Get Certified for

Commercial Banking (CBCA®)

Stand out and gain a competitive edge as a commercial banker, loan officer, or credit analyst with advanced knowledge, real-world analysis skills, and career confidence.

A measure of the financial performance of a REIT

The P/AFFO is calculated by adding the P/FFO to any rent increases and subtracting capital expenditures and routine maintenance costs. The P/AFFO is a measure of the financial performance of a REIT (Real Estate Investment Trust). It is equal to the P/FFO adjusted to consider capital expenditures and regular maintenance costs, making it a more accurate REIT valuation tool than P/FFO.

It is also a more precise predictor of dividends that a company will pay in the future, and it can help potential investors make a decision on whether or not to buy shares of the company. The P/AFFO is also known as the Funds Available for Distribution.

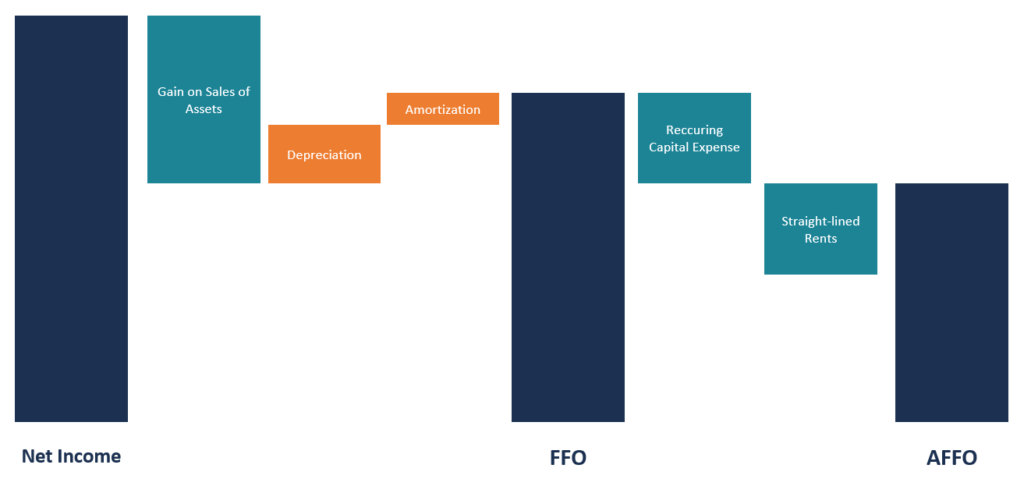

The calculation of the P/AFFO requires that we first determine the P/FFO and then deduct other forms of expenditures from the P/FFO to get the P/AFFO. The P/FFO is used to evaluate cash flow from real estate investments. It is calculated by first getting the net income of the company and then adding back any depreciation and amortization costs during the period. The depreciation is added back to the equation because real estate properties appreciate in value, and deducting depreciation would distort the value of a property.

The P/AFFO is obtained from taking the P/FFO value and then deducting capital expenditures like maintenance costs and any capital gains on the sale of the property. The capital gains on the property sale are deducted since it’s a one-time event and does not result in any long-term effect on the property.

The P/AFFO ratio measures a REIT’s ability to pay dividends to shareholders in the long term. The payout ratio is calculated by taking a REIT’s yearly dividend rate and dividing it by the estimated P/AFFO per share. It helps evaluate the REIT’s operations cash flow after taking into account the capital expenditures and other routine maintenance costs.

If a calculated ratio is over 100%, it means that the dividends of that REIT are higher than income projected for future operations. As a result, the REIT can be obliged to pay dividends from its cash reserve. However, such a scenario is not a cause for alarm if it prevails in the short term. It can, however, be a cause for alarm if it extends to the long term, which will be unsustainable for the business and will require swift action for the adjustment of dividends payout.

The P/AFFO is more preferred than P/FFO when measuring the REITs performance since the former deducts expenses incurred by the business in detail, including capital expenditures and routine maintenance costs. The P/FFO only considers the depreciation and amortization costs, while excluding other important costs that affect a company’s value.

Another point of contention between the two metrics is that the P/FFO is more standardized than the P/AFFO for most companies. There are guidelines that companies can use when calculating the P/FFO, but there is no standard method for calculating the P/AFFO.

It means that every company can use its preferred way to determine its P/AFFO; the values obtained by companies may not be comparable with other values across the industry. Comparison is an important aspect in the real estate industry since it enables experts to determine how different companies are performing.

For a steady growth of per-share P/AFFO and an increase in the dividends payable to shareholders, companies are required to maintain lower costs of capital than cash yields. Debt is a key aspect for most companies since they can take on debt to boost their growth or cover a deficit in the financing of their operations. However, the cost of debt varies, and companies should obtain the cheapest debts that are flexible and with manageable terms of repayment.

Companies use leverage ratios to evaluate the risk associated with a given debt offer. The ratio is also used by credit rating bureaus in assessing the viability of REITs in terms of credit. Creditors use the data obtained by the rating agencies to prove the creditworthiness of a borrowing firm.

The data elaborates on the cash flow and ability of a REIT to comfortably repay the debt and whether they have other outstanding debts with other creditors. A company’s credit rating is essential to its creditworthiness since creditors consult such records to gauge the repayment ability and the default risk. Low credit rates, therefore, limit a company’s growth opportunity.

CFI is the official provider of the Commercial Banking & Credit Analyst (CBCA®) certification program, designed to transform anyone into a world-class financial analyst.

In order to help you become a world-class financial analyst and advance your career to your fullest potential, these additional resources will be very helpful:

Below is a break down of subject weightings in the FMVA® financial analyst program. As you can see there is a heavy focus on financial modeling, finance, Excel, business valuation, budgeting/forecasting, PowerPoint presentations, accounting and business strategy.

A well rounded financial analyst possesses all of the above skills!

CFI is the global institution behind the financial modeling and valuation analyst FMVA® Designation. CFI is on a mission to enable anyone to be a great financial analyst and have a great career path. In order to help you advance your career, CFI has compiled many resources to assist you along the path.

In order to become a great financial analyst, here are some more questions and answers for you to discover: