Get In-Demand Finance Certifications

A company's enterprise value divided by its total annual revenue

The Enterprise Value to Revenue Multiple is a valuation metric used to value a business by dividing its enterprise value (equity plus debt minus cash) by its annual revenue. The EV to revenue multiple is commonly used for early-stage or high-growth businesses that don’t have positive earnings yet.

If a company doesn’t have positive Earnings Before Interest Taxes Depreciation & Amortization (EBITDA) or positive Net Income, it’s not possible to use EV/EBITDA or P/E ratios to value the business. In this case, a financial analyst will have to move further up the income statement to either gross profit or all the way up to revenue.

If EBITDA is negative, then having a negative EV/EBITDA multiple is not useful. Similarly, a company with a barely positive EBITDA (almost zero) will result in a massive multiple, which isn’t very useful either.

For these reasons, early-stage companies (often operating at a loss) and high growth companies (often operating at breakeven) require an EV/Revenue multiple for valuation.

The formula for calculating the multiple is:

Where:

Here is an example of how to calculate the EV to Revenue multiple:

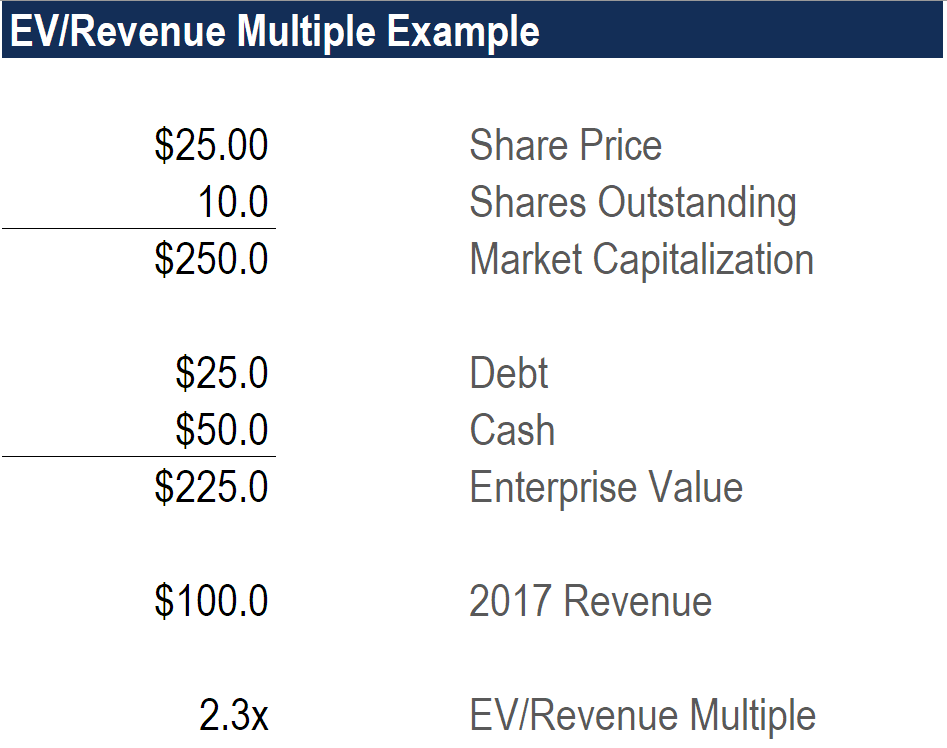

Suppose a company has a current share price of $25.00, shares outstanding of 10 million, a debt of $25 million, cash of $50 million, no preferred shares, no minority interest, and a 2017 revenue of $100 million. What is its EV/Revenue ratio?

Answer:

Below is a screenshot of the calculation in Excel:

Download the free Excel template now to advance your finance knowledge!

EV is used instead of the price or market cap in the numerator to remove any impact of valuation caused by a company’s capital structure. This will allow the comparison of values between similar-type companies with different capital structures (debt vs. equity mix).

As with any valuation method, there are advantages and disadvantages, which are outlined below:

As a case study, you can learn how to calculate the EV to revenue multiple in two of CFI’s online courses. The first example is in the Business Valuation course, which leads students through a detailed exercise of creating a “Comps Table” or comparable company analysis.

The second example is in CFI’s e-Commerce Financial Modeling course, where students will build a model from scratch to value a business, which includes determining the company’s EV/Revenue ratios across various years.

Thank you for reading CFI’s guide to Enterprise Value to Revenue Multiple. To continue learning on your own, these resources will be helpful:

Below is a break down of subject weightings in the FMVA® financial analyst program. As you can see there is a heavy focus on financial modeling, finance, Excel, business valuation, budgeting/forecasting, PowerPoint presentations, accounting and business strategy.

A well rounded financial analyst possesses all of the above skills!

CFI is the global institution behind the financial modeling and valuation analyst FMVA® Designation. CFI is on a mission to enable anyone to be a great financial analyst and have a great career path. In order to help you advance your career, CFI has compiled many resources to assist you along the path.

In order to become a great financial analyst, here are some more questions and answers for you to discover: