Get Certified for Financial Modeling (FMVA)®

Gain in-demand industry knowledge and hands-on practice that will help you stand out from the competition and become a world-class financial analyst.

The market value of the assets owned by shareholders after all debts have been repaid

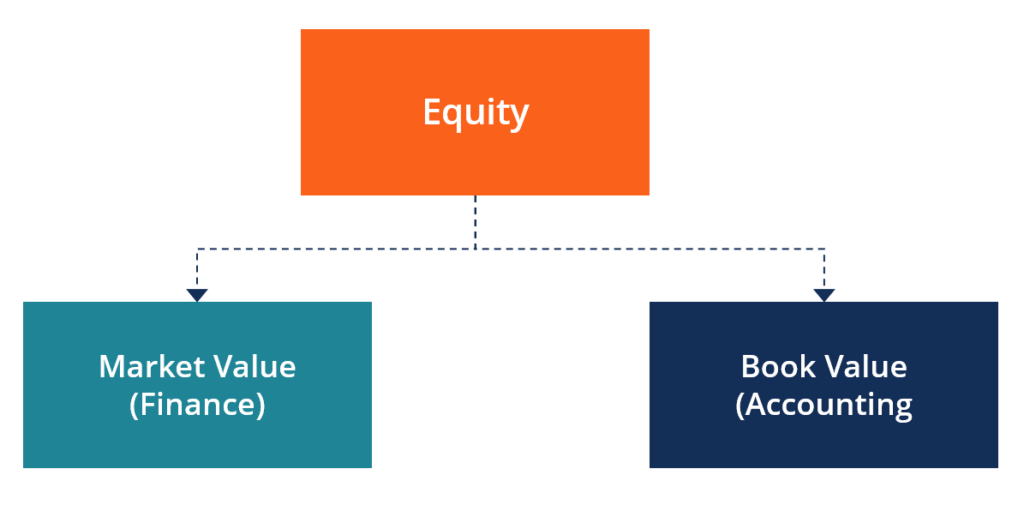

In finance, equity is the market value of the assets owned by shareholders after all debts have been paid off. In accounting, equity refers to the book value of stockholders’ equity on the balance sheet, which is equal to assets minus liabilities. The term, “equity”, in finance and accounting comes with the concept of fair and equal treatment to all shareholders of a business on a pro-rata basis.

Image: CFI’s Intro to Corporate Finance Course

Owners of a company (whether public or private) have shares that legally represent their ownership in the company. Each share of the same class has the exact same rights and privileges as all other shares of the same class. This is part of the term’s meaning – equity meaning “equal”.

Companies can issue new shares by selling them to investors in exchange for cash. Companies use the proceeds from the share sale to fund their business, grow operations, hire more people, and make acquisitions. Once the shares have been issued, investors can buy and sell them from each other in the secondary market (how stocks normally trade on an exchange).

There are two main applications of the term, each of which is discussed below:

Financial analysts are typically concerned with the market value of equity, which is the current price or fair value they believe shares of the business are worth. Since finance professionals want to know how much of a return they can make on an investment, they need to understand how much the investment will cost them, and how much they believe they can sell it for.

Market Value Formula

There are various ways to calculate or estimate the market value of equity for a company. Below are several methods that can be used to calculate the value:

To learn more about how financial analysts value companies, check out CFI’s Business Valuation Fundamentals Course.

Example

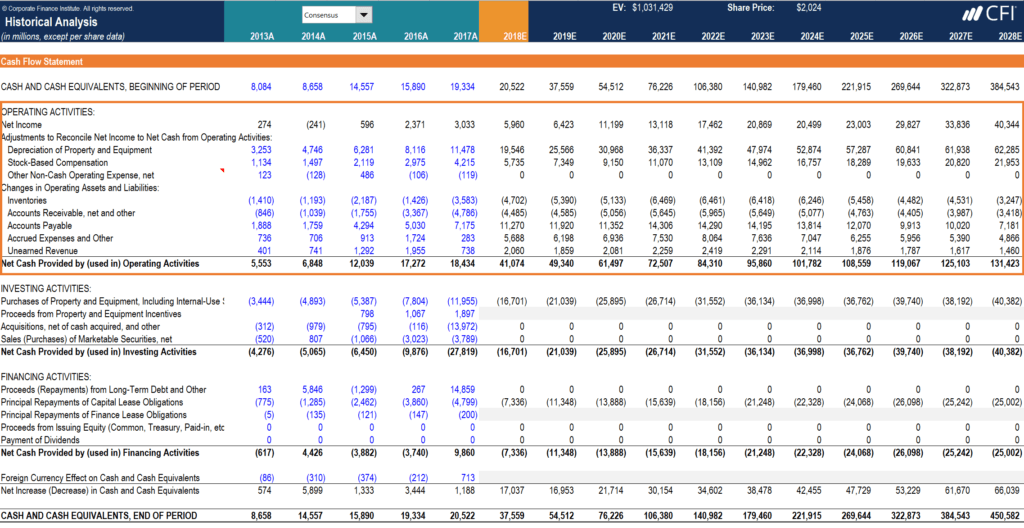

In the example below from CFI’s Financial Modeling Course about Amazon, you can see how an analyst can build a Discounted Cash Flow (DCF) model to forecast the company’s cash flows into the future and then discount them back to the present. After netting out debts owed, the resulting value is divided by the number of shares outstanding to arrive at the intrinsic value of equity per share.

Accountants are concerned with recording and reporting the financial position of a company, and, therefore, focus on calculating the book value of equity. In order for the balance sheet to balance, the formula Equity = Assets – Liabilities must be true.

Book Value Formula

There are various ways to calculate or calculate the book value of equity for a company. Below are several methods that can be used to calculate the value:

To learn more about financial statements, check out CFI’s Accounting Courses.

Example

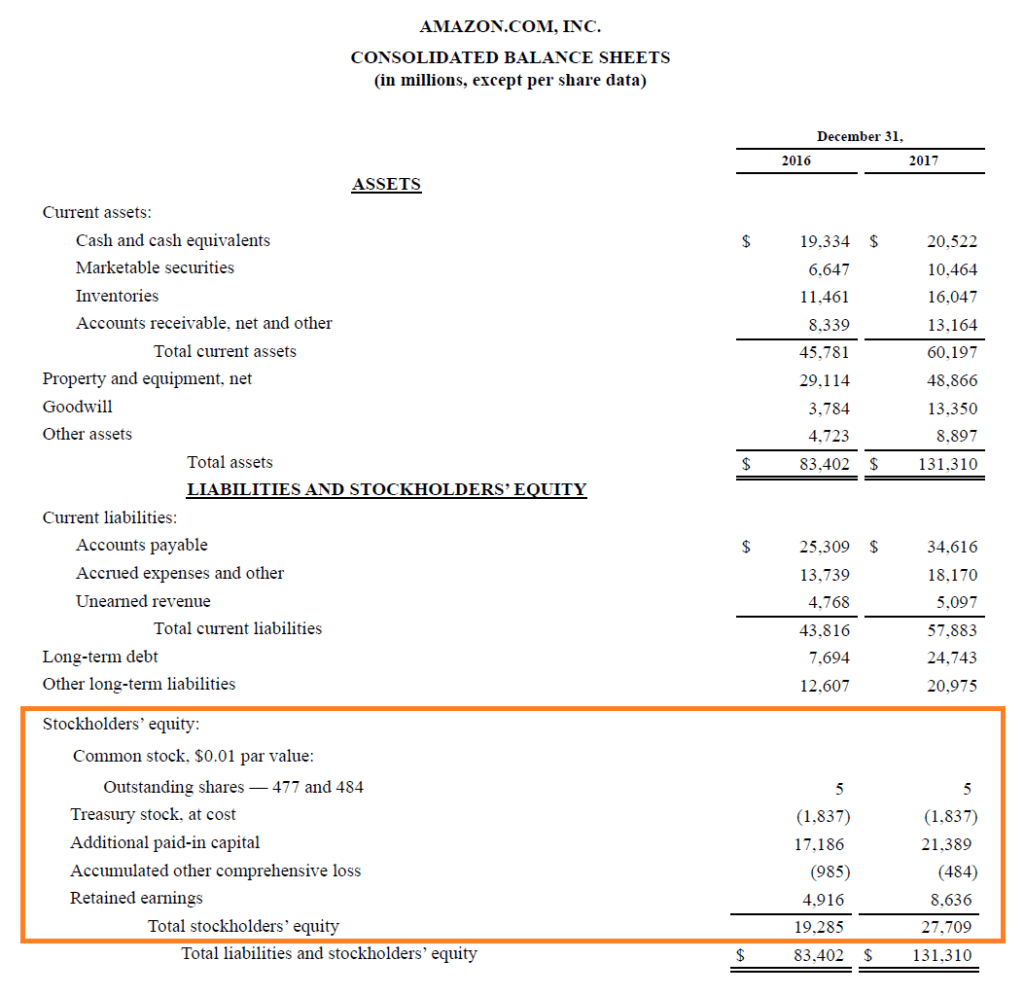

Below is a screenshot of Amazon’s 2017 balance sheet, which shows a breakdown of the book value of its stockholders’ equity. As you can see, in 2017, the company reported total stockholders’ equity of $27.7 billion.

The main difference between market value and book value is that market value is forward-looking (expectations about the future), and book value is backward-looking (recording a history of what happened in the past).

Finance professionals are typically concerned with forecasting or estimating how a company will perform in the future. Accountants, on the other hand, are focused on providing a detailed and accurate picture of what has actually happened, and, thus, they focus on the past.

Since one is forward-looking and the other is backward-looking, there may be a large discrepancy between market value and book value. This is not necessarily a “good” or “bad” thing.

In order to assess how large the gap is between the market value and book value of a company’s equity, analysts will often use the Price-to-Book (P/B) ratio.

CFI offers the Financial Modeling & Valuation Analyst (FMVA)™ certification program for those looking to take their careers to the next level. To keep learning and advancing your career, the following CFI resources will be helpful: