitless measure.

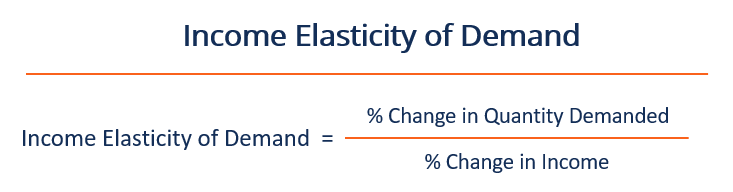

The income elasticity of demand is defined as the measure of the percentage change of the quantity demanded of a good in reference to changes in the consumer’s income. Calculating the income elasticity of demand allows economists to identify normal and inferior goods, as well as how responsive quantity demanded is to changes in income.

If the income elasticity of demand is positive, the good is considered to be a normal good – implying that when income increases, the quantity demanded at any given price increases.

If the income elasticity of demand is negative, the good is considered to be an inferior good – implying that when income increases, the quantity demanded at any given price decreases.

If the income elasticity of demand is higher than 1, then the good is considered to be income elastic, implying that demand rises faster than income. Luxury goods include international vacations or second homes.

If the income elasticity of demand is higher than 0 but less than 1, then the good is income inelastic, implying that demand for income-inelastic goods rises but at a slower rate than income.

Connect what you just learned to a clear career path with CFI’s role‑based courses and certification programs.

Thank you for reading CFI’s guide on Elasticity. To keep learning and advancing your career, the following resources will be helpful: