P/FFO vs P/AFFO

Learn more about P/FFO and P/AFFO

What is P/FFO vs P/AFFO?

P/FFO vs P/AFFO are considered more sophisticated metrics to measure REIT performance. Though earnings per share (EPS) is often used to measure the performance of a REIT, P/FFO (Price/Funds from Operations) and P/AFFO (Price/Adjusted Funds from Operations) are preferred since they embrace procedures that better estimate the performance of the real estate industry.

EPS takes the total revenues for the period minus all costs, divided by the total number of shares to get the earnings per share. It does not consider the fact that certain costs may be non-cash, such as amortization and depreciation. Non-cash expenses reduce the dividends paid to the shareholders, while most real estate properties appreciate as opposed to depreciating. The P/FFO and, consequently, the P/AFFO take into consideration such costs and overlook them to give the shareholders their deserved dividend amounts.

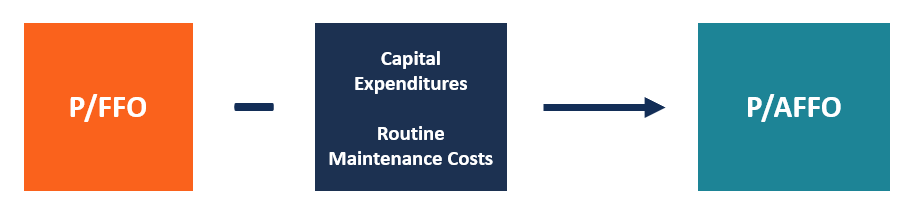

Differences: P/FFO vs P/AFFO

There are two conspicuously notable differences between the two methods of determining the performance of a real estate investment trust (REIT). First, the P/FFO comes with a common formula across the board used by different companies, while the P/AFFO lacks a standard formula. Different companies use different formulas and include various factors in the formula for calculating the P/AFFO. It makes the P/AFFO difficult to compare between different companies and REITs.

Secondly, the P/AFFO is an adjusted version of the P/FFO. The P/AFFO is adjusted by subtracting any capital expenditures from the P/FFO. The P/FFO ignores capital expenditures and other routine maintenance costs like repainting and roof replacement. They are vital costs that keep the property in its best condition and make it attractive to investors and potential tenants. The P/AFFO also subtracts straight-line rent income, which decreases the cash available for distribution.

Similarities: P/FFO vs P/AFFO

P/FFO is the net income plus amortization and depreciation. The costs are added back because when calculating the net income, we deduct the total costs from the total revenue.

Depreciation and amortization are non-cash expenses that do not affect the cash flows of a company. Deducting non-cash expenses from the revenue results in a lower profit. Therefore, the dividends distributed to shareholders are reduced by the sum of the non-cash expenses.

Both the P/FFO and P/AFFO add back the non-cash costs to the net income to eliminate the effects of depreciation and amortization, which do not affect cash flow. Both methods work better than conventional procedures such as the EPS in measuring the real estate industry’s performance.

Both metrics are also common in the measurement of REITs but are not yet defined in financial reporting standards. Currently, the International Financial Reporting Standards (IFRS) does not officially recognize the two procedures as qualified measurements for the real estate industry.

P/FFO vs. P/AFFO: Which is More Appropriate to Use?

Between the two metrics, the most appropriate measurement for evaluating the real estate industry depends on the instance. When conducting a comparison of REITs across multiple companies, the most preferred metric is the P/FFO. This is because P/FFO is standardized, and multiple REITs will use the standard formula.

P/AFFO lacks a standardized formula. The adjusted funds from operations can, however, be termed as a better estimator of the REIT’s performance since it eliminates non-cash costs from the formula. The P/AFFO is precise since it subtracts the capital expenditures and other routine maintenance expenses.

Both methods offer the possibility of giving a common estimate in rare circumstances. If a REIT does not incur depreciation, amortization, and capital expenditures, both methods will arrive at similar figures in the measurement of REIT performance. For example, the P/FFO takes the net income and adds depreciation and amortization, which, in this case, is absent, making both formulas identical. The P/AFFO takes the P/FFO and subtracts the capital expenditures and other routine expenses, which, in this case, are absent.

Related Readings

CFI is the official provider of the Financial Modeling and Valuation Analyst (FMVA)™ certification program, designed to transform anyone into a world-class financial analyst.

To keep learning and developing your knowledge of financial analysis, we highly recommend the additional CFI resources below:

Additional Resources

CFI is a global provider of financial modeling courses and of the FMVA Certification. CFI’s mission is to help all professionals improve their technical skills. If you are a student or looking for a career change, the CFI website has many free resources to help you jumpstart your Career in Finance. If you are seeking to improve your technical skills, check out some of our most popular courses. Below are some additional resources for you to further explore:

The Financial Modeling Certification

Analyst Certification FMVA® Program

CFI is a global provider of financial modeling courses and of the FMVA Certification. CFI’s mission is to help all professionals improve their technical skills. If you are a student or looking for a career change, the CFI website has many free resources to help you jumpstart your Career in Finance. If you are seeking to improve your technical skills, check out some of our most popular courses. Below are some additional resources for you to further explore:

The Financial Modeling Certification

Below is a break down of subject weightings in the FMVA® financial analyst program. As you can see there is a heavy focus on financial modeling, finance, Excel, business valuation, budgeting/forecasting, PowerPoint presentations, accounting and business strategy.

A well rounded financial analyst possesses all of the above skills!

Additional Questions & Answers

CFI is the global institution behind the financial modeling and valuation analyst FMVA® Designation. CFI is on a mission to enable anyone to be a great financial analyst and have a great career path. In order to help you advance your career, CFI has compiled many resources to assist you along the path.

In order to become a great financial analyst, here are some more questions and answers for you to discover:

- What is Financial Modeling?

- How Do You Build a DCF Model?

- What is Sensitivity Analysis?

- How Do You Value a Business?