Get In-Demand Finance Certifications

Overview of key concepts

This guide will outline the foundations of real estate financial modeling and the key concepts you need to get started building your own models for development projects.

In order to get started, we will begin by defining some of the key terms you’ll need to know before building your model.

LTV – “loan to value” – the amount of debt financing a lender will provide as a percent of the market value (e.g., 80%)

LTC – “loan to cost” – the amount of debt financing a lender will provide as a percent of the cost of a development (e.g., 70%)

NOI – “net operating income” – gross rental revenue less operating expenses (property taxes, insurance, repairs & maintenance, capital expenditures, etc.)

Cap Rate – net operating income divided by the value of the property, expressed as a percentage (e.g., 4.5%)

Amortization period – the number of months/years the principal repayments of a loan are spread out over. The total length of time it will take you to pay off your mortgage (e.g., 30 years).

Most developments are structured as a joint venture between General Partners (GPs) and Limited Partners (LPs).

Key points about GPs:

Key points about LPs:

As covered in CFI’s real estate financial modeling course, the key assumptions that will be input into the model include:

These are discussed in great detail in our actual course.

To set the foundations of real estate financial modeling, it is important to cover the key sections that will be built based on project assumptions.

The key sections in the development model include:

Once the model is built, it’s important to create a one-page summary document or Pro Forma that can be shared with bankers, investors, partners, and anyone else who needs to analyze the deal.

This output pro forma should include the following information:

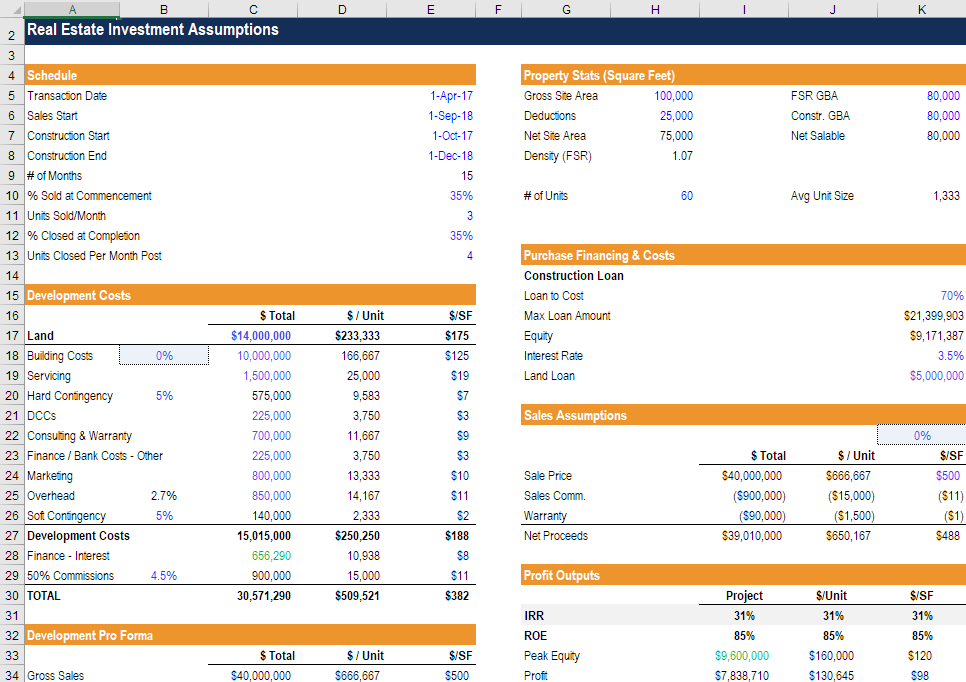

This is an example of the one-page output from our real estate financial modeling course. As you can see, it clearly displays all the information listed above and makes it easy for someone to evaluate the deal.

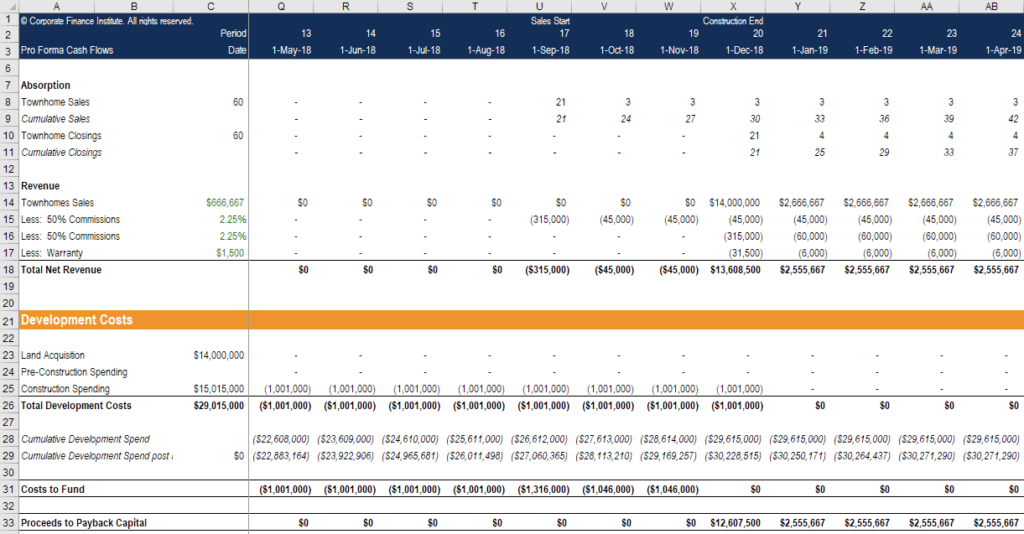

Here is an example of the actual inner workings of the model, where you can see absorption by month for the development project, which builds up to revenue and, ultimately, cash flow.

These foundations of real estate financial modeling are covered along with much more detail in our online course.

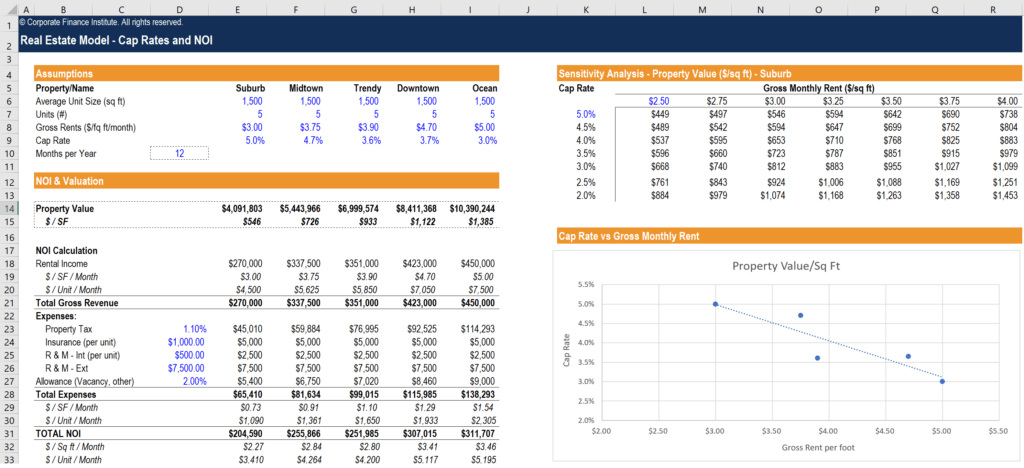

Net operating income, which is equal to gross rental revenue less operating expenses (property taxes, insurance, repairs & maintenance, capital expenditures), is the key profitability or cash flow measure used to evaluate real estate development transactions.

Cap rate, which is equal to net operating income divided by the value of the property, is expressed as a percentage and used to value real estate. The lower the cap rate, the more highly valued a piece of real estate is, and the higher the cap rate, the less valued the real estate is. Price and cap rate move in inverse directions to each other, just like a bond. Learn more in our financial math course.

The best way to learn is by doing, and CFI’s real estate financial modeling course gives you the step-by-step instruction you need to build financial models on your own. It comes with both a blank template and a completed version, so you can either build a model yourself or go straight to the completed version. The high-quality video instruction will guide you every step of the way as you work through a case study for a townhouse real estate development project.

Connect what you just learned to a clear career path with CFI’s role‑based courses and certification programs.

Thank you for reading CFI’s guide to Foundations of Real Estate Financial Modeling. To learn more about valuation, corporate finance, financial modeling, and more, we highly recommend these additional free CFI resources: