Get Certified for Financial Modeling (FMVA)®

Gain in-demand industry knowledge and hands-on practice that will help you stand out from the competition and become a world-class financial analyst.

The amount of debt that a company uses to fund its operations in proportion to equity capital

Gearing is the amount of debt, in proportion to equity capital, that a company uses to fund its operations. A company that possesses a high gearing ratio shows a high debt to equity ratio, which potentially increases the risk of financial failure of the business.

Gearing serves as a measure of the extent to which a company funds its operations using money borrowed from lenders versus money sourced from shareholders. An appropriate level of gearing depends on the industry in which a company operates. Therefore, it’s important to look at a company’s gearing ratio relative to that of comparable firms.

Several gearing ratios exist that compare the owner’s equity to the funds borrowed by a company. Gearing ratios measure a company’s level of financial risk. The best-known gearing ratios include:

When a company possesses a high gearing ratio, it indicates that a company’s leverage is high. Thus, it is more susceptible to any downturns that may occur in the economy. A company with a low gearing ratio is generally considered more financially sound.

The degree of gearing, whether low or high, reveals the level of financial risk that a company faces. A highly geared company is more susceptible to economic downturns and faces a greater risk of default and financial failure. This means that with the limited cash flows that the company is getting, it must meet its operational costs and make debt payments. A company may frequently experience a shortfall in cash flows and fail to pay equity shareholders and creditors.

A low gearing ratio may not necessarily mean that the business’ capital structure is healthy. Capital intensive firms and firms that are highly cyclical may not be able to finance their operations from shareholder equity only. At some point, they will need to obtain financing from other sources in order to continue operations. Without debt financing, the business may be unable to fund most of its operations and pay internal costs.

A business that does not use debt capital misses out on cheaper forms of capital, increased profits, and more investor interest. For example, companies in the agricultural industry are affected by seasonal demands for their products. They, therefore, often need to borrow funds on at least a short-term basis.

Lenders use gearing ratios to determine whether to extend credit or not. They are in the business of generating interest income by lending money. Lenders consider gearing ratios to help determine the borrower’s ability to repay a loan.

For example, a startup company with a high gearing ratio faces a higher risk of failing. Most lenders would prefer to stay away from such clients. However, monopolistic companies like utility and energy firms can often operate safely with high debt levels, due to their strong industry position.

Investors use gearing ratios to determine whether a business is a viable investment. Companies with a strong balance sheet and low gearing ratios more easily attract investors. Investors may view companies with a high gearing ratio as too risky.

A highly geared firm is already paying high amounts of interest to its lenders and new investors may be reluctant to invest their money, since the business may not be able to pay back the money.

Gearing ratios are used as a comparison tool to determine the performance of one company vs another company in the same industry. When used as a standalone calculation, a company’s gearing ratio may not mean a lot. Comparing gearing ratios of similar companies in the same industry provides more meaningful data.

For example, a company with a gearing ratio of 60% may be perceived as high risk. But if its main competitor shows a 70% gearing ratio, against an industry average of 80%, the company with a 60% ratio is, by comparison, performing optimally.

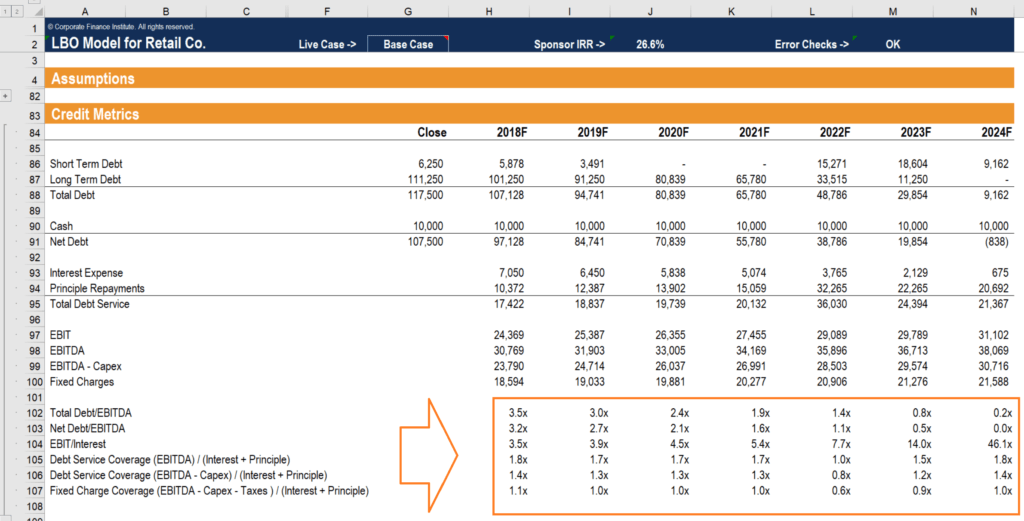

Below is a screenshot from CFI’s Leveraged Buyout (LBO) Modeling course, in which a private equity firm uses significant leverage to enhance the internal rate of return (IRR) for equity investors.

There are several instances when a company may engage in financial gearing to strengthen its capital structure, including the following:

When sourcing for new capital to support the company’s operations, a business enjoys the option of choosing between debt and equity capital. Most owners prefer debt capital over equity, since issuing more stocks will dilute their ownership stake in the company. A profitable company can use borrowed funds to generate more revenues and use the returns to service the debt, without affecting the ownership structure.

A company that mainly relies on equity capital to finance operations throughout the year may experience cash shortfalls that affect the normal operations of the company. The best remedy for such a situation is to seek additional cash from lenders to finance the operations. Debt capital is readily available from financial institutions and investors as long as the company appears financially sound.

A company may require a large amount of capital to finance major investments such as acquiring a competitor firm or purchasing the essential assets of a firm that is exiting the market. Such investments require urgent action, and shareholders may not be in a position to raise the required capital due to the time limitations. If the business is on good terms with its creditors, it may obtain large amounts of capital quickly as long as it meets the loan requirements.

Thank you for reading CFI’s explanation of Gearing. CFI is the official provider of the Financial Modeling and Valuation Analyst (FMVA) certification program, designed to transform anyone into a world-class financial analyst. To keep learning and developing your knowledge of financial analysis, we highly recommend the additional CFI resources below: