Get Certified for

Commercial Banking (CBCA®)

Stand out and gain a competitive edge as a commercial banker, loan officer, or credit analyst with advanced knowledge, real-world analysis skills, and career confidence.

"Price to Funds From Operations"

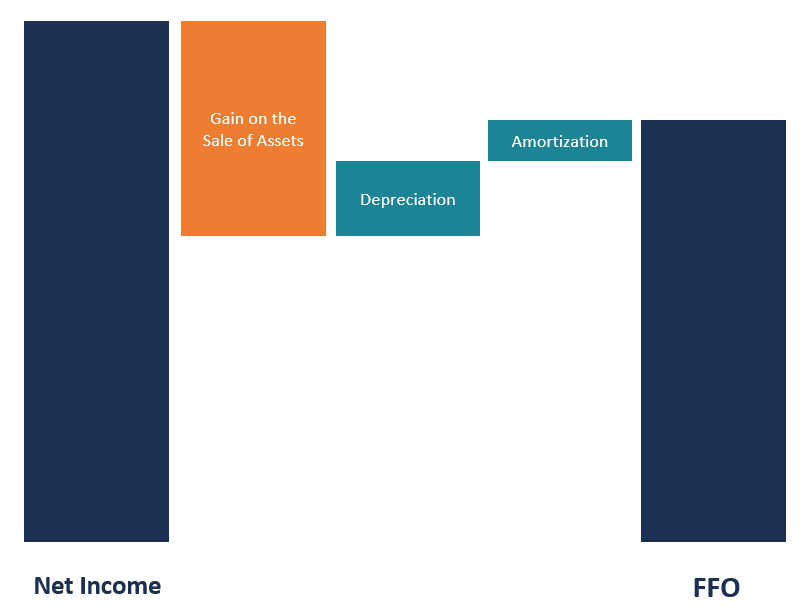

P/FFO, or Price to Funds From Operations, can be described as a reliable and modern way of determining the value of a Real Estate Investment Trust (REIT). The P/FFO metric is calculated by adding amortization and depreciation to the net income and then deducting the gains on the sale of properties.

Unlike other conventional methods of determining the value of a REIT like EPS (Earnings Per Share) and P/E (Price to Earnings), the FFO is reliable to a large extent. In the evaluation of FFO, the net income is the bottom line, although it includes the value of the depreciation expense. In most businesses, depreciation is an accepted expense that is allocated as part of the investment cost. However, in real estate, properties appreciate in value, and they rarely depreciation in value like other assets such as equipment or machinery.

Net income is an inferior measure of real estate performance. Unlike net income, FFO excludes depreciation, making it a more preferred measure of real estate performance. Companies are required to disclose the FFO and the net income values in the footnotes in every reporting period. The FFO equals net income plus depreciation and amortization minus any gains on sales of properties. The gains are subtracted because they are non-recurrent and not part of the core operations of the business.

P/FFO is a better measure of a REIT performance than any other cost accounting procedures. Many real estate investments increase in value over time, and should not be depreciated like other types of assets. However, many conventional cost-accounting procedures charge depreciation as an expense, while many properties increase in value over time. The FFO is a good predictor of REIT value since it does not account for depreciation in properties but rather adds back the depreciation value back to the net income.

FFO deducts any gains or losses from the sale of assets, since including the transaction would result in discrepancies in the revenues reported in each period. It would present the company as too profitable when it has earned profits from the sale of properties in one period, while in other periods, the company would be viewed as unprofitable when it has not sold any real estate properties. Other valuation methods do not make a similar consideration, making them unreliable.

The P/FFO does not account for deductions of capital expenditures, such as the maintenance of properties in the existing portfolio. Capital expenditures like repainting the premises and replacing worn-out roofs are important in maintaining high standards in the real estate. FFO does not account for such expenditures, and therefore, it is not a true residual figure after all expenses and expenditures are deducted. The Adjusted Funds from Operations (AFFO) addresses such weaknesses by accounting for the left-out adjustments.

The AFFO is regarded as a better predictor of the REITs value than the FFO. The AFFO is preferred to the FFO for several reasons. One of the reasons is that it gives a better estimate figure of a REIT’s value with a more precise residual figure for the data consumers. It can also predict more precisely the value of future dividends, which enables investors to plan on shares investments.

FFOPS is obtained by dividing the proceeds from operations in a company by the number of shares. REITs are required by law to distribute a majority of their net taxable earnings to shareholders as dividends. It is because they are taxed as individual incomes rather as a corporation, which is in a higher tax bracket. The FFOPS, therefore, helps in determining the per-share value of the investment.

The FFOPS is determined by adding the amortization and depreciation back to the net income and then subtracting any gains in sales from the sum, which gives the FFO. The result is then divided by the total sum of shares in the portfolio, which gives the per-share value for the funds from operations. The term FFOPS and cash from operations per share are two different terms that mean different things. The latter is an important component in a cash flow statement, while the former is used to evaluate the value of a REIT.

An FFO Multiple is the factor by which the FFO per share determines the value of the property. The FFO multiple is evaluated by taking the price per share and dividing it by the FFO per share. The FFO multiple helps in complementing the FFO in the valuation of a REIT. They are both used in measuring the performance of an investment.

CFI is the official provider of the Commercial Banking & Credit Analyst (CBCA®) certification program, designed to transform anyone into a world-class financial analyst.

In order to help you become a world-class financial analyst and advance your career to your fullest potential, these additional resources will be very helpful:

Below is a break down of subject weightings in the FMVA® financial analyst program. As you can see there is a heavy focus on financial modeling, finance, Excel, business valuation, budgeting/forecasting, PowerPoint presentations, accounting and business strategy.

A well rounded financial analyst possesses all of the above skills!

CFI is the global institution behind the financial modeling and valuation analyst FMVA® Designation. CFI is on a mission to enable anyone to be a great financial analyst and have a great career path. In order to help you advance your career, CFI has compiled many resources to assist you along the path.

In order to become a great financial analyst, here are some more questions and answers for you to discover: