Get Certified for Financial Modeling (FMVA)®

Gain in-demand industry knowledge and hands-on practice that will help you stand out from the competition and become a world-class financial analyst.

Comparing EBIT and EBITDA

The difference between EBIT and EBITDA is that Depreciation and Amortization have been added back to Earnings in EBITDA, while they are not backed out of EBIT. This guide on EBIT vs EBITDA will explain everything you need to know!

EBIT stands for: Earnings Before Interest and Taxes.

EBITDA stands for: Earnings Before Interest, Taxes, Depreciation, and Amortization.

As noted above, EBIT represents earnings (or net income/profit, which is the same thing) that have interest and taxes added back to them. On an income statement, EBIT can be easily calculated by starting at the Earnings Before Tax line and adding back to that figure any interest expenses the company may have incurred.

To spell it out one more time, EBITDA stands for Earnings Before Interest, Taxes, Depreciation, and Amortization. The additional adding back of Depreciation and Amortization is the only difference between EBIT vs EBITDA.

EBITDA can be harder to calculate from the income statement. Depreciation and Amortization can be included in several spots on the income statement (in Cost of Goods Sold and as part of General & Administrative expenses, for example) and, therefore, require special focus.

The easiest way to ensure that you have the full depreciation and amortization numbers is by checking the Cash Flow Statement, where they will be fully broken out.

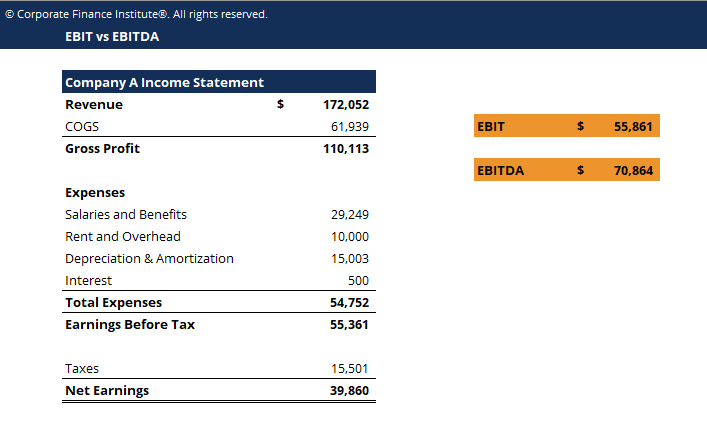

The example below shows how to calculate EBIT and EBITDA on a typical income statement.

We will take you through this example step by step, so you can see how to calculate each of these metrics on your own.

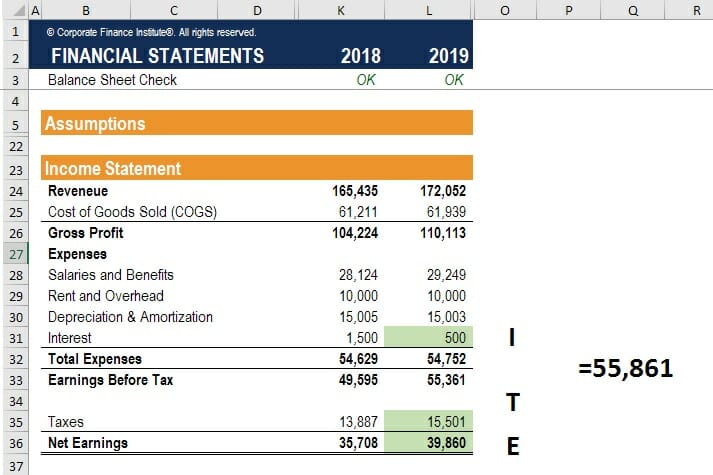

For the EBIT example, let’s take the numbers in 2019, starting with Earnings, and then add back Taxes and Interest.

The EBIT formula is:

EBIT = 39,860 + 15,501 + 500 = 55,861

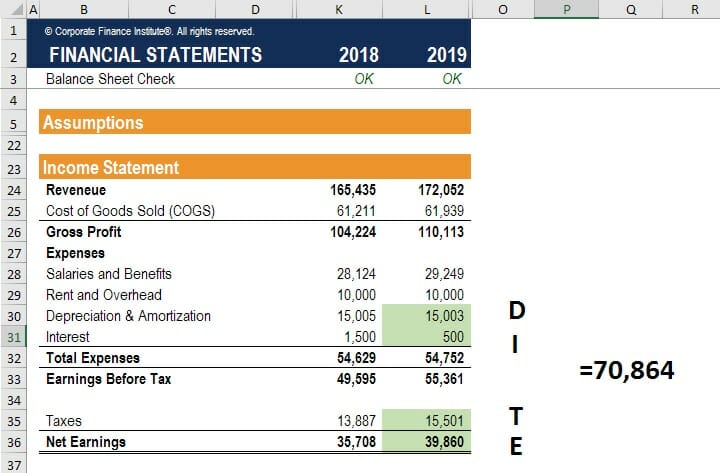

In the EBITDA example, let’s continue to use the 2019 data and now take everything from the EBIT example and also add back 15,003 of Depreciation.

The EBITDA formula is:

EBITDA = 39,860 + 15,501 + 500 + 15,003 = 70,864

Download CFI’s free Excel template that compares EBITDA vs EBIT calculations. Try rebuilding the formulas and changing the numbers around to fully understand the differences.

Just enter your name and email in the form below and you can download the free template now!

The above example of EBIT vs EBITDA shows how you can calculate the numbers by starting with earnings before tax and then adding back the appropriate line items on the income statement.

There is a lot of debate about which metric is better, and there are good arguments on both sides of the fence.

For a company or industry with relatively low capital expenditures required to maintain its operations, EBITDA can be a good proxy for cash flow.

However, for companies in capital-intensive industries such as oil and gas, mining, and infrastructure, EBITDA is a near meaningless metric. The extensive amount of capital spending required means that EBITDA and cash flow will often be very far apart. In such a case, EBIT may be more appropriate, as the Depreciation and Amortization captures a portion of past capital expenditures.

To see more on the topic, we’ve outlined why Warren Buffett does not like to use EBITDA. As he put it, “Do people think the Tooth Fairy pays for capital expenditures?”

Depreciation doesn’t perfectly correspond to capital expenditures, but it is analogous and represents a smoothed-out version of such expenditures over time.

People who favor using EBIT explain that, over time, depreciation is relatively representative of capital expenditures (Capex), and Capex is required to run the business, so it makes sense to look at earnings after depreciation.

On the other hand, capital expenditures can be extremely lumpy, and sometimes are discretionary (i.e., the money is spent on growth as opposed to sustaining the business).

People who favor using EBITDA view Capex as largely discretionary and therefore think it should be excluded.

Capital-intensive industries will trade at very low EV/EBITDA multiples because their depreciation expense and capital requirements are so high. This means they could be a “value trap” to the untrained eye (i.e., they appear undervalued but actually are not).

EBIT multiples will always be higher than EBITDA multiples and may be more appropriate for comparing companies across different industries.

The key is to know your industry and which metrics are most commonly used and most appropriate for it.

For true intrinsic value analysis, such as in financial modeling, EBITDA is not even relevant, as we rely entirely on unlevered free cash flow to value the business.

Connect what you just learned to a clear career path with CFI’s role‑based courses and certification programs.

Thank you for reading CFI’s guide to EBIT vs EBITDA. To keep learning and advancing your career, the following CFI resources will be helpful: