Get Certified for Financial Modeling (FMVA)®

Gain in-demand industry knowledge and hands-on practice that will help you stand out from the competition and become a world-class financial analyst.

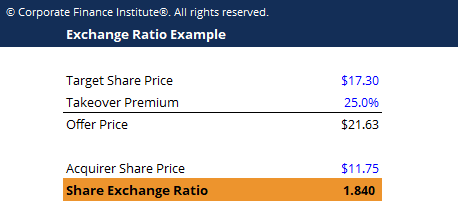

Ratio of shares traded in a merger and acquisition

In mergers and acquisitions (M&A), the exchange ratio measures the number of shares the acquiring company has to issue for each individual share of the target firm. For M&A deals that include shares as part of the consideration (compensation) for the deal, the share exchange ratio is an important metric. Deals can be all cash, all shares, or a mix of the two.

Assume Firm A is the acquirer and Firm B is the target firm. Firm B has 10,000 outstanding shares and is trading at a current price of $17.30 and Firm A is willing to pay a 25% takeover premium. This means the Offer Price for Firm B is $21.63. Firm A is currently trading at $11.75 per share.

To calculate the exchange ratio, we take the offer price of $21.63 and divide it by Firm A’s share price of $11.75.

The result is 1.84. This means Firm A has to issue 1.84 of its own shares for every 1 share of the Target it plans to acquire.

Enter your name and email in the form below and download the free template now from the example shown above!

In the event of an all-cash merger transaction, the exchange ratio is not a useful metric. In fact, in this situation, it would be fine to exclude the ratio from the analysis. Often times, M&A valuation models will note the ratio as “0.000” or blank, when it comes to an all-cash transaction. Alternatively, the model may display a theoretical exchange ratio, if the same value of the cash transaction were, instead, to be carried out by a stock transaction.

However, in the event of a 100% stock deal, the exchange ratio becomes a powerful metric. It becomes virtually essential and allows the analyst to view the relative value of the offer between the two firms.

In the event of a split deal, where a portion of the transaction involves cash and a portion involves a stock deal, the percentage of stock involved in the transaction must be considered. Excluding any cash effects, what is the actual exchange ratio based on the stock? Additionally, M&A models may want to also show what this transaction would look like if there was a 100% stock deal.

Accounting for exchange ratios becomes more difficult when analyzing the firm’s values. This is because it involves the transfer of some value of the acquirer firm into the target firm’s owners. When an acquiring firm offers cash to the target firm, the effect is simple. The target firm is absorbed by the acquirer in exchange for cash.

However, when an acquirer offers stock in its own firm for the target firm, the valuation becomes more complex. This is because some of the value of the acquiring firm is diluted and given to the target firm. After the transaction, some of the value of the merged firm and its synergies will be owned by the target firm. Thus, this must be taken into account when calculating the proper exchange ratio to use in an M&A transaction.

In financial modeling for M&A transactions, it’s important for an analyst to factor in the full impact of the transaction. The main impact comes from calculating the accretion/dilution of the Earnings per Share (EPS) of the combined company.

To learn more, launch CFI’s M&A financial modeling course.

CFI is the official global provider of the Financial Modeling & Valuation Analyst (FMVA® certification program, designed to transform anyone into a world-class financial analyst. To advance your career, check out these additional free resources below: