Leveraged Recapitalization

Borrowing money to pay a special dividend

What is a Leveraged Recapitalization?

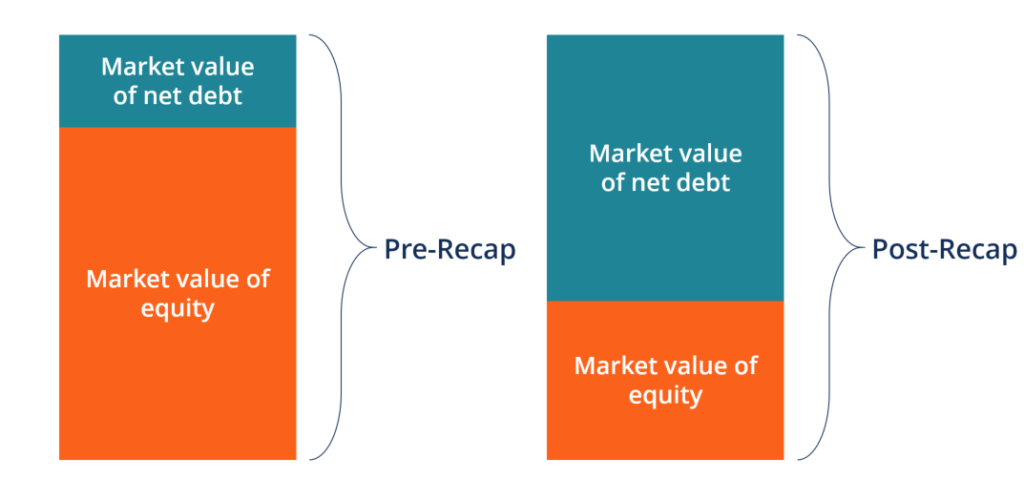

A leveraged recapitalization involves changing the capital structure of a company by increasing debt and reducing equity. This means a corporation will borrow money (i.e., issue bonds) to generate cash proceeds, which will then be used to repurchase previously issued shares and reduce the proportion of equity in the company’s capital structure. Hence the term, leveraged recapitalization.

The term capitalization is a reference to how a company is capitalized, meaning how much debt and equity it has. Both debt and equity generate a balance on the right side of the balance sheet, which is then used to fund the assets on the left side of the balance sheet.

A leveraged recapitalization is a useful financial strategy often used in conjunction with MBOs or other forms of restructuring. Higher leverage is beneficial to the company in times of strong growth; therefore the objective of a leveraged recap is often to bolster future growth prospects.

Motivations for a Leveraged Recapitalization

This often seems counterintuitive to those studying corporate finance. Why make the company more indebted than it already is? Why use debt to repay equity?

There are several mathematical proofs for the benefit of leveraged recapitalizations. One of these, for example, is the Modigliani-Miller theorem, which forms the basis of modern thought on capital structure. This theorem describes how debt provides a tax benefit or interest tax shield that equity does not.

Furthermore, using debt to purchase stock or pay off older debt reduces the opportunity cost of having to use earned profits to do the same.

Additionally, the economic environment may be such that interest rates are low. Companies may want to take advantage of this interest rate environment to perform a leveraged recapitalization.

Finally, issuing debt prevents dilution of shareholder equity, which the issuance of new shares would cause. This creates a positive effect from the point of view of shareholders.

Disadvantages of a Leveraged Recapitalization

Despite all the advantages listed above, some argue that leveraged recapitalizations limit the growth potential of a company because it does not take a longer-term view.

A leveraged recapitalization often takes into account the current debt environment, which may not stay fixed forever. In other words, if interest rates change, a leveraged recapitalization may provide a negative effect on the company in the form of increased interest expense.

Most importantly, changing the capital structure towards a heavier debt weighting increases the financial risk of the business. If things don’t go according to plan, it could end up destroying a lot of shareholder value.

Additional Resources

CFI offers the Certified Banking & Credit Analyst (CBCA)® certification program for those looking to take their careers to the next level. To keep learning and developing your knowledge base, please explore the additional relevant resources below:

Additional Resources

CFI is a global provider of financial modeling courses and of the FMVA Certification. CFI’s mission is to help all professionals improve their technical skills. If you are a student or looking for a career change, the CFI website has many free resources to help you jumpstart your Career in Finance. If you are seeking to improve your technical skills, check out some of our most popular courses. Below are some additional resources for you to further explore:

The Financial Modeling Certification

Analyst Certification FMVA® Program

CFI is a global provider of financial modeling courses and of the FMVA Certification. CFI’s mission is to help all professionals improve their technical skills. If you are a student or looking for a career change, the CFI website has many free resources to help you jumpstart your Career in Finance. If you are seeking to improve your technical skills, check out some of our most popular courses. Below are some additional resources for you to further explore:

The Financial Modeling Certification

Below is a break down of subject weightings in the FMVA® financial analyst program. As you can see there is a heavy focus on financial modeling, finance, Excel, business valuation, budgeting/forecasting, PowerPoint presentations, accounting and business strategy.

A well rounded financial analyst possesses all of the above skills!

Additional Questions & Answers

CFI is the global institution behind the financial modeling and valuation analyst FMVA® Designation. CFI is on a mission to enable anyone to be a great financial analyst and have a great career path. In order to help you advance your career, CFI has compiled many resources to assist you along the path.

In order to become a great financial analyst, here are some more questions and answers for you to discover:

- What is Financial Modeling?

- How Do You Build a DCF Model?

- What is Sensitivity Analysis?

- How Do You Value a Business?