Get In-Demand Finance Certifications

The number of shares after dilutive securities are taken into account

Fully diluted shares outstanding is the total number of shares a company would theoretically have if all dilutive securities were exercised and converted into shares. Dilutive securities include options, warrants, convertible debt, and anything else that can be converted into shares. For a financial analyst, it is important to have a solid understanding of the difference between basic and fully diluted shares and what it means for key metrics like EPS.

Public companies are required to report both Basic and Diluted Shares, which they use in their calculation of Earnings Per Share (EPS). Below are an explanation and comparison of Basic EPS vs. Diluted EPS.

Basic EPS

Basic earnings per share is calculated by taking the total net income from the period and dividing it by the weighted average shares outstanding during the period.

Diluted EPS

Diluted earnings per share is derived by taking net income during the period and dividing by the average fully diluted shares outstanding in the period. The diluted shares are calculated by taking into account the effect of employee stock awards, options, convertible securities, etc.

When EPS is Negative (a Loss)

When companies experience a period with a loss or negative EPS, they will not include dilutive securities in the calculation of EPS, as they would have an anti-dilutive effect.

Amazon Example

Below is an example of what Amazon discloses in their Form 10-K about how many basic and diluted shares they have outstanding.

Most public companies use stock-based compensation as a way of incentivizing and rewarding their employees. By granting stock to employees, the companies are increasing the number of shares outstanding, which causes dilution and needs to be factored into the financial analysis.

Employee stock options, shares, and restricted share units are subject to a vesting period, typically between two and five years. Since some employees will quit before their shares vest, companies typically make an estimate, based on judgment, about forfeitures and the total number that will actually vest.

This category is often one of the biggest causes of dilution to shares outstanding.

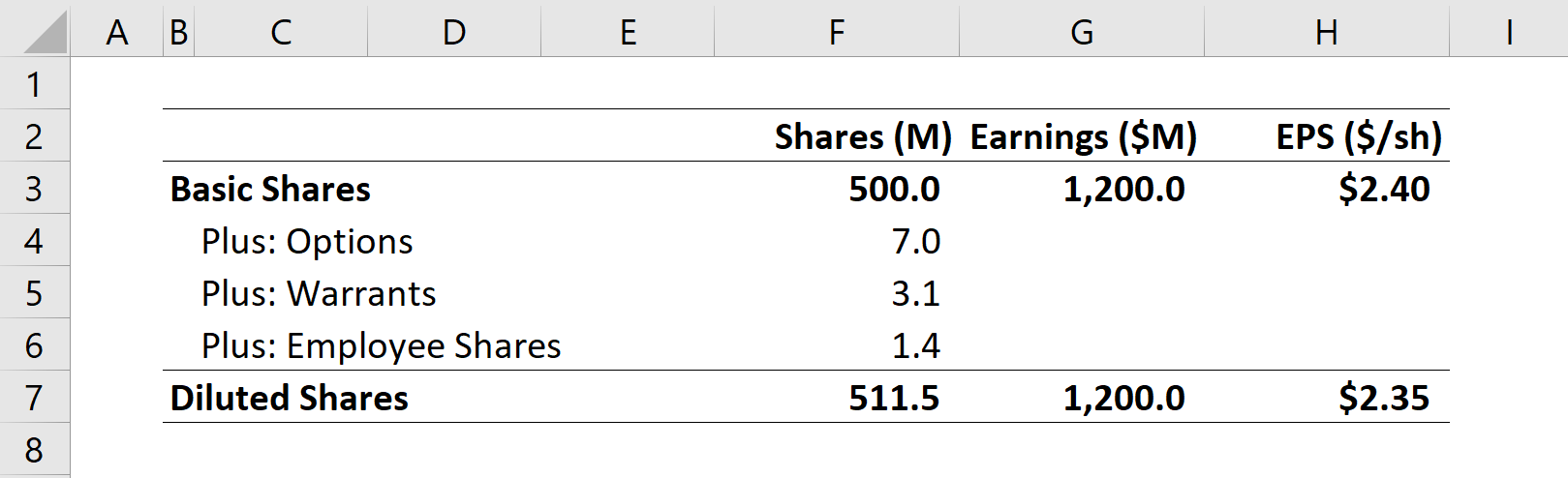

Below is an example of how to calculate diluted shares outstanding for a company, as well as basic and diluted EPS. As you can see, the basic shares are increased by the effect of options, warrants, and employee shares that have been issued.

The company reported $1.2 billion of net earnings, so its basic EPS is $2.40, and its diluted EPS is $2.35.

Thank you for reading CFI’s guide to Diluted Shares Outstanding. To continue learning and advancing your career, these additional guides will be helpful:

Below is a break down of subject weightings in the FMVA® financial analyst program. As you can see there is a heavy focus on financial modeling, finance, Excel, business valuation, budgeting/forecasting, PowerPoint presentations, accounting and business strategy.

A well rounded financial analyst possesses all of the above skills!

CFI is the global institution behind the financial modeling and valuation analyst FMVA® Designation. CFI is on a mission to enable anyone to be a great financial analyst and have a great career path. In order to help you advance your career, CFI has compiled many resources to assist you along the path.

In order to become a great financial analyst, here are some more questions and answers for you to discover:

Learn accounting fundamentals and how to read financial statements with CFI’s online accounting classes.

These courses will give you the confidence to perform world-class financial analyst work. Start now!

Boost your confidence and master accounting skills effortlessly with CFI’s expert-led courses! Choose CFI for unparalleled industry expertise and hands-on learning that prepares you for real-world success.