Get In-Demand Finance Certifications

Key valuation metrics used to value mining assets

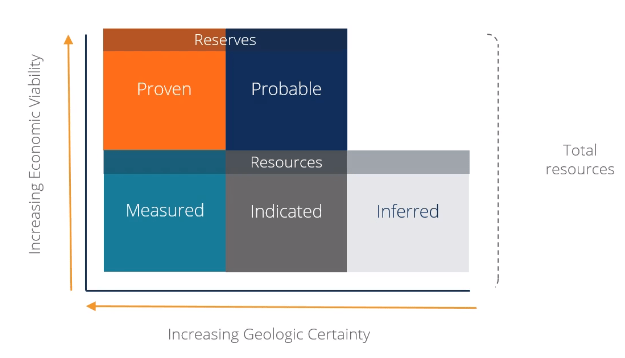

Mining assets are very challenging to value. Given the degree of geologic uncertainty around reserves and resources, it’s hard to know how much metal is actually in the ground. This guide to mining valuation will teach you all you need to know to value an asset!

The best way to value a mining asset or company is to build a discounted cash flow (DCF) model that takes into account a mining plan produced in a technical report (like a Feasibility Study). Without such a study available, one has to resort to more crude metrics.

Here is an overview of the main valuation methods used in the industry:

P/NAV is the most important mining valuation metric, period.

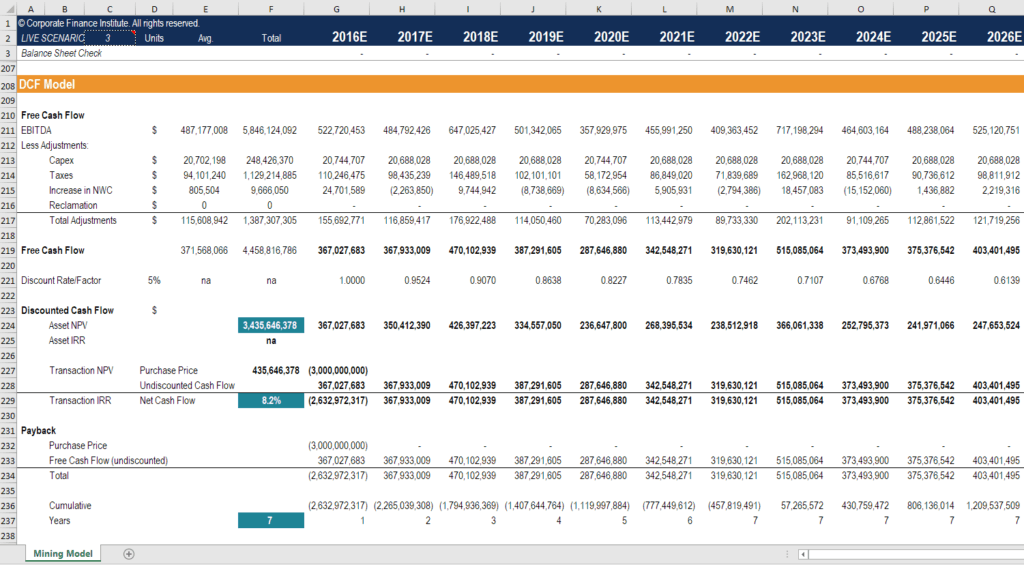

“Net asset value” is the net present value (NPV) or discounted cash flow (DCF) value of all the future cash flow of the mining asset less any debt plus any cash. The model can be forecast to the end of the mine life and discounted back today because the technical reports have a very detailed Life of Mine plan (LOM).

The formula is as follows:

P/NAV = Market Capitalization / [NPV of all Mining Assets – Net Debt]

For a more detailed overview of P/NAV see our course on mining financial modeling.

NAV is a sum-of-the-parts approach to valuation, in that each individual mining asset is independently valued and then added together. Corporate adjustments are made at the end, such as head office overhead or debt.

Below is a screenshot of a NAV model from CFI’s Mining Financial Modeling Course.

P/CF, or “P-cash flow” is also common but only used for producing mines, as it uses the current cash flow in that year, relative to the price in the security.

The ratio takes the adjusted cash flow of the business in a given year (i.e. 2018E) and compares that to the share price.

Operating cash flow is after interest (and thus an equity metric) it’s also after taxes, but it does not include capital expenditures.

The formula is as follows:

P/CF = Price per Share / Cash From Operations per Share

We discuss P/CF in more detail in our mining valuation course.

The EV/Resource ratio takes the enterprise value of the business and divides it by the total resources contained in the ground.

This metric is typically used for early-stage development projects, where there is not a lot of detailed information (not enough to do a DCF analysis).

The ratio is very basic and doesn’t take into account the capital cost to build the mine, nor the operating cost to extract the metal.

The formula is as follows:

EV/Resource = Enterprise Value / Total Ounces or Pounds of Metal Resource

Another commonly used metric in the mining industry for early-stage projects is Total Acquisition Cost or TAC.

This represents the cost to acquire the asset, build the mine and operate the mine, all on a per ounce basis.

Suppose that a publicly-traded stock’s market capitalization is $100 million dollars, and it owns 1 million ounces.

I can, therefore, acquire the asset for $100 dollars per ounce.

I know that the cost of building the mine divided by the number of ounces will be $200 dollars per ounce.

I also know that the average all-and-sustaining cost to operate the mine is about $900 dollars per ounce. Based on some studies.

All the above combine for a $1,200 per ounce TAC.

The formula is as follows:

TAC = [Cost to Acquire + Cost to Build + Cost to Operate] / Total Ounces

For detail on all of the above metrics, take a free trial of our mining financial modeling and valuation course.

Connect what you just learned to a clear career path with CFI’s role‑based courses and certification programs.

To keep learning and expanding your knowledge, check out these additional resources: