Get Certified for Financial Modeling (FMVA)®

Gain in-demand industry knowledge and hands-on practice that will help you stand out from the competition and become a world-class financial analyst.

Evaluating a company's short-term liquidity

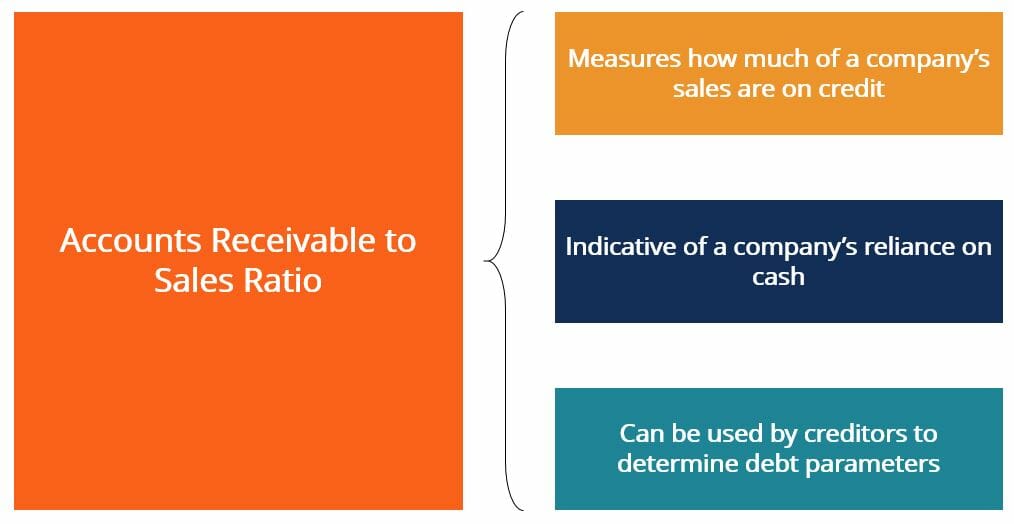

The Accounts Receivable to Sales Ratio is a business liquidity ratio that measures how much of a company’s sales occur on credit. When a company has a larger percentage of its sales happening on a credit basis, it may run into short-term liquidity problems. Such a scenario may happen if a company is running low on cash due to a lack of cash sales in the business cycle.

The Accounts Receivable to Sales Ratio is useful in evaluating how inclined a company is to conduct business on a credit basis. This can provide insight into its operational structure. A company that is able to run fine with little cash may have very small fixed costs or a low amount of debt in its capital structure.

Having a very high AR to Sales ratio can be a negative indicator to debt providers, since high credit sales may compromise a company’s ability to make periodic interest payments. Furthermore, a very high ratio indicates that a company may not have much of a cash cushion to rely on during difficult economic times or slow sales cycles.

The Accounts Receivable to Sales Ratio is calculated by dividing the company’s sales for a given accounting period by its accounts receivables for the same period. The formula to calculate this ratio is as follows:

Where:

Accounts Receivable – refers to sales that have occurred on credit, meaning that the company has not yet collected the cash proceeds from these sales. Found in the “current assets” section of the balance sheet.

Sales – refers to all sales that the company has realized over the given accounting period, including sales on credit and cash sales. Found on the income statement.

Generally speaking, a low Accounts Receivable to Sales ratio is almost always favorable, as it means that the company’s cash collection cycle does not represent a great liquidity risk. The bulk of the company’s sales go into its cash account, which can then be used to finance the business. A low AR to Sales ratio also means that the business is generating fairly large cash flows from its operations. It relies less on its investing and financing activities for liquidity.

However, a company can see some benefit to having mostly credit sales in the form of accrued interest. Businesses can incentivize purchasers to pay within a certain time frame by treating accounts receivable as debt and charging interest beyond a certain time.

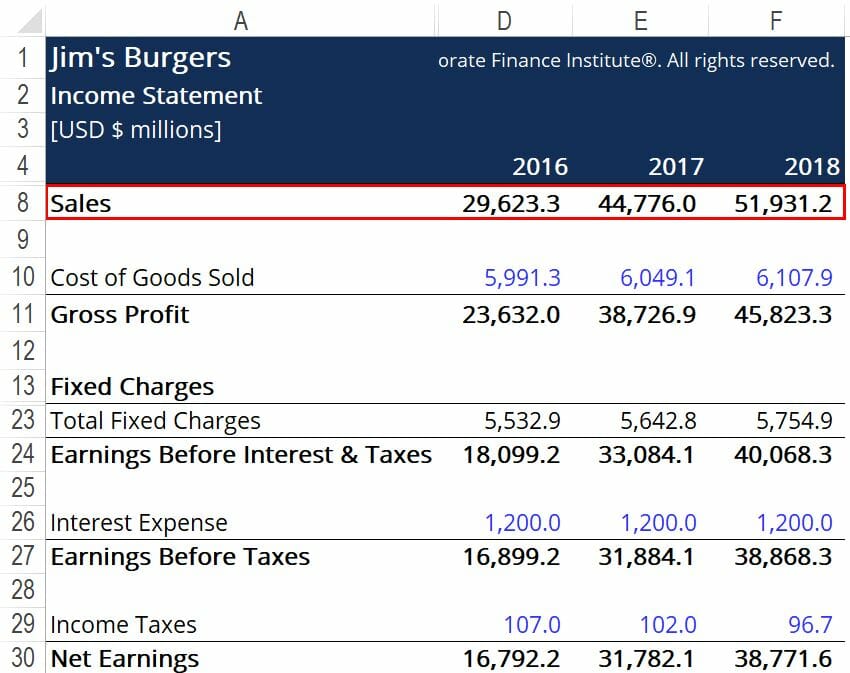

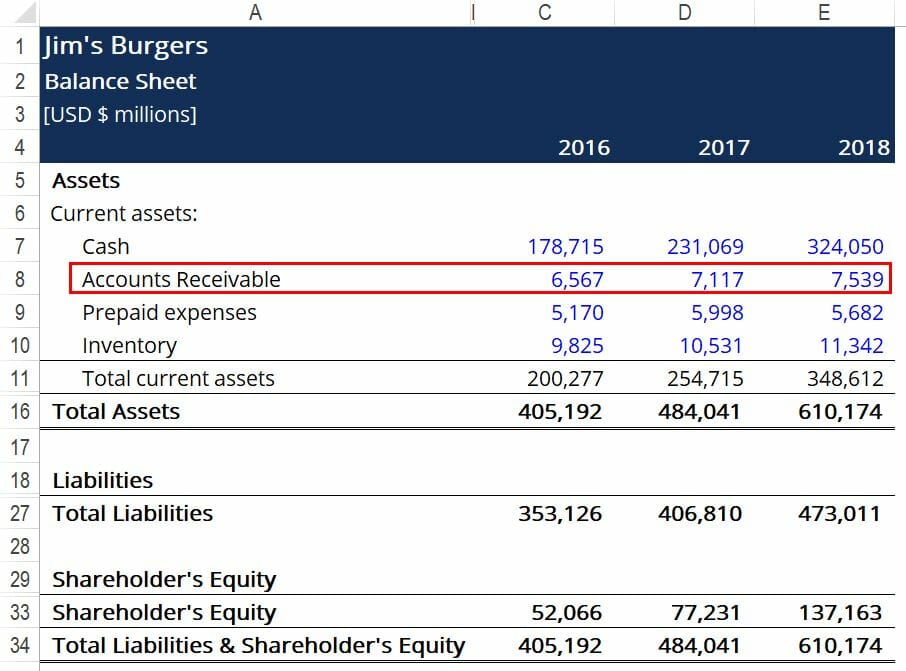

Jim’s Burgers wants to calculate its Accounts Receivables to Sales ratio for the past few years in order to get a better understanding of its probable future liquidity. Below are snippets from Jim’s financial statements:

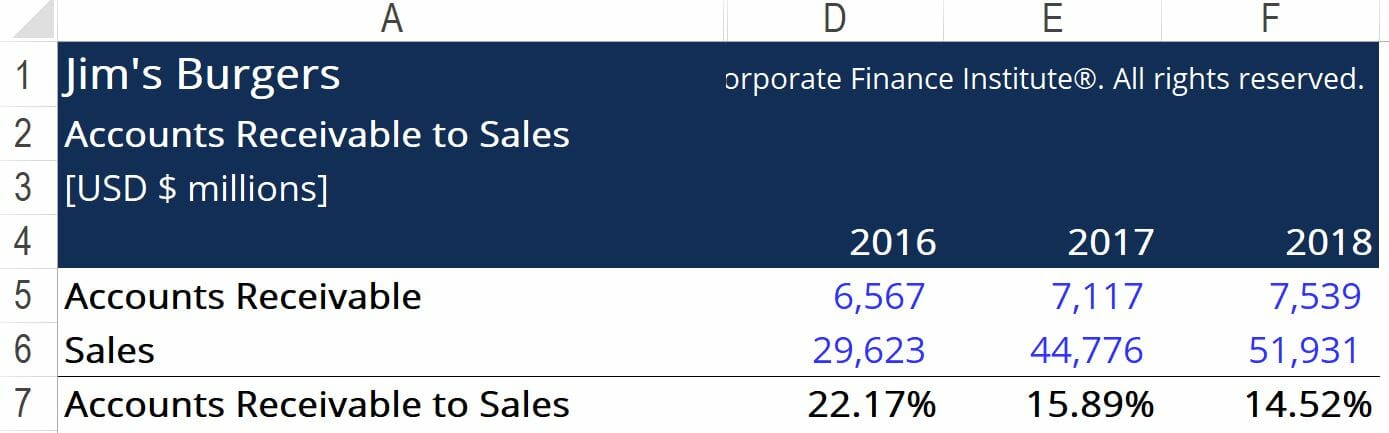

The red boxes highlight the important information that we need to calculate Accounts Receivables to Sales, namely the company’s current accounts receivable and its total sales. Using the formula provided above, we arrive at the following figures:

In this case, we see that Jim’s AR to sales ratio is consistently decreasing year over year, which is indicative of improving liquidity for the business. This means that an increasing number of purchasers are buying from Jim’s with cash upfront, rather than on credit. This will likely lead to an increase in Jim’s operating cash flow, which may allow the company to consider debt financing in the future.

Thank you for reading CFI’s guide to Accounts Receivable to Sales Ratio. To learn more about related topics, check out the following CFI resources: