Breakup Value

The value of a company if its components were to be sold or spun off and operated independently

What is Breakup Value?

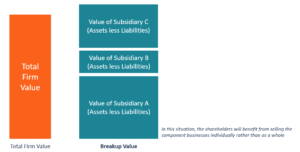

Breakup value is the value of a company if its components were to be sold or spun off and operated independently. The breakup value is obtained by taking the total assets of each component and deducting the total liabilities. If the current breakup value exceeds the current market value of the company, it will pay off to sell off the components of the company in order to increase the shareholder value.

The net proceeds from the sale of the components are then distributed to shareholders as dividends. An alternative to selling off the components is to spin off the components and allocate shares in the spun-off companies to the shareholders of the parent company.

Summary

- Breakup value is the market value of a company if its components were to be sold off and the main business left to operate independently.

- Investors use the breakup value to assess a company’s financial strength and determine the best entry point for investment.

- The breakup value is derived by calculating the total assets of each business unit minus its liabilities.

Causes of a Company Breakup

The following are some of the situations that may cause a company to break up:

1. Bad management

One of the common causes of a company breakup is poor management. When one subsidiary of the company is run down by its management and all efforts to revive it are unsuccessful, the board of directors may decide to split it apart and sell its assets for cash.

An alternative is to spin off the subsidiary to another company. In return, the parent company will receive compensation in the form of cash or shares of stock in the acquiring company. The acquirer may decide to give the target company’s shareholders a single share of stock in exchange for one or more shares in the company.

2. Liquidity problems

The other event that may trigger a company to sell off one of its subsidiaries is unresolved liquidity problems. When one subsidiary runs short of funds to finance its operations, the parent company bears the responsibility to salvage the company until it recovers. However, it may affect the operations of the parent company and other subsidiaries.

The parent will be redirecting its cash resources into the struggling component rather than investing the money in revenue-generating activities. If the subsidiary is unable to recover, the parent can sell the whole subsidiary to another business. It may use the proceeds from the sale to restore the operations of the main business and other subsidiaries.

3. One division is slowing down the growth of the company

A company that is experiencing rapid growth may decide to sell one of the divisions that is growing at a slow pace than the rest of the business. Although profitable, the division will slow down the growth of the company and its other divisions, making it less competitive in an industry where other competitors are experiencing faster growth than the company. Selling off the division will provide additional funds to finance the rapid growth, as well as allow the company to experience more intense growth than its competitors.

How the Breakup Value is Used

Investors may use the breakup value of a company in two main ways:

1. Assess the financial strength of a company

Investors may calculate the breakup value of a company to decide whether or not to hold on to their shareholding. If the shares of the company are trading at a discount relative to the breakup value, it signifies that the stock is undervalued and offers a chance of appreciating in the long term.

Therefore, they should continue holding onto their shares, unless there are other factors that provide a negative outlook of the company’s future. If the company is performing poorly, the shareholders may call for the subsidiaries to be sold or spun off. The proceeds may be shared among the shareholders in the form of cash or stock in the acquirer’s company.

2. Determine the potential entry point for a prospective buyer

Before buying stock in a perceived high-growth company, potential investors can calculate the breakup value of the company to determine the best entry point. Investors will need access to the latest data for each operating unit’s revenues, earnings, and cash flows. They can then use the relative valuations method or discounted cash flow method to derive the breakup value of the company.

How to Calculate the Breakup Value of a Company

Investors can use the following valuation methods to calculate the value of each segment:

1. Relative valuations

The relative valuation method compares the value of the segment to comparable peers or competitors in the industry. The method uses ratios, averages, and multiples to determine how business segments are performing vis-à-vis its comparable entities.

The price-to-earnings ratio is the most commonly used valuation multiple when calculating the breakup value of a company. If a segment with a low P/E is trading at a lower price per dollar of earnings per share, it is considered undervalued.

2. Discounted Cash flow (DCF) Model

The discounted cash flow (DCF) valuation method uses future expected cash flows to determine the value of an investment. The future cash flows are then discounted to get the present value of the investment opportunity. If the value obtained through the DCF model is higher than the cost of the investment, it may point to an investment with a positive future outlook.

Related Readings

CFI is the official provider of the Financial Modeling and Valuation Analyst (FMVA)™ certification program, designed to transform anyone into a world-class financial analyst.

To keep learning and developing your knowledge of financial analysis, we highly recommend the additional resources below:

Analyst Certification FMVA® Program

Below is a break down of subject weightings in the FMVA® financial analyst program. As you can see there is a heavy focus on financial modeling, finance, Excel, business valuation, budgeting/forecasting, PowerPoint presentations, accounting and business strategy.

A well rounded financial analyst possesses all of the above skills!

Additional Questions & Answers

CFI is the global institution behind the financial modeling and valuation analyst FMVA® Designation. CFI is on a mission to enable anyone to be a great financial analyst and have a great career path. In order to help you advance your career, CFI has compiled many resources to assist you along the path.

In order to become a great financial analyst, here are some more questions and answers for you to discover:

- What is Financial Modeling?

- How Do You Build a DCF Model?

- What is Sensitivity Analysis?

- How Do You Value a Business?