Get Certified for

Capital Markets (CMSA®)

From equities and fixed income to derivatives, the CMSA certification bridges the gap from where you are now to where you want to be — a world-class capital markets analyst.

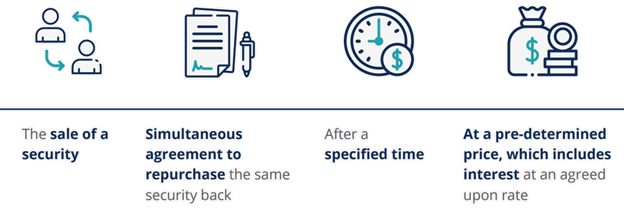

The sale and subsequent repossession of the same security at a future date at a higher price

A repurchase agreement (“repo”), also known as a sale-and-repurchase agreement, is an agreement involving the sale and subsequent repossession of the same security at a future date at a higher price. In simple terms, it is an exchange of a security (which acts as collateral) for cash. Repurchase agreements are commonly used to provide short-term liquidity.

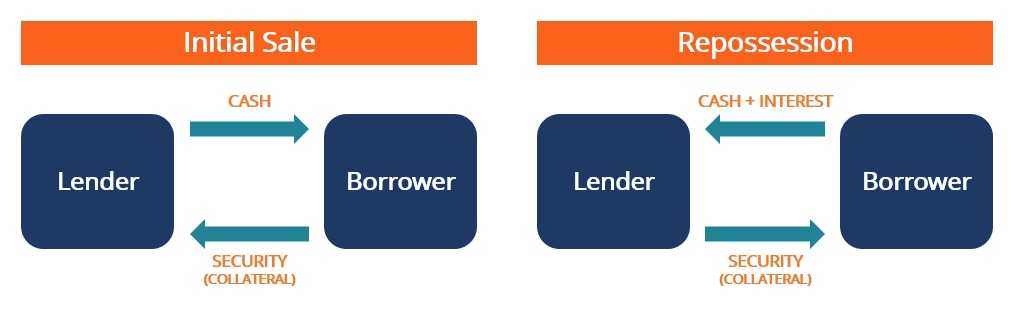

The following is a simple illustrative example of how a repurchase agreement works:

A repurchase agreement can be thought of as a collateralized loan. The lender provides cash to the borrower in exchange for a security, which acts as collateral. At a future date, the borrower repurchases the same security with the initial cash received plus accrued interest.

Below, the lifecycle of a repurchase agreement and the parties involved are detailed.

The lifecycle of a repurchase agreement involves a party selling a security to another party and simultaneously signing an agreement to repurchase the same security at a future date at a specified price. The repurchase price is slightly higher than the initial sale price to reflect the time value of money. This is visually illustrated below.

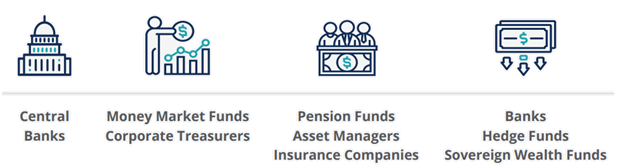

There are two parties involved in a repurchase agreement:

Participants in a repurchase agreement include central banks, money market funds, corporate treasurers, pension funds, asset managers, insurance companies, banks, hedge funds, and sovereign wealth funds.

At a high level, the party selling securities in a repurchase agreement commonly does so to be able to raise short-term funds, while the party purchasing the securities commonly does so to earn interest on excess cash.

However, there may be specific use cases for engaging in repurchase agreements. For example, the U.S. Federal Reserve engages in repurchase agreements as part of its monetary policy and for liquidity management purposes. Specific use cases for repurchase agreements by certain parties are outlined in CFI’s course on repurchase agreements.

For a Canada-specific benchmark that reflects overnight repo market activity, see Canadian Overnight Repo Rate Average (CORRA).

In general, high-quality debt securities are used in a repurchase agreement. The securities function as collateral in a repurchase agreement. Examples may include government bonds, agency bonds, supranational bonds, corporate bonds, convertible bonds, and emerging market bonds.

The duration (time length) of a repurchase agreement is referred to as the tenor. There are two main types of repo tenors:

The repurchase agreement rate is the interest rate charged to the borrower (i.e., the party borrowing cash by using its securities as collateral) in a repurchase agreement. The repo rate is a simple interest rate that is stated on an annual basis using 360 days. To understand this, an example is presented below.

A trader enters into a repurchase agreement with a hedge fund by agreeing to sell U.S. treasuries with a market value of $9,579,551.63 to a hedge fund at a repo rate of 0.09% with a fixed one week tenor. What is the total payment that the trader must make to the hedge fund at the end of the repurchase agreement?

First, we calculate the required interest payment. This is calculated as Principal x Repo Rate x (No. of Days Outstanding / 360) = $9,579,551.63 x 0.09% x (7 / 360) = $167.64.

Next, we add the interest payment to the principal amount to determine the total payment. This is calculated as $9,579,551.63 + $167.64 = $9,579,719.27.

To learn more about the core concepts of short-term funding, check out CFI’s Repo (Repurchase Agreements) course!

Connect what you just learned to a clear career path with CFI’s role‑based courses and certification programs.

CFI offers the Capital Markets & Securities Analyst (CMSA)® certification program for those looking to take their careers to the next level. To keep learning and advance your career, the following resources will be helpful: